Recent Interest Rate Hikes Temporary

Interest rates in advanced economies are likely to fall to pre-pandemic levels when authorities succeed in bringing inflation back under control, the latest International Monetary Fund (IMF) blog post has suggested. The blog post added that the “recent increases in real interest rates are likely to be temporary.”

The return of real interest rates to levels seen before the spread of Covid-19 will also coincide with the easing of the respective countries’ monetary policy regimes. As has been reported by Bitcoin.com News, central banks from advanced economies have raised benchmark rates as they seek to tame inflation. The rising interest rates have sparked fears that the global economy may be headed for a recession.

However, in their April 10 blog post, the authors claimed a transition to a green economy may potentially lead to lower real interest rates globally:

Transitioning to a cleaner economy in a budget-neutral way would tend to push global natural rates lower in the medium term, as higher energy prices (reflecting a combination of taxes and regulations) would bring down the marginal productivity of capital. However, deficit-financing of public investment in green infrastructure and subsidies could potentially offset and even reverse this result.

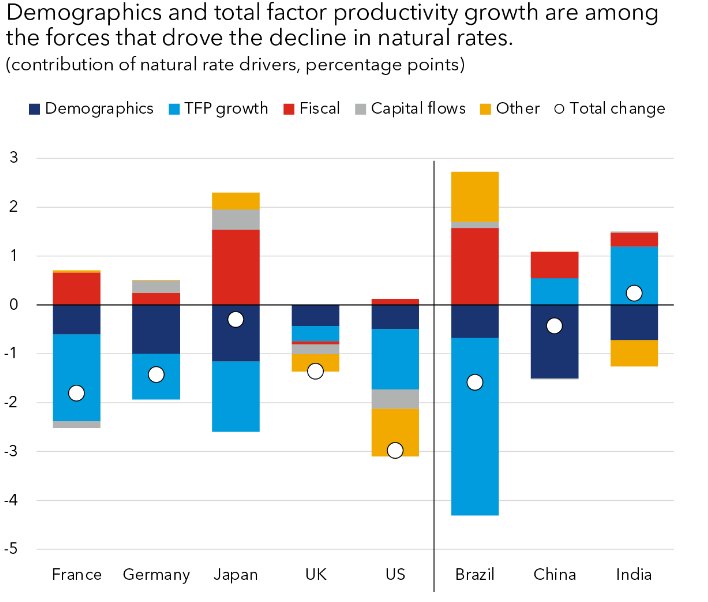

The authors also suggested that so-called deglobalization forces could intensify and this may result in both “trade and financial fragmentation.” According to the authors, this outcome is likely to result in driving up the natural rate in advanced economies and down in emerging markets economies.