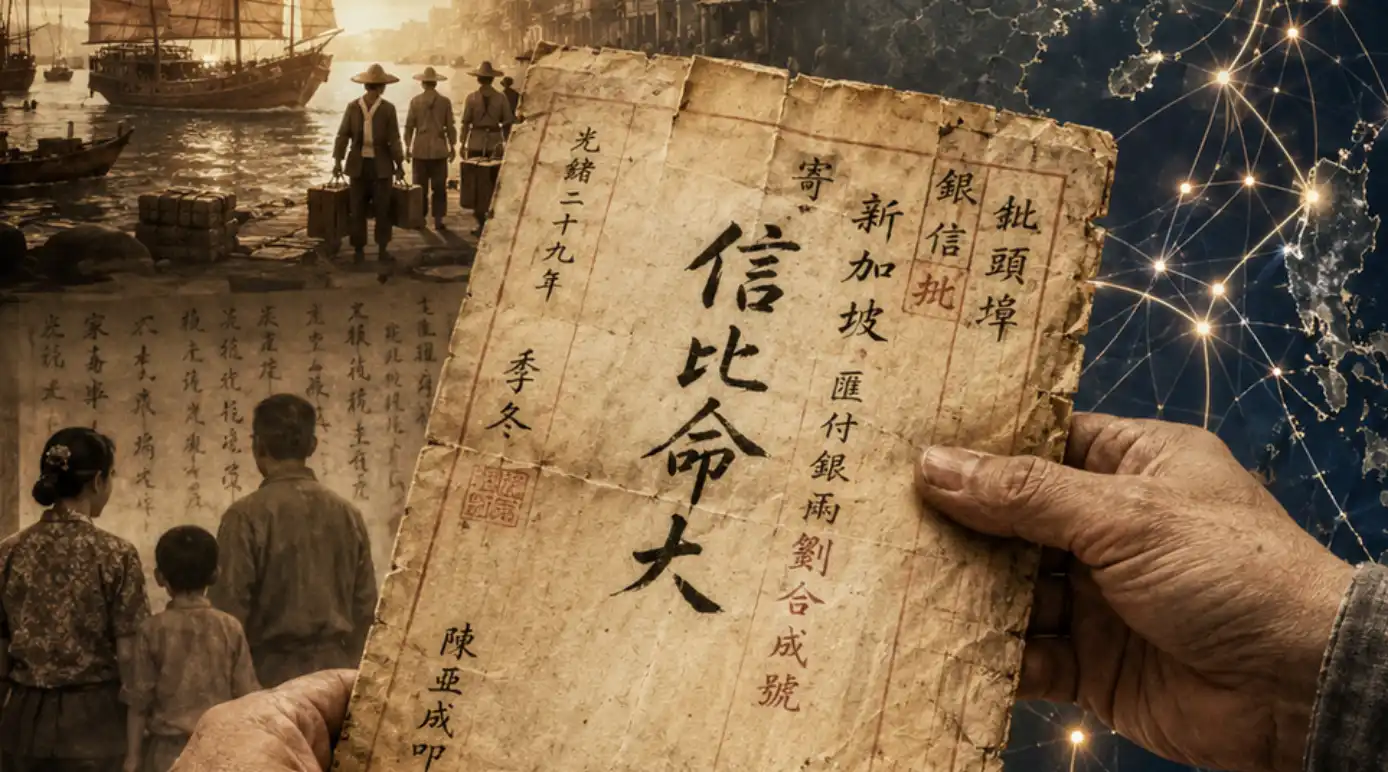

A Century Before Swift and Blockchain, China Built Its Own Cross-Border Financial Network

A century before Swift and blockchain, China's cross-border financial miracle: The Qiaopi Network.

Driven by the phrase "a promise is greater than life," the Qiaopi (overseas Chinese remittance letter) system was a remarkable, entirely private financial network. Operating for over a hundred years until 1979, it facilitated billions in remittances, at one point constituting over 50% of China's foreign exchange during WWII—all without central banks, official clearing, or government backing.

It began with "Shuike" (water guests), couriers who carried cash and letters personally between Southeast Asia and Chinese villages like Chaozhou. Their operation was peer-to-peer, identity-verified through kinship, and had a near-zero default rate, as trust was their sole collateral. This evolved into "Piju" (remittance houses), creating an institutional network. They ingeniously used currencies like the Hong Kong Dollar for settlement and practiced netting clearance, offsetting remittance flows against trade payments to minimize physical cash movement.

Its resilience shone in wartime. When Japanese forces cut off main routes, the network forged an underground "Dongxing Remittance Path" through Vietnam. It used coded messages ("a bag of rice" for a sum of silver) to evade interception, reliably delivering funds critical for survival and even clandestine support for the war effort.

Unlike Swift (built on state cooperation) or blockchain (relying on cryptography), Qiaopi was founded on clan,乡土 (native place), and human trust—a cultural consensus where违约 meant social death. Modern finance compensates for this lost trust with complex collateral and regulation. The Qiaopi network, powered only by sailing ships, familiar accents, and profound integrity, achieved a feat of decentralized, cross-border finance that remains unparalleled—a poignant story of信用 (trust/credit) in its purest form.

marsbit05/15 04:04