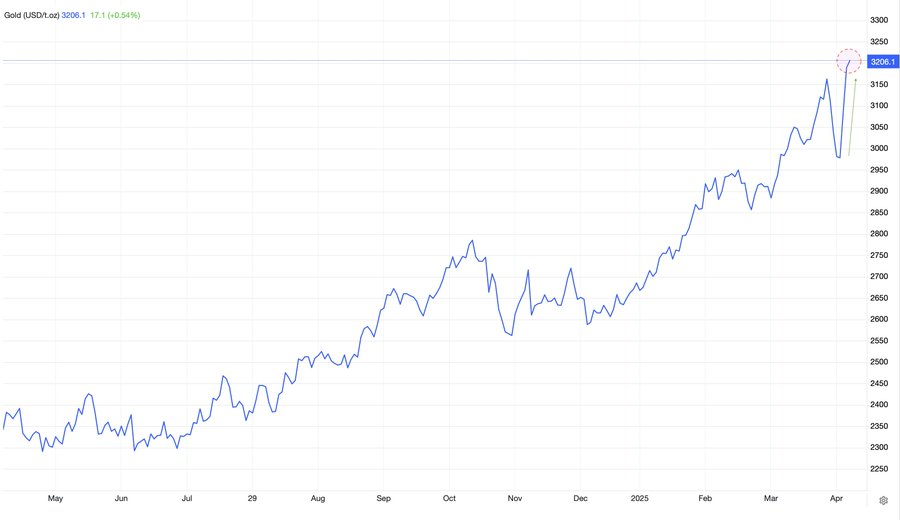

Пока мир штормит из-за очередного витка торговых пошлин, золото, как настоящий ветеран кризисов, снова показало отличную динамику. Его цена вылетела на новый исторический максимум — $3,200 за унцию. Те, кто заранее вложился в драгоценный металл, сейчас явно потирают руки — доходность улетела в космос.

На фоне паники на рынках активы-убежища, вроде золота, снова вошли в моду и пользуются бешеным спросом.

Авторитетный аналитик CryptoQuant Алекс Адлер младший подметил интересную деталь: биткоин начинает всё активнее примерять на себя роль «золота 2.0«. За год BTC подтянулся в цене на бодрые 16%, закрепляя за собой статус защиты от экономических катаклизмов.

По словам того же Адлера, основным триггером резкого скачка цен на золото стала свежая выходка США — очередное повышение тарифов на импорт из Китая. Новая планка пошлин — это какой-то ультимативный уровень: плюс 125% к действующим ставкам, что довело общий тариф до заоблачных 145%.

В то же время для других стран власти США включили режим «передышки» — дали 90-дневную отсрочку от новых пошлин. Но Китай оказался главным мишенью — рынки тут же отреагировали нервно.

Адлер считает, что усиление тарифной войны разогрело страхи инвесторов перед экономическим завалом. Особенно на фоне того, что доллар теряет свои позиции. Поэтому золото стало настоящим магнитом для капитала, спасаясь от будущих потрясений.

Золото всегда умело удерживать статус надёжного укрытия от инфляции и прочих финансовых напастей. С начала года цена на жёлтый металл выросла больше чем на 20% — не в последнюю очередь благодаря массовым закупкам со стороны иностранных центробанков.

Если торговая война будет только разрастаться, Адлер прогнозирует, что ценник на золото может ещё не раз удивить новыми высотами.

Пока весь мир следит за ростом цен на физическое золото, биткоин тоже показывает силу. За последний год крипта прибавила крепкие 16% — несмотря на общую турбулентность рынков.

На данный момент BTC немного подрос и торгуется в районе $81,910. Да, это всё ещё ниже исторического максимума в $109 тысяч, но динамика говорит сама за себя — инвесторы всё активнее добавляют его в свой набор защитных активов наряду с золотом.