Ethereum остается одной из ведущих криптовалют, но его инвестиционный потенциал вызывает споры. Сеть обладает мощной технологической базой, но также сталкивается с рядом проблем, которые могут повлиять на ее будущее.

Результаты Ethereum в 2024 году

Прошлый год для Ethereum был неоднозначным. Актив показал рост на 63%, но уступил другим криптовалютам: Bitcoin (+123%), Solana (+138%) и BNB (+134%). Еще хуже выглядела ситуация по сравнению с SUI (+555%), XRP (+335%) и Hedera (+300%). Ethereum и Hedera оказались единственными крупными проектами, не обновившими свой исторический максимум.

Проблемы начались после того, как несколько ключевых членов команды Ethereum присоединились к EigenLayer — проекту, работающему в экосистеме Ethereum. Дополнительные вопросы вызвал перевод $100 млн на Kraken, который породил сомнения в прозрачности работы фонда.

Ситуация усугубилась на фоне новостей о том, что Ethereum Foundation продает ETH каждые 11 дней, а также ухода ключевого разработчика Эрика Конора. Это усилило сомнения в долгосрочной стратегии платформы.

Мнение экспертов о будущем Ethereum

Мнения криптосообщества о перспективах Ethereum разделились.

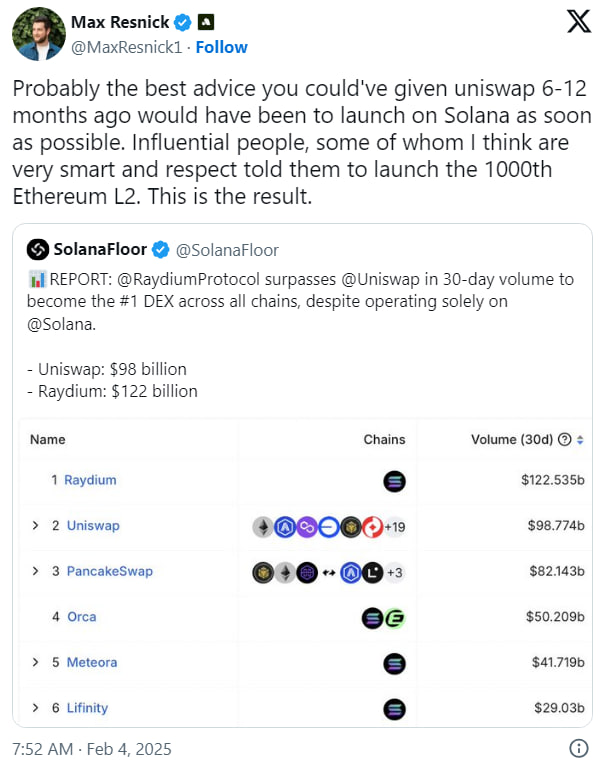

Макс Ресник, ведущий экономист Anza, раскритиковал стратегию Uniswap, заявив:

«Лучший совет, который могли дать Uniswap 6–12 месяцев назад, — как можно быстрее запуститься на Solana. Однако им рекомендовали запуск еще одного L2 на Ethereum.»

Антон Буков, сооснователь 1Inch, придерживается противоположного мнения:

«Несмотря на рыночную неопределенность вокруг крупнейших платформ для смарт-контрактов, я уверен, что Ethereum и его L2 остаются самыми популярными и удобными для разработчиков.»

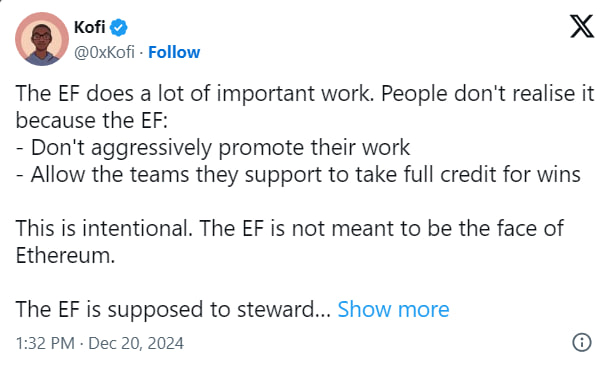

Аналитик Кофи считает, что Ethereum Foundation — это не сама сеть, а лишь одна из ее составляющих: По его мнению фонд выполняет очень важную работу. Люди этого не замечают, потому что:

- Он не продвигает свои достижения.

- Не заявляет о своих заслугах, а дает право командам, которым она оказывает поддержку, самостоятельно получать признание за их достижения.

Кофи считает, что это сделано намеренно и Ethereum Foundation не должен быть лицом Ethereum. Его задача — ухаживать за «бесконечным садом», поддерживая разнообразную сеть разработчиков в фоновом режиме, отметил аналитик.

Ключевые факторы для Ethereum в 2025 году

Развитие Layer-2 решений

Одна из самых ожидаемых инноваций Ethereum — развитие Layer-2. Эти технологии, включая Arbitrum, позволяют обрабатывать транзакции за пределами основного блокчейна, снижая нагрузку и уменьшая комиссии.

Высокие комиссии Ethereum долгое время оставались барьером для новых пользователей. Если L2-решения смогут изменить эту ситуацию, это повысит ценность сети и привлечет больше пользователей.

Перспективы Ethereum ETF

Еще одним важным фактором может стать одобрение спотового Ethereum ETF. Этот инструмент упростит доступ институциональных и розничных инвесторов к Ethereum, увеличив спрос и способствуя росту цены.

Одобрение Bitcoin ETF уже показало, что такие финансовые продукты могут кардинально изменить динамику рынка. Если Ethereum ETF получит зеленый свет, это станет мощным драйвером роста.

Стоит ли инвестировать в Ethereum в 2025 году?

С одной стороны, у проекта есть серьезный потенциал. Layer-2 решения, возможное одобрение ETF и масштабируемость могут усилить позиции сети. С другой, конкуренция растет, а внутренняя нестабильность подрывает доверие инвесторов.

Как подчеркнул аналитик Кофи, Ethereum это не просто фонд или команда разработчиков, а децентрализованная экосистема. Это дает проекту устойчивость, но не исключает рисков.