In the past, the closure of traditional financial markets typically meant a suspension of price discovery. Assets such as stocks, commodities, and ETFs would enter a silent state after Friday's close, and investors had to wait until the next trading day's opening to see the real impact of events reflected in prices.

However, the on-chain derivatives market, spearheaded by Hyperliquid, is changing this structure.

With Hyperliquid HIP-3 allowing external builders to deploy RWA perpetual contracts for stocks, commodities, indices, and more, certain traditional assets, represented by the XYZ market, can now achieve 24/7 continuous trading on-chain. When traditional markets are closed, the on-chain market does not halt matching; instead, it can become a front-running venue for risk expression and price discovery.

The recent weekend price action of the Korean chipmaker SK Hynix (SK Hynix) on-chain provides a clear observation sample. Hyperliquid xyz:SKHX was not just experiencing sporadic trades during the KRX closure. According to 1m K-line data from candleSnapshot, substantial volume exchanges between longs and shorts occurred over the weekend.

By June 8th, Monday, just before the official KRX market open, the on-chain market had already charted a complete weekend price path.

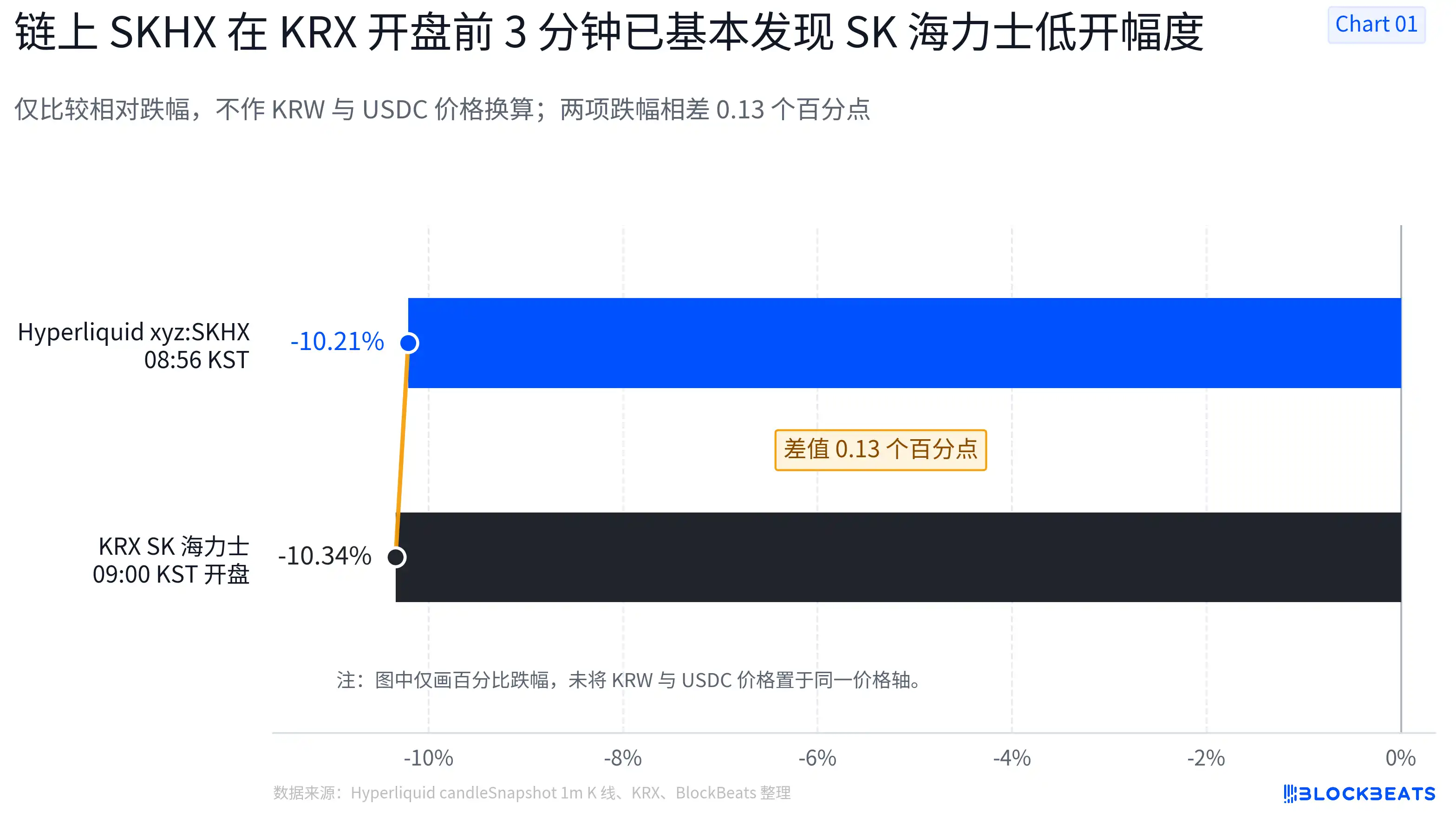

Accuracy Within 0.13%: SK Hynix's Weekend Price Discovery

On June 5th, SK Hynix's stock on KRX closed at 2,070,000 KRW. Subsequently, the Korean stock market entered its weekend closure.

According to 1-minute K-line data from Hyperliquid, its base price on-chain remained at 1336.5 USDC after Friday's close. On Monday morning, just before the KRX open, significant price fluctuations occurred on-chain:

· Monday 08:56 KST (Korean Standard Time): xyz:SKHX dropped to a low of 1200.0 USDC, corresponding to a decline of -10.21%.

Three minutes later, the traditional world's KRX officially opened, with the real-world data as follows:

· Monday KRX Official Opening: 1,856,000 KRW, corresponding to a decline of -10.34%.

The difference between the two was only 0.13 percentage points.

This means that just 3 minutes before the KRX official open, the funds in the on-chain market had almost completely discovered the extent of SK Hynix's lower open on Monday. It didn't vaguely express the direction of "will fall," but precisely priced the decline around 10%, aligning closely with the actual opening result.

A Critical Reversal: Not a Failed Prediction, But Front-Running the Post-Open Trend

The market then entered a second phase of change, concentrated in the final 120 seconds before the open.

During the period from 08:58 to 08:59 KST, xyz:SKHX experienced unusual volume surges:

· 08:58: Minute trading volume rose to 708.132, placing it at the 99.85th percentile of the entire weekend's minute-by-minute volume;

· 08:59: Volume remained high at 665.584 (99.82nd percentile), and the price rebounded from 1201.1 USDC to 1228.8 USDC, a +2.31% bounce within two minutes.

If looking only at the final price at 08:59, the on-chain price was about 2 percentage points higher than the subsequent actual KRX opening price. However, this does not indicate a failure of on-chain price discovery. A more reasonable explanation is that the on-chain market had already front-run the low-price buying that would occur immediately after the stock's opening.

Looking at the actual post-open movement on KRX:

· KRX opened and probed a low of 1,855,000 KRW;

· 09:03 KST: The stock price had already recovered to 1,904,000 KRW, rebounding approximately +2.64%.