Editor's Note: DeFi is once again approaching its historical high but has failed to break through significantly, revealing not a lack of products but a bottleneck in user growth. The expansion of stablecoins, yield-bearing stablecoins, and RWA indicates that the demand for moving funds on-chain and earning yields remains strong, yet it has not been truly brought to the mass market.

This article argues that the next step for DeFi lies not in more complex structures or speculative designs, but in simple, secure, yield-focused products, along with user-friendly access and distribution methods for ordinary users. Only when DeFi begins to target fintech users, rather than solely serving crypto-native audiences, can a new growth cycle truly begin.

Below is the original text:

Current Situation

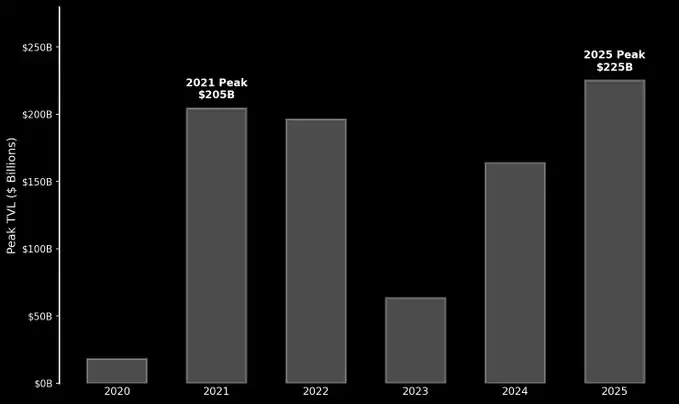

In 2025, DeFi's total value locked (TVL) reached a new historical high, but it did not significantly exceed the peak of 2021. As the market gradually cools, a question worth revisiting is: where will the next wave of capital and users come from?

Driven by DeFi Summer, TVL climbed to $204 billion by the end of 2021. Subsequently, following the collapse of events like FTX and the market entering a bear phase, the capital scale declined steadily. Later, DeFi struggled to recover, reaching $225 billion in October 2025. However, a mere 10% growth over four years can hardly be considered explosive. The earliest participants in DeFi—primarily crypto-native users and traders—may have nearly reached the "ceiling."

The proximity of these two peaks is indeed cause for caution, but it does not yet constitute a "survival crisis." The current user base—though highly engaged and loyal—is not large enough to propel DeFi to the next level on its own.

To achieve a breakthrough, DeFi needs to reach a larger audience. The good news is that such an audience does exist—it is still on the sidelines, waiting to be properly "onboarded" with the right tools and products.

A Glimmer of Hope

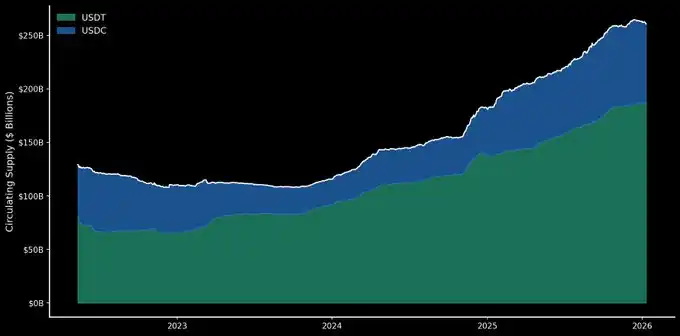

Over the past year, the stablecoin market has been one of the biggest beneficiaries. The amount of USD on-chain has reached a historical high, more than ever before. USDT and USDC have continued to grow steadily, with their combined market capitalization exceeding $260 billion—meaning that the scale of stablecoins alone is already larger than the entire DeFi market.

Even without parabolic growth in DeFi, people continue to mint stablecoins, indicating that the demand for moving funds on-chain remains strong. At the same time, an increasing number of users are beginning to access the yields provided by DeFi, and the growth in this area points to where the next breakthrough may come from.

The rise of yield-bearing stablecoins and RWA (real-world assets) further confirms this trend. According to @stablewatchHQ data, the scale of yield-bearing stablecoins has exceeded $20 billion, with products like sUSDS and sUSDe gaining significant adoption over the past year or so. Parallel to yield-bearing stablecoins, RWA has also made progress on-chain: these products, backed by traditional assets such as treasury bonds, offer real yields and are growing rapidly.

The problem is that they currently primarily cater to crypto-native users and large on-chain holders. As long as this remains the case, their potential will be underestimated. If they can be productized and packaged in a way that is more accessible to everyday users, yield-bearing stablecoins and RWA present enormous opportunities in the mass market.

Retail Has Not Yet Arrived

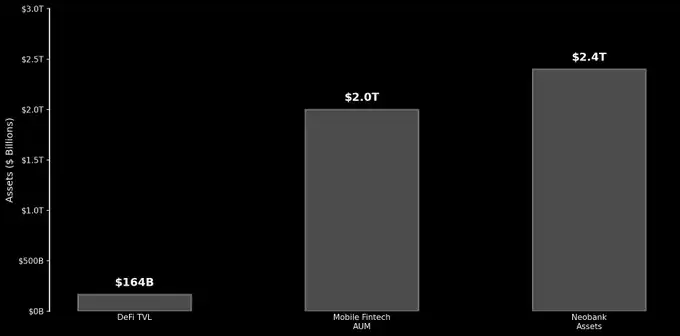

To understand the scale of this opportunity, it is helpful to compare DeFi with fintech. Currently, the entire DeFi TVL is approximately $164 billion. In contrast, global mobile fintech apps manage over $2 trillion in customer assets; the top 100 neobanks alone have assets totaling $2.4 trillion. By comparison, DeFi is currently almost a negligible fraction.

The notion that "if you build it, they will come" can only drive limited growth. If DeFi wants to continue expanding, it must compete for the ordinary users that have made fintech so vast.

In 2025, the success of protocols like Aave, Ethena, and Pendle has demonstrated a strong demand for yield among market participants. They were the highlights of the year, attracting significant capital and attention. If such products can be delivered to the masses in a clear, understandable, and low-barrier manner, the potential encompasses (literally) trillions of dollars in capital and tens of millions of potential users.

The Path Forward

The real test for DeFi in the coming year is whether it can make yield opportunities easily and safely accessible to ordinary people. Growth will not come from more complex financial structures, the 100th liquidity mining pool, the 100th perpetual futures DEX, or the millionth airdrop. Growth will come from simple, reliable products—built on decentralized protocols—that solve real problems for ordinary people. And yield should be center stage (ahem, Aave App, ahem).

Today, hundreds of millions of people use banking and fintech apps daily, already accustomed to managing their funds on their phones. If DeFi can capture even a small share of this, it will be enough to trigger a new wave of growth, and it will not once again stall at the $200 billion TVL level.

Embedded DeFi will play a crucial role in this—fintech companies and neobanks integrating on-chain yield capabilities directly into their products. But teams should not stop there. The protocols that are truly consumer-facing and at the forefront will capture the greatest upside; those that continue to optimize only for crypto-native users will ultimately be competing for a pie that may no longer be expanding.

DeFi will win.