撰文:孟岩的区块链思考

7 月 27 日特朗普在纳什维尔比特币大会上 50 分钟的演讲,被誉为加密资产行业的又一个里程碑事件。但会后有人统计了一下,发现特朗普只字未提以太坊、区块链、Web3,唯一一次提到 Vitalik,后来还发现是听错了。

为什么特朗普不提 Web3 呢?确切的原因我当然也不知道,只能去问给特朗普写演讲稿的老兄,据说是《比特币杂志》的 CEO David Bailey。但是如果把这件事情放在整个 crypto 行业的大框架里来看,其实是不难理解的。

简而言之,特朗普的演讲基本体现了进步的比特币至上主义派的主张。

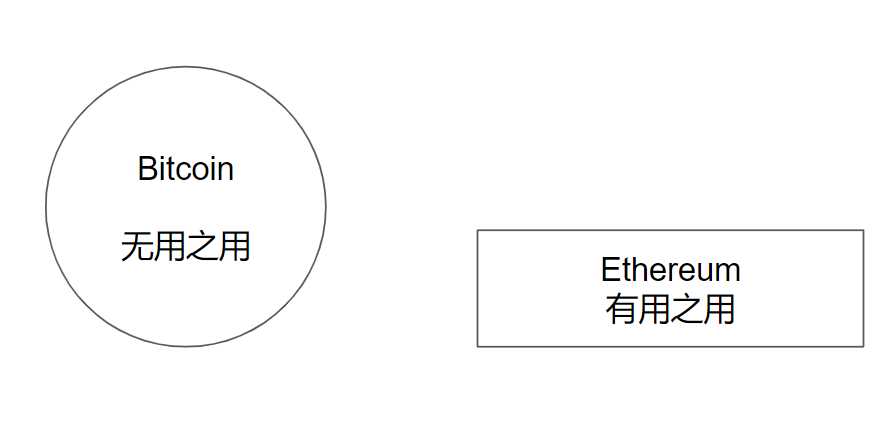

比特币和以太坊是 Crypto 行业遥遥领先的两个领头羊,经常被放在一起比较。但实际上两者截然不同,可以说代表着两个完全不同的思想门派:比特币是「无用之用」,以太坊是「有用之用」。

比特币的目标是作为数字黄金,数字世界利的价值标杆,除此之外别无它用,特别是没有任何使用价值。恰恰因为没有使用价值,因此你不能从效用的层面去分析它,不能用指标去衡量它的价值。因此比特币是不可战胜的,因为你想不到战胜它的逻辑。但另一方面,比特币没有给应用开发和生态建设留下什么空间,你很难在上面建造任何东西。有很多比特币的拥趸不断宣称,比特币是第一个也应该是最后一个区块链应用,比特币把区块链的合理价值全部发挥殆尽,区块链该做的比特币都做了,比特币没做的都是区块链不该做的,除了比特币之外的其他一切区块链创新全都是自作多情。这些观点正是原教旨的比特币至上主义的典型主张。这当然是对比特币的一种极致的推崇,但也是对于比特币无法作为基础设施支撑更大价值的屈服。

以太坊就不同,它的最初目标是做全球计算机,现在则是数字经济结算层,也是专用计算机,是一个有用的东西,从一开始就是作为一个生态基础设施出现的。这是以太坊的优势,但也是它的薄弱环节。既然有用,那么它的用处就可以基于一些指标来分解衡量,比如性能、TVL、用户数量、吞吐量等等。因为以太坊有用,所以理论上,如果你做出一个在各方面指标都超越以太坊的区块链,那就是一个更有用的区块链,就能打败以太坊。从 2017 年开始,出现了无数的 Ethereum Killer 的公链叙事,有些曾经一度获得很高的估值,其背后的逻辑就在于此。

所以可以这样比拟,比特币是一个大球,自身圆满,但是你在上面修不了上层建筑。以太坊是一块平板,给你修建上层建筑提供了良好的基础条件,但是它本身比比特币要脆弱。

川普这次演讲,虽然讲了很多,但其实只是围绕华尔街的比特币逻辑反复螺旋式增强,也就是认可比特币数字黄金的价值,对其价值表达信心,提供当选后的政策保证,一浪高过一浪,但是也仅此而已,并没有涉及到其他方面,完全没有涉及到区块链在改变互联网应用范式方面的话题。

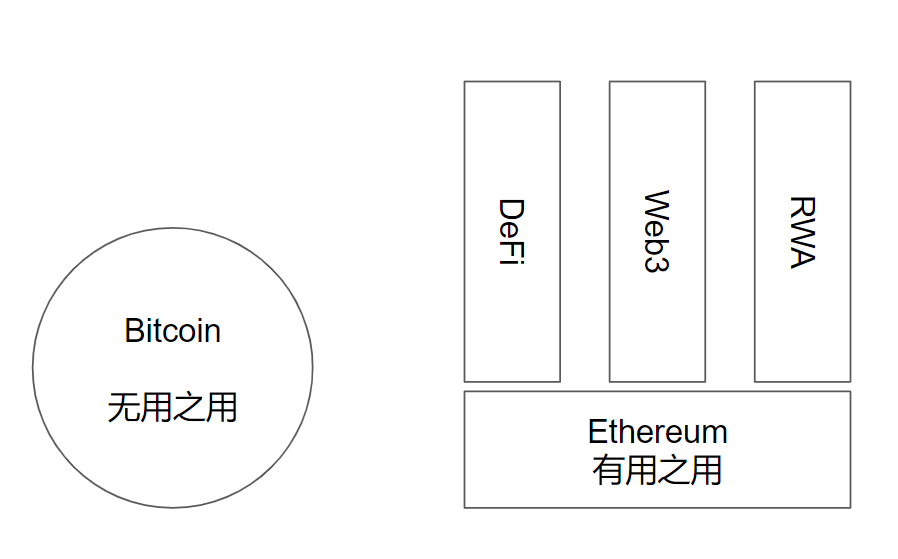

比特币跟以太坊提供了不同的承诺,比特币是站稳数字黄金的位置,不断提高市值。而以太坊是打下基础,为 DeFi、Web3、RWA 等应用提供支撑。

我觉得特朗普对这个行业的了解不可能这么具体,因此他的演讲里主要体现的还是《比特币杂志》这帮人的长期一贯立场,就是我们终于把比特币这种资产确立为主流合规资产了,现在可以在主流金融圈围绕这种新资产,把各种可做的业务和衍生品都来上这么一遍。过去黄金有的,现在都给比特币加上。华尔街是比较喜欢这样的叙事的。只要客户喜欢交易,就有佣金可以赚。

相反创造新的技术、工具、平台、应用范式,这是硅谷喜欢干的事儿。所以像在以太坊上创建 DeFi、Web3、RWA 或者产业区块链这些事情,我们不能指望华尔街特别积极,还是得先干出一些名堂来,然后华尔街才会加入进来。

当然这并不是说特朗普的这些表态,如果真的落实的话,对 DeFi、Web3、RWA 这些方面就没有意义。意义还是很大的。首先是大量资金涌入数字资产的话,本身也会波及到这些上层建筑领域。另一方面,特朗普说要给 SEC 换人这个点非常耐人寻味。因为詹斯勒这个家伙虽然招人恨,但是实话实说,人家任内对于比特币是基本还是开绿灯的,没有过多为难。如果说只是站在比特币的立场上看詹斯勒,就算不是高分,也非常及格。詹斯勒真正的保守是体现在对待以太坊生态、特别是 Web3 的极力阻挠之上,特别是在 Hester Peirce 的《通证避风港》提案都已经起草出来的情况下,长期束之高阁,严重阻碍了 Web3 的发展。所以换詹斯勒这个事情实际上对于比特币意义不大,但可能是利好 Web3 的。

如果美国想要变成 Web3 的福地,SEC 而不是华尔街的态度更关键。只有允许 Web3 项目以自然合理的方式应用 token 进行用户激励和治理,同时实施有效监管,坚决打击发币割韭菜的镰刀们和欺诈者,Web3 才能获得一个较长的发育周期,实际长出业务飞轮。唯有如此这个行业才能真正摆脱大起大落的循环。

我不知道特朗普在这个问题上认识有多深,但看上去贺锦丽应该不会往这个方向前进,越是自认为代表历史前进方向的人,侵犯个人自由和权利的时候越无所顾忌。所以这次美国大选确实是关乎 Web3 行业利害的,且让我们拭目以待吧。