撰文:David Canellis,Blockworks

编译:AididiaoJP,Foresight News

Fundstrat 的首席投资官 Tom Lee 或许是这轮牛市的「多头之王」

当然,有很多人投身加密领域是出于对技术的热爱。

事实上,真正为了技术而投身其中,比如基于区块链的数字城邦、智能城市,以及现实世界资产代币化才是成为「顶级多头」的最有效途径。

Michael Saylor:极度推崇技术;DFJ 投资公司创始合伙人 Tim Draper、a16z 联合创始人 Marc Andreessen、Coinbase 联合创始人兼 CEOBrian Armstrong 和前 Coinbase CTO Balaji Srinivasan 也是如此。还有谁比他们更疯狂呢?

答案就是 Fundstrat 首席投资官 Tom Lee。

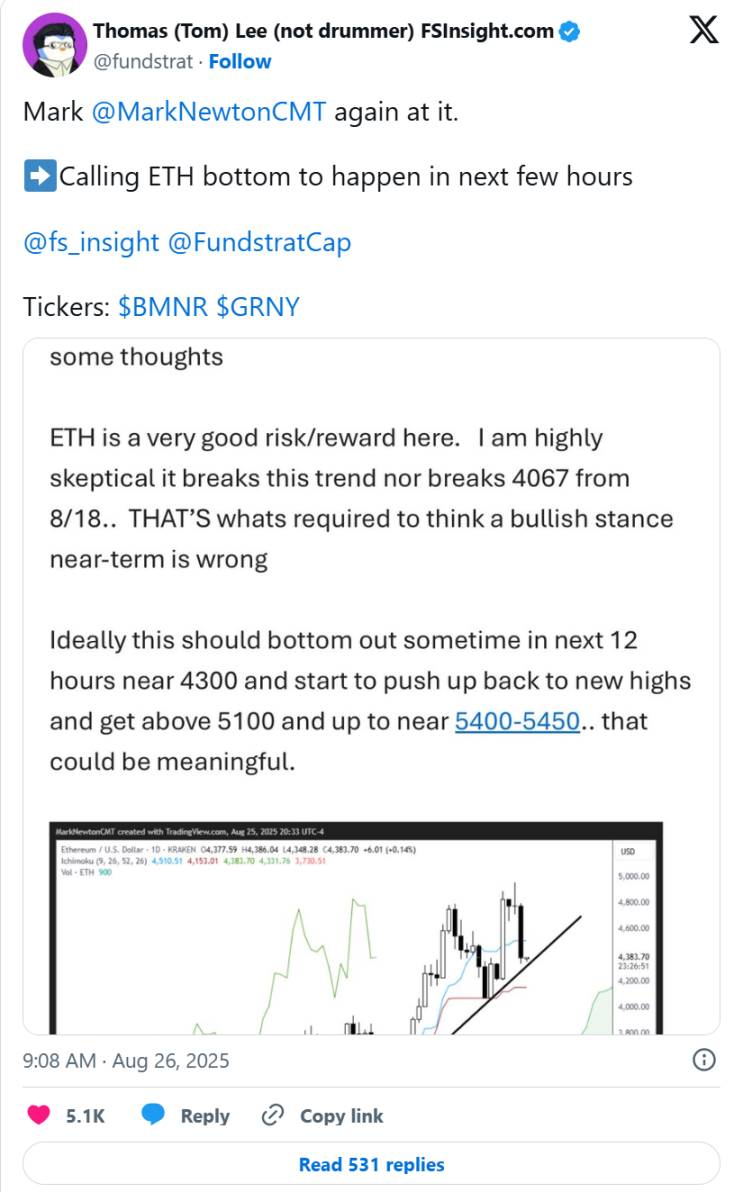

昨晚九点,Tom Lee 已经开始喊单 ETH 底部已经出现。

实际上,Tom Lee 看涨的时间比当今几乎所有仍在活跃的人都要长。

他首次公开预测加密货币的价格是在 2017 年年中。当时比特币价格在上半年翻了一倍多,达到 2500 美元,这促使 Tom Lee 在截至 2018 年 5 月的 10 个月内,至少对比特币的未来价格进行了 10 次预测。

他的第一个预测实际上成真了。「加密货币正在蚕食投资者对黄金的需求,」Tom Lee 在八年前比特币处于 2607 美元时写给 Fundstrat 客户的报告中表示。「比特币正在成为一种更稀缺的价值存储手段。投资者需要制定策略来捕获加密货币潜在上涨带来的收益。」

-

实际走势:到 2022 年,比特币将达到 2 万美元。涨幅近 10 倍。

-

预测走势:到 2022 年,达到 5.5 万美元。五年内涨 22 倍。

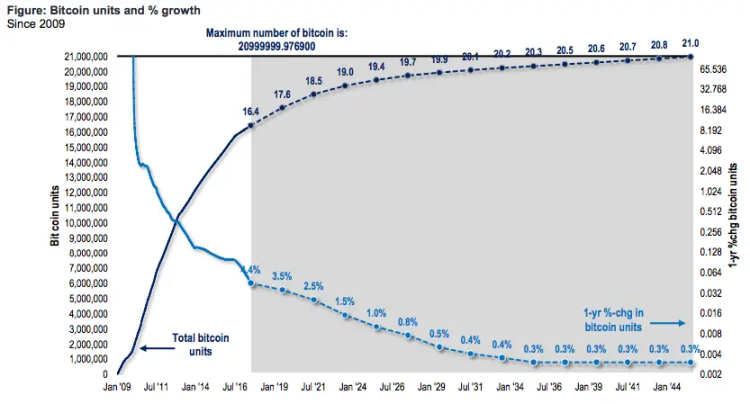

Tom Lee 的报告中包含了这张关于比特币稀缺性的实用图表。

Tom Lee 完全正确,比特币在 2021 年 2 月首次突破 5.5 万美元,比预期稍早一些,并在九个月后触及 6.9 万美元以上的峰值。

让事情变得复杂的是,他在第一次成功预测之后继续做出预测。

有些预测最终是正确的,但要么预测价格太低,要么预测时间太早;其他预测则并未如他设想的那样实现(例如围绕 2018 年 Consensus 会议的反弹从未发生,或者比特币在 2018 年多次预测均未达到 2.5 万美元)。

不过,还有其他一些精彩的预测。2018 年 1 月,他表示比特币到 2022 年可能达到 12.5 万美元,这一目标在三年后实现了。

2020 年底,他预测到 2025 年初,比特币的价格将在 10 万至 15 万美元之间,综合考虑这一预测并不算太离谱。

但如果对 Tom Lee 预测最差的批评是说它们已经成为历史,那么你会喜欢他最近的预测:2025 年比特币可能达到 20 万至 25 万美元(三周前的预测),并在未来几年内超过 100 万美元。

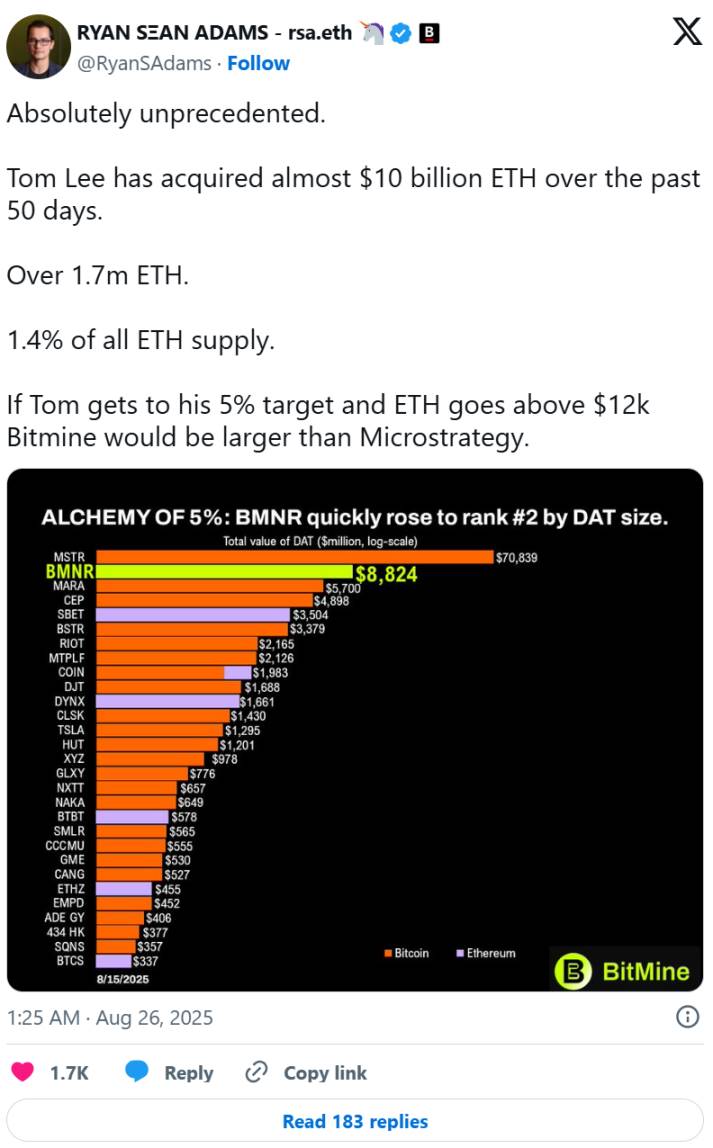

Tom Lee 最近首次公开发表了对 ETH 的预测,这是在他担任 BitMine 董事长仅约一个月后做出的,而 BitMine 正在执行以以太坊为重点的国库计划。

Tom Lee 预测:到今年年底,ETH 可能达到每枚 1.5 万至 1.6 万美元,较当前价格上涨 3 倍。

但为了保险起见,也许在这个价格基础上需要再多加几年时间。