Author: Zhao Ying

Source: Wall Street News

The commercialization of AI applications is extending from selling software and memberships to selling token-calling capabilities. Here, Tokens refer to the smallest units of information processed by large models, serving as the basis for API billing, settlement, and consumption. As the volume of calls increases, Tokens themselves are beginning to be procured, routed, split, and resold like a form of "inventory."

Chen Liangdong, an analyst at Huayuan Securities, summarized the core change in a recent media industry report: "Token operations are forming a new intermediary market, which involves exploring token distribution models to connect upstream large model providers with downstream developers, enterprises, and individuals. The essence is the liquidity infrastructure for a global network of token wholesale to retail."

The background for this business is not complex: On one hand, China's daily token call volume has surged rapidly, rising from 100 billion tokens per day at the beginning of 2024 to 100 trillion by the end of 2025, surpassing 140 trillion by March 2026. On the other hand, domestic large models have improved significantly, entering the global top tier in certain rankings and call volumes. With increasing demand and a growing number of models, the real barriers to transactions have become payment, network access, interfaces, compliance, distribution channels, and scenario implementation.

However, token distribution cannot be simply understood as "reselling API quotas." The thinnest layer of profit comes from resale margins, while the thicker portion comes from inference acceleration, unified interfaces, enterprise-level prompt engineering, Agent orchestration, model selection, and integration with business systems. Precisely because the entry barrier is not high, the risks in this market are equally direct: intensified competition, funding requirements for upfront payments, bad debts, and policy changes from upstream model providers can all squeeze the profits of the intermediary layer.

Tokens Now Have "Wholesalers" and "Retailers"

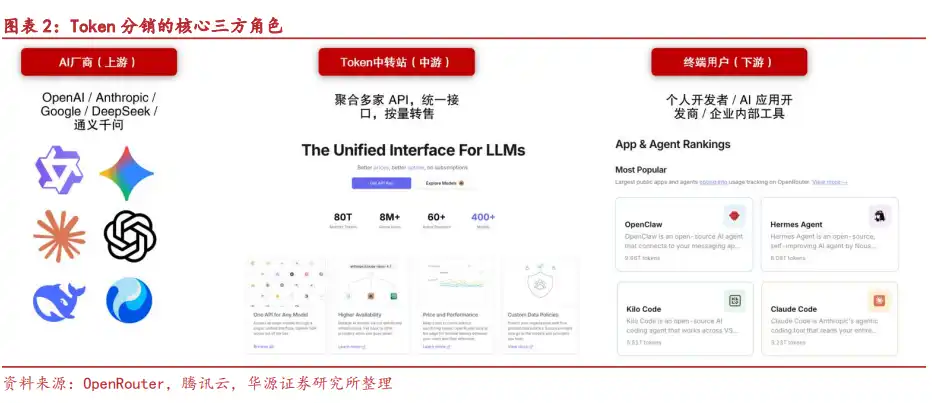

The basic chain of token distribution includes three types of roles.

Upstream are the model providers, including ByteDance's Seedance series, Alibaba's Qwen series, Zhipu's GLM series, Moonshot AI's Kimi series, DeepSeek series, etc. They are the original suppliers of tokens.

In the middle are agency platforms responsible for procuring resources from upstream model providers and distributing them to end-users. Their work is not just about reselling quotas; they also convert the interface protocols of different models into a unified API format, enabling downstream users to access multiple models through a single API Key.

Downstream are the actual consumers of tokens, including individual users, developers, enterprise clients, and possibly lower-tier distributors.

The value of this intermediary layer focuses on several areas: reducing network barriers through domestic direct connections; enabling a single codebase to adapt to multiple models; supporting both personal and corporate payments; potentially obtaining lower costs through bulk procurement; and aggregating models like GPT, Claude, DeepSeek, and Kimi on one platform to reduce the cost of repeated integration for developers.

Thus, token distribution appears to be asset-light, requiring neither the training of large models nor massive server clusters. The core assets become the API routing and scheduling system, upstream model resources, channel clients, and service capabilities.

The Surge in Call Volume is the Most Direct Fuel for This Business

For the token operation model to succeed, there must first be a sufficiently large consumption volume.

China's daily token call volume increased more than a thousandfold in two years, from 100 billion to over 140 trillion tokens. This expansion stems from the deployment of various vertical Agents and the embedding of generative AI into more business processes by enterprises.

IDC data presents an even more aggressive trajectory: the number of active intelligent agents in Chinese enterprises is expected to exceed 350 million by 2031, with a compound annual growth rate (CAGR) exceeding 135%. As the density and complexity of agent tasks increase, the annual growth rate in token consumption by agents is projected to exceed 30-fold.

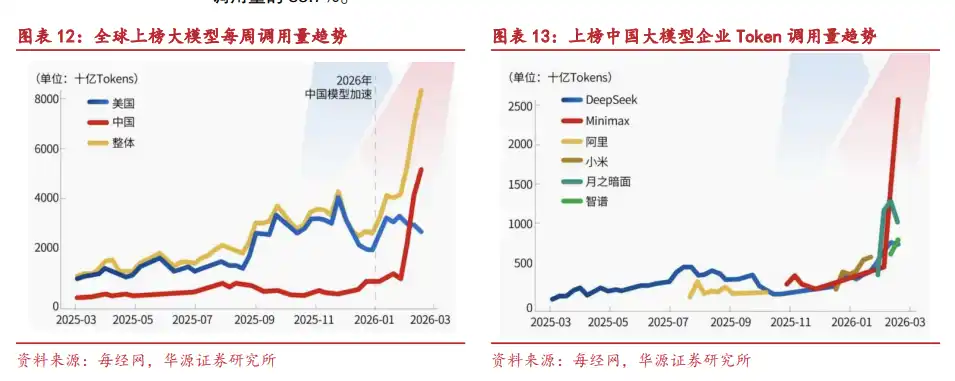

This change is already visible in execution-oriented agents. The weekly token consumption of OpenClaw on the OpenRouter platform increased from 0.81T between February 2 and March 16, 2026, to 4.97T, with its share rising from 8.31% to 24.36%.

Once tokens become a mass-consumed commodity, their procurement, pricing, routing, and settlement naturally stratify. Model providers may not directly serve every client, and end customers may not be willing to integrate with each model individually, creating space for the intermediary layer.

The Cost-Effectiveness of Domestic Models Opens the Door for Token Export

The improvement in domestic large model capabilities is a key variable enabling token distribution to expand from domestic to cross-border markets.

Data from SuperCLUE shows that domestic models like ByteDance's Doubao and the DeepSeek series have achieved overall scores exceeding 70 points, narrowing the gap with leading overseas models like GPT-5.4 and Gemini. Models like Tongyi Qianwen, Kimi, and Zhipu GLM have also formed a relatively clear tiered structure.

According to OpenRouter data, for the week ending May 10, 2026, Tencent's Hy3 preview (free) topped the call volume list. Among the top 5, top 10, and top 20 models, there were 2, 6, and 9 domestic large models, respectively.

A more significant change occurred in Q1 2026. From February 9 to 15, the call volume of Chinese models on OpenRouter reached 4.12 trillion tokens, surpassing the 2.94 trillion tokens of US models for the first time in the same period. From February 16 to 22, the weekly call volume of Chinese models further increased to 5.16 trillion tokens. Among the top five models on the platform by call volume, four were from Chinese providers: MiniMax M2.5, Kimi K2.5, Zhipu GLM-5, and DeepSeek V3.2, collectively accounting for 85.7% of the total call volume of the top five.

The price advantage is also prominent. The input price for both MiniMax M2.5 and GLM-5 is $0.3 per million tokens, compared to $5 for Claude Opus 4.6. For output, MiniMax M2.5 is $1.1, GLM-5 is $2.55, and Claude Opus 4.6 is $25. The cost-effectiveness of domestic models becomes more pronounced in high-token-consumption scenarios like AI Agents and code development.

Global AI Resource Imbalance Makes Routing Platforms the "Transit Hubs"

Token distribution doesn't just solve price issues; it also addresses resource mismatches.

Leading overseas large models face barriers like regional access restrictions, compliance rules, and payment hurdles, preventing them from directly reaching certain user groups, including developers in mainland China. Similarly, high-quality domestic models expanding overseas encounter challenges in localization, channel development, and user acquisition.

This imbalance fuels the demand for cross-border flow, aggregated routing, and layered distribution.

OpenRouter is already a typical example. The volume of tokens processed on its platform increased from 5-7 trillion per week in 2025 to over 20 trillion per week by April 2026. Its annualized revenue in 2026 exceeded $50 million, a roughly fivefold increase from the over $10 million annualized revenue disclosed in October 2025.

Similar platforms exist domestically. Silicon Flow is a one-stop large model cloud service platform based on its self-developed inference engine for efficient inference acceleration, while also providing enterprise-grade large model services. As of December 2025, the platform had over 9 million registered users, more than 10,000 enterprise users, and over 150 models available.

Even politically connected capital in the US has entered this field. On May 5, 2026, WLFI, a cryptocurrency company closely linked to Trump and his family, partnered with WorldClaw to launch WorldRouter, integrating over 300 models including Claude, GPT, and Gemini. Settled in USD, its pricing is approximately 30% lower than official public rates.

Real Profits May Not Lie in "Resale Margins"

There are three ways to profit from token distribution.

The first is resale margins. Platforms purchase API quotas in bulk from upstream model providers and resell them at a markup to downstream clients. OpenRouter, which adds about a 5.5% premium to supplier costs, exemplifies this model.

The second is technological premium. Platforms use self-developed inference acceleration engines to reduce the cost per token. Even when selling at prices close to or lower than official rates, they can generate gross profit through computational efficiency advantages. Silicon Flow's SiliconLLM and OneDiff technologies improve language model inference speeds by 10 times and text-to-image efficiency by 3 times, reducing the cost of large model API calls to as low as 1/10th of the industry average.

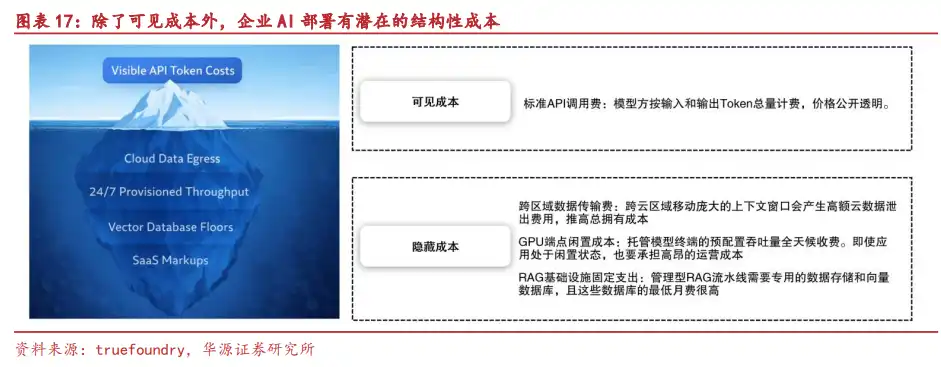

The third is enterprise value-added services. The cost of deploying AI for enterprises isn't just in token unit prices; it also includes prompt engineering, multi-model selection, business system integration, workflow orchestration, operational scheduling, and employee AI skills development. As basic token prices decline, these hidden costs become more likely points for monetization.

Silicon Flow's enterprise-level MaaS platform follows this direction: providing enterprise users with capabilities across three layers—model training and fine-tuning, deployment and inference, and application development support—covering data processing, model fine-tuning, prompt engineering, and RAG, ultimately delivered in the form of standardized APIs to industries like energy, finance, and government.

Marketing, Short Videos, Gaming, and E-commerce Are Scenarios That Consume Tokens More Easily

To be profitable, token distribution must ultimately land in real-world scenarios.

Generative AI applications are entering industries like healthcare, transportation, and industrial manufacturing and are starting to participate in core processes like corporate decision support and strategic management. However, many enterprises have weak foundations for digital transformation, insufficient data asset accumulation, and limited computing power investment, making direct AI deployment challenging.

In contrast, marketing and advertising companies already possess clients and scenarios, especially in short videos, webtoons, gaming, and e-commerce. Their token consumption demand is more direct and sustained. For such companies, the opportunity isn't just about reselling model capabilities but embedding tokens into client workflows for content generation, ad placement, asset production, and video creation.

Investment leads also unfold along two main lines:

One category includes companies with strong model capabilities, such as Alibaba, Tencent Holdings, Kuaishou, Kunlun Tech, Zhipu, MiniMax, etc.

The other category includes companies with strong token consumption scenarios and quality client sources, especially those with overseas client resources and marketing scenarios, and a willingness to actively invest in AI marketing and AI videoization. Examples include EasyClick and BlueFocus.

Risks Are Also Concrete: Low Barriers, Upfront Funding Requirements, Upstream Dependence

The token distribution business model is asset-light, but its moat is not inherently deep.

Peer competition is the first risk. The technical barrier for distribution is relatively low. Once leading distributors with capital, client, and channel advantages enter, they can quickly replicate the model, compressing profit margins.

Upfront funding requirements and bad debts are the second risk. Distributors often offer monthly or quarterly settlements to downstream clients but need to fund the upfront purchase of API quotas from upstream providers. The larger the token consumption scale, the greater the funding pressure. If clients delay payment, bad debt risks amplify simultaneously.

Policy changes by upstream model providers are the third risk. Large model providers control API pricing and access rules and may adjust prices or tighten policies for third-party access. For the intermediary layer, this is the most difficult factor to control.