最近Curve创始人套现行为和持续的抵押CRV借出稳定币的行为在市场流动性受SEC事件影响时成为备受市场关注的焦点。为了分析CRV的链上做空成本,可能性以及相关影响,先回顾一下在去年的CRV多空大战中,看看过去的做空操作是如何进行的

去年FTX暴雷后不久,市场缺乏信心流动性极度萎缩时,一名巨鲸从Aave借出了大量CRV代币,转移到OKX交易所,总计借出了4700万CRV,受到巨鲸的砸盘做空影响,CRV价格从0.545美元下跌至0.424美元,跌幅达21.88%,最低达到0.4美元,这种操作为通过链上反复借贷并转移代币,以打压币价进行大规模做空。

随后创始人Michael创始人购买CRV来抬高币价,尽管Aave账户承担清算风险,但空头仍有获利潜力。一种获利方法是在OKX等交易所进行高杠杆空头交易,利用市场流动性不足且缺乏强劲多头干扰的情况下获取高概率的盈利机会。另一种获利方法是将空头仓位转为多头仓位。当市场流动性被耗尽时空头平仓转而做多

Aave在CRV多空博弈事件后取消了CRV借出(即无法通过同样的链上循环贷不断增加杠杆进行做空)。目前在Fraxlend中CRV仅有20mln borrowing ceiling, 借出利率为20%,池子的利用率很高(99%)且目前只有少量CRV可借; 即链上整体可借数量不足以支撑类似去年的链上借循环贷的做空行为

此外,中心化交易所也提供了借币做空的机会。当前,CRV代币的筹码分布如下:Curve dex中持有1.16亿,币安持有6547万,OKX持有1256万,其他中心化交易所共计5329万。可以看出,中心化交易所持有大量的CRV代币,占据了流通总量的15%。但由于缺少中心化交易所数据无法计算可能的做空行为成本。

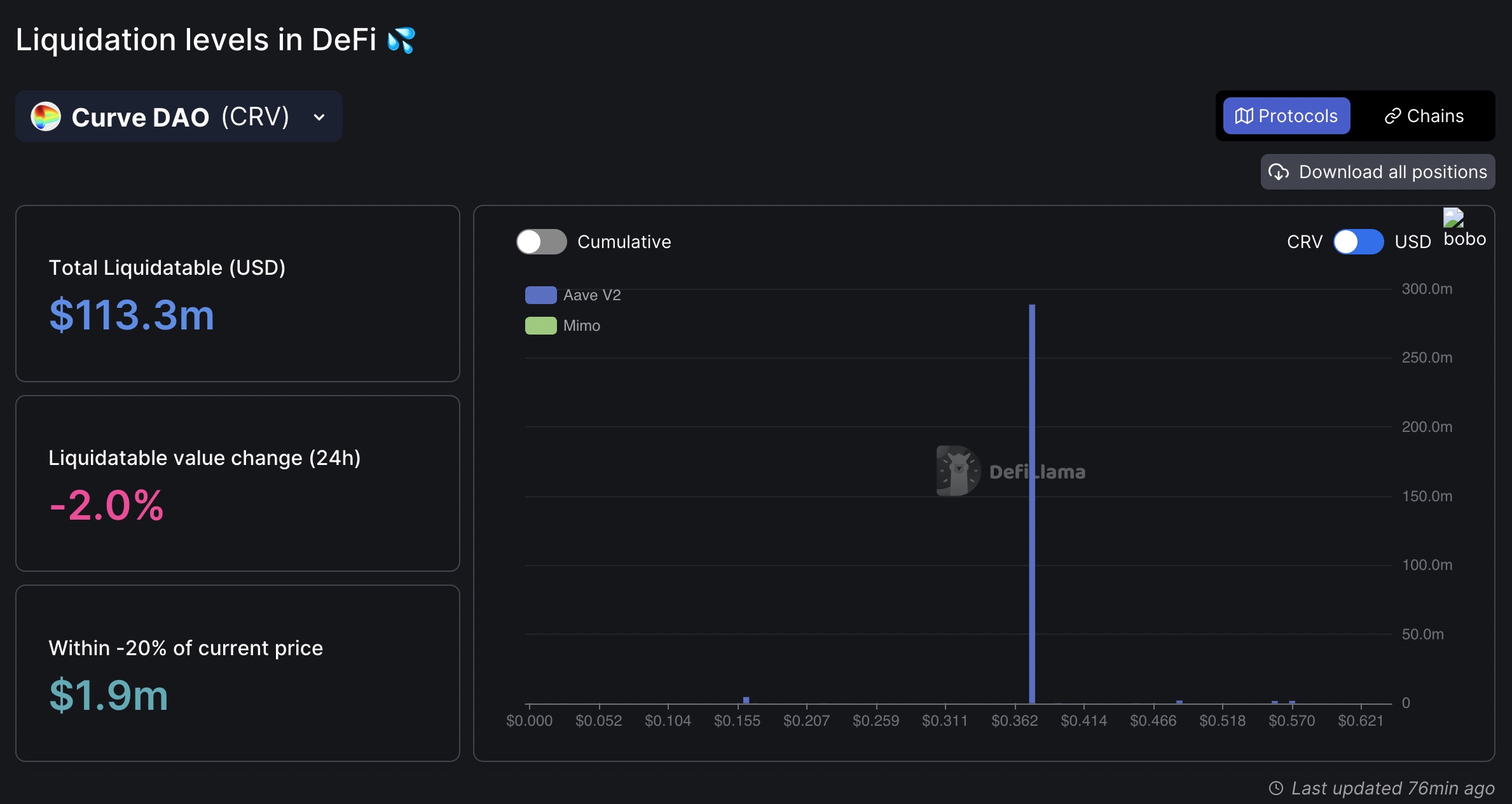

目前来看,CRV的总链上可清算金额为1.13亿美元,其中99%(2.89亿CRV)集中在0.375美元的价格附近。这意味着,借币做空可能会足够将价格压到清算价格附近,但Curve创始人有能力添加保证金让清算价格继续下移,单纯做空成本会非常高。