Author: Pantera Capital

Compilation: Jiahuan, ChainCatcher

Perpetual futures (or "perpetual contracts") are gradually becoming one of the dominant trading instruments in global financial markets. They are evolving from a crypto-native phenomenon into a fundamental shift in market structure that traditional investors can no longer ignore.

This concept is not new. Today, the infrastructure supporting it has caught up, especially in the on-chain realm of decentralized finance. And just last week, with a series of actions taken by the U.S. Commodity Futures Trading Commission (CFTC), the U.S. regulatory system has begun to formally accept it.

Advantages of Perpetual Contracts

The first formal futures market was the Dojima Rice Exchange established in 1730, aimed at helping Japanese rice farmers hedge against crop price risks. External speculators realized they could use margin and leverage to trade these contracts, making directional bets on rice prices without needing to physically deliver rice (cash settlement).

Capitalism, as always, played its role. Today, futures cover all major asset classes (commodities, foreign exchange, equities), and most futures trading is related to leveraged, directional betting.

A perpetual contract is a futures contract that never expires. Instead of setting an expiration date, it uses a funding rate: a small fee paid periodically (e.g., every hour, or every 8 hours as is most common on crypto exchanges) between longs and shorts.

When the perpetual contract price is too high relative to the spot price, longs pay fees to shorts; when the price is too low, shorts pay fees to longs. Basis arbitrageurs step in to anchor the contract price to the spot price.

The absence of an expiration date might sound like a simple design choice, but it offers significant benefits compared to existing derivatives (such as periodic futures and options): easier to manage from an execution standpoint, easier to understand from a risk perspective, and natively supporting 24/7 trading.

From an execution perspective, perpetual contracts require less management than traditional futures. Traditional futures have expiration dates (e.g., monthly), which is why they are often called "periodic futures."

To hold a position over a longer period, traders must continuously roll over from one contract to the next, sometimes managing a series of contracts with different expiration dates, each with its own basis between futures and spot prices.

Perpetual contracts simplify this complexity into a single continuous position with no expiration date, thus eliminating the need for rollovers. Traders can hold for seconds, or theoretically forever, without worrying about trade management.

From a risk management perspective, perpetual contracts are also easier to understand than other derivatives. Periodic futures require a view on a specific timeframe. With options that also have specific expirations, a trader might be correct in direction but still lose money due to time decay or changes in implied volatility.

Perpetual contracts strip away these complexities, allowing traders to express conviction more directly, almost entirely (though not completely) based on price.

Perpetual contracts also never stop; they trade around the clock, with no market hours restrictions or weekend closures. This generation of internet-native users lives in a globally connected, always-on economy. For them, continuous access is not an add-on feature but a default expectation.

Driven by these market demands, traditional exchanges are already moving in this direction. Extrapolating the current trend, perpetual contracts seem a natural progression.

Given their origins, periodic futures feel somewhat outdated. For the directional leveraged exposure most participants want, perpetual contracts are a more natural instrument, offering all the aforementioned advantages.

Digital Assets Laid the Groundwork for Perpetual Contracts

The design of perpetual contracts is not new, dating back to a 1993 paper by Nobel laureate Robert Shiller. However, the existing market structure of traditional exchanges created too much friction for them to gain popularity.

The digital asset industry, unburdened by legacy systems, created the environment for perpetual contracts to thrive in an internet-native way. The specific mechanisms making perpetual contracts work were first solved at scale in 2016 by BitMEX for trading Bitcoin, and BitMEX achieved remarkable growth with this innovation.

Perpetual contracts subsequently gained tremendous traction. In 2025, the total trading volume of perpetual contracts on centralized exchanges reached $62 trillion. This is many times the approximately $19 trillion spot trading volume and constitutes the majority of the $86 trillion total derivatives trading volume, indicating a market preference for perpetual contracts over options.

For most of this time, perpetual contracts traded on centralized exchanges (CEX). The more recent and interesting story is their migration on-chain to decentralized exchanges (DEX).

There were many early attempts with some success, most notably GMX and Synthetix using a pool-based trading model, and dYdX using a central limit order book and a dedicated blockchain, but they struggled to match centralized platforms in latency, liquidity, and user experience.

Hyperliquid has elevated DEX perpetual contracts to a new level, significantly increasing the market share of on-chain perpetual contracts. DEX perpetual contract volume has reached 14% of CEX perpetual contract volume, up from less than 1% when Hyperliquid first launched in early 2023.

The Rise of Hyperliquid

Hyperliquid is the largest decentralized perpetual contract exchange, accounting for approximately 40% of on-chain perpetual contract volume. It was conceived by Jeff Yan, an alumnus of Harvard's Math 55 course and a former high-frequency trader who had previously run a low-key market-making firm, Chameleon Trading, for several years.

The collapse of FTX was the catalyst for building Hyperliquid. Yan pivoted his trading team to create a decentralized alternative to replace the centralized exchanges that had just failed users, while also recognizing that existing blockchains were too slow for professional on-chain trading.

The team built their own Layer 1 blockchain tailored for trading and launched it globally at the end of February 2023. One change included adding a feature akin to a speed bump to prevent the most aggressive high-frequency trading firms from taking advantage of market makers, sacrificing short-term volume for healthier growth.

To address the cold-start problem faced by all exchanges, the team bootstrapped liquidity by opening their own proprietary trading algorithms to the public, allowing anyone to participate through an on-chain vault called HLP (Hyperliquidity Provider).

Offering this high-performance strategy for free brought the additional benefit of winning over the community, whose members became consistent advocates, further driving Hyperliquid's growth.

Concerned about regulatory uncertainty in the U.S. regarding decentralized finance and perpetual contracts, they also moved to Singapore in the spring of 2024. This is one of many significant losses suffered by the U.S. due to its previous regulatory stance, which is now being corrected.

With a high-density talent core team, a spirit of stakeholder alignment representing the best ideas in cryptocurrency, and incredible execution, Hyperliquid has surpassed competitors to become the largest and most profitable decentralized perpetual exchange, with monthly trading volume exceeding $250 billion and annualized revenue reaching $800 million.

Hyperliquid's trading volume continues to grow, and its share of volume relative to centralized exchanges increases over time.

From Digital Assets to "Holding All Finance"

Hyperliquid's growth accelerated this year as it expanded beyond crypto-native assets to stocks, commodities, indices, and private companies. Jeff Yan describes this vision as "holding all finance" on a single platform.

Hyperliquid has two blockchain-native attributes that have helped it successfully expand its horizon to traditional assets typically traded on traditional exchanges. First, as a decentralized exchange, Hyperliquid is open by default 24/7, including weekends and holidays. In contrast, traditional exchanges like the New York Stock Exchange (NYSE) or the Chicago Mercantile Exchange (CME) are only open five business days a week.

The second attribute is that Hyperliquid is permissionless, meaning any third party can quickly list the assets people most want to trade. The market for listings is not limited to the imagination of Hyperliquid's core team.

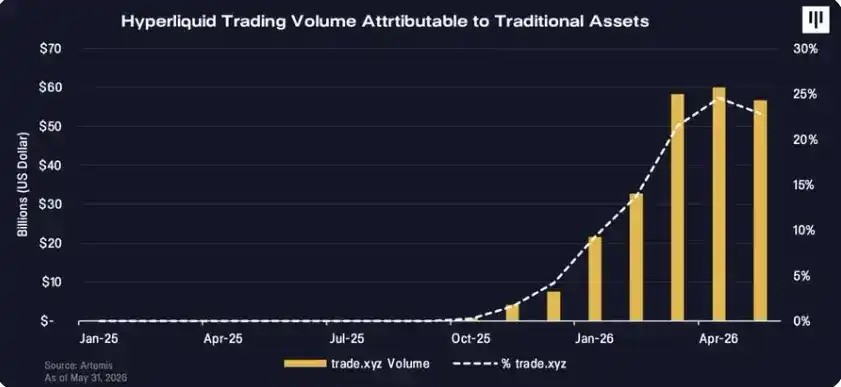

Permissionless listing was unlocked by Hyperliquid Improvement Proposal 3 (HIP-3), a framework allowing any third party to permissionlessly launch new perpetual contract markets, incentivized with a portion of trading fees. An independent group operating under the brand trade.xyz has been the most active deployer.

Consequently, the Hyperliquid platform can adapt quickly, attracting trading volume on whatever asset is hottest at the moment, even when traditional markets are closed, with remarkable results. On-chain perpetual contracts are becoming a parallel, always-on derivatives platform, beginning to meaningfully compete with traditional infrastructure.

The most obvious evidence appears during stressful moments outside traditional trading hours. When gold and silver prices took off in late 2025, Hyperliquid was the only platform where these assets could be traded over the weekend, including the moment China announced changes to silver trading collateral requirements. Silver briefly reached 2% of global derivatives trading volume at its peak.

When the Iran conflict began on a Saturday morning in late February, Hyperliquid was the only platform where people could trade oil that weekend, with daily crude oil volume surging (Editor's note: The original text is missing the number here).

When oil futures opened on Sunday evening, the opening price was exactly the price at which oil perpetual contracts had already been trading on Hyperliquid. Oil trading reached 2% of global oil derivatives trading volume at its peak.

A month later, a fully licensed S&P 500 index perpetual contract surpassed $100 million in trading volume on its first day. Trading volume of traditional assets on Hyperliquid has sometimes reached up to 40%, a figure that was essentially zero at the end of 2025.

Mainstream Attention Begins

Hyperliquid's appeal garnered mainstream attention this year. We are hearing more traditional asset hedge funds referencing Hyperliquid prices and even considering trading on the platform to react more timely to world events.

Hyperliquid is becoming the exchange for price discovery when all other markets are closed. This doesn't just mean weekends but increasingly applies to pre-IPO private companies.

On the day of Cerebras's IPO (the largest IPO year-to-date), the banks underwriting the IPO were monitoring prices on Hyperliquid. A circulating photo showed a banker's screen displaying the Hyperliquid trading interface before the market opened.

Traditional exchanges on Wall Street are also paying attention. On May 27th, at Bernstein's Strategic Decisions conference, Intercontinental Exchange (ICE) founder and CEO Jeffrey Sprecher called Hyperliquid "bigger than Nasdaq" and noted that ICE had met with its founders several times.

Just two weeks ago, reports emerged that ICE and CME were pressuring regulators to restrict Hyperliquid, indicating they view it as a genuine competitive threat. The significance is that one of the world's major exchange operators is now publicly acknowledging Hyperliquid as a serious competitive challenge, not a fringe experiment.

The public equity market has also shown interest. Hyperliquid Strategies Inc. (NASDAQ: PURR) is a Digital Asset Treasury ("DAT") dedicated to Hyperliquid, with Pantera as a cornerstone investor. The company holds HYPE on its balance sheet, chaired by former Barclays CEO Bob Diamond and with David Shamis as CEO.

The duo has taken the case for HYPE directly to mainstream U.S. financial media, including CNBC's Squawk Box and Bloomberg, bringing traditional finance pedigree and credibility to this crypto-native asset, thereby raising its profile.

As of June 1, 2026, PURR's stock price has increased over 200% year-to-date and is one of the few DATs consistently trading at a premium to its net asset value, hinting at strong demand.

The next catalyst to watch is SpaceX's IPO, reportedly targeted for later this month. There is a SpaceX perpetual contract on Hyperliquid, offering traders a way to express pricing expectations for the company before its Nasdaq listing opens to public equity investors.

As of June 1, 2026, SpaceX is currently trading around $200 per share on Hyperliquid, above the level rumored bankers wanted to price the stock.

Every market participant is watching this IPO, and we can reasonably expect Elon Musk, the famously "chronically online" and crypto-supportive SpaceX CEO, might prompt bankers and potential investors to consider SpaceX's trading on Hyperliquid, significantly boosting the platform's profile.

How Big Can This Become?

Hyperliquid is an on-chain protocol with a token-based capital structure. HYPE is the native token, through which Hyperliquid's protocol economics accumulate value, most notably via the platform's programmatic buyback mechanism utilizing 99% of revenue—a capital allocation strategy akin to many stocks with fundamental value.

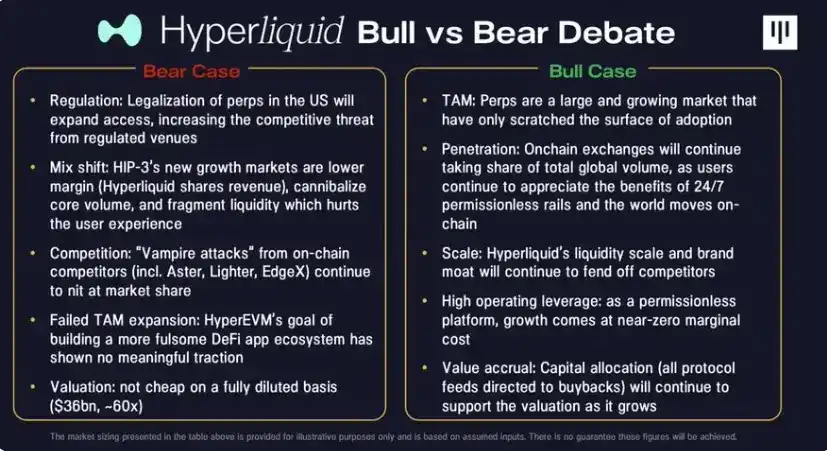

The investment case for Hyperliquid rests on several pillars:

Large and Growing Target Market: Hyperliquid is a disruptive platform targeting an attractive and expanding end market. Perpetual contracts are an innovative product serving a large set of investors better than traditional derivatives, historically monetized with highly attractive trading fees. As Hyperliquid expands from crypto-native markets toward its "holding all finance" goal, its total addressable market grows by multiples.

Strong Execution and Scale Flywheel: The protocol has captured significant market share by scaling faster and more successfully than prior decentralized perpetual exchange iterations. In this market, scale creates a flywheel advantage: higher trading volume drives order book liquidity, which continuously improves user experience and attracts more capital.

Superior Product Experience: Hyperliquid delivers a premium user experience by operating on a custom Layer 1 blockchain built for derivatives trading. User feedback consistently highlights that the platform is far superior to other DEXs and rivals major CEXs in speed and user experience.

Direct and Powerful Token Holder Value Accrual: Crucially, these strong fundamentals translate directly into protocol profitability and token value. Hyperliquid generates $800 million in annualized revenue, with almost all of it directed to its programmatic token buyback mechanism. This creates exceptionally tight alignment between protocol growth and token holder value.

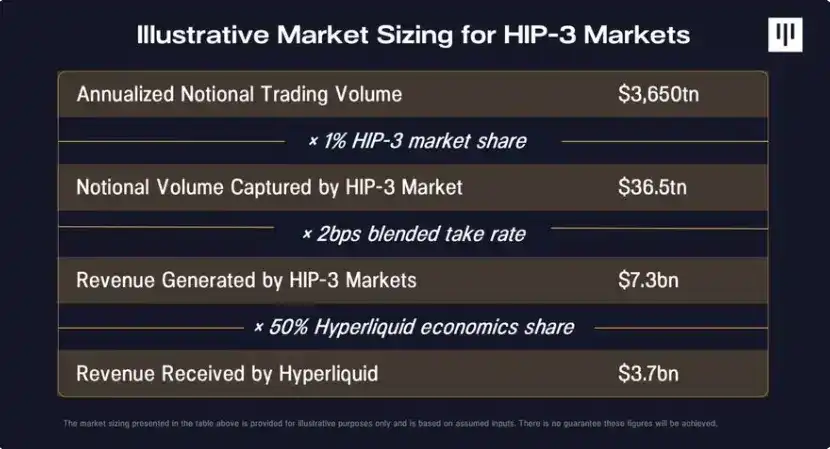

Zooming out, Hyperliquid's total addressable market (TAM) is approximately $10 trillion in daily notional trading volume. Currently, among instruments investors use for simple high-leverage directional exposure, stock trading volume for 0DTE options and leveraged ETFs is about $200 billion daily.

Commodity derivatives daily volume is $2 trillion, and Hyperliquid has proven it can make inroads, especially on holidays and weekends. FX derivatives daily volume is around $8 trillion and remains almost entirely untapped on-chain, presenting a massive blue ocean opportunity.

Sustainably capturing even a very low single-digit percentage of this combined volume implies potential revenue 5x today's level, with a similarly expansionary potential for valuation.

Nevertheless, it's important to recognize that Hyperliquid faces real risks. The biggest risk Hyperliquid faces is regulation. Perpetual contracts are currently not freely tradable in the U.S., although a trend toward legalization and listing has emerged.

Hyperliquid is a decentralized exchange, meaning it has no KYC requirements. While it has geofenced U.S. users, it's not impossible to think methods to bypass exist.

If perpetual contracts are legalized in the U.S., Hyperliquid will face a more competitive landscape and could lose share of U.S. user volume migrating to regulated platforms. A mitigating factor is that Hyperliquid might also launch a regulated U.S. exchange version, as other platforms have done.

The Door Opens for Regulatory Developments

The single biggest constraint on the growth of U.S. perpetual contracts has been regulation, the very uncertainty that pushed Hyperliquid's team offshore to Singapore. Americans have not had access to true perpetual futures, with both centralized and decentralized platforms geofencing U.S. users.

This began to change last week. The CFTC approved a Bitcoin-based perpetual futures contract filing by Kalshi, a U.S.-registered exchange, and its staff separately cleared the way for Coinbase to offer certain crypto perpetual contracts through a foreign affiliate, treating them as foreign futures.

The headline is that the CFTC has opened a path for regulated crypto perpetual contracts under the existing futures framework, rather than requiring entirely new rules.

Some policy advocates argue that the absence of perpetual contracts in the U.S. was more a commercial accident of what existing firms chose to list than a thoughtful regulatory choice, and there was never a fundamental reason why the CFTC couldn't approve them. The CFTC now just needs to act to clarify this if and when exchanges apply to list more perpetual contracts.

The harder question is what it would take to bring decentralized perpetual contracts to U.S. users, and the path here is less clear. A centralized participant can register as a U.S. exchange today, and we've already seen others like Coinbase and Kalshi looking to list true perpetual contracts.

For a permissionless on-chain protocol, the Commission would need to expand exemptions to include waivers from the requirement that derivatives must trade on a registered exchange, and from rules about who can access certain contracts.

Both the SEC and CFTC hold pro-innovation stances and have previously made statements supporting the view that "nothing in the core stack of an on-chain protocol inherently requires registration." However, reconciling permissionlessness and lack of KYC with legitimate concerns about sanctions and market integrity will take some work to resolve.

Perpetual contracts began on the fringes of cryptocurrency, where market structure evolved fastest. Perpetual contracts are now moving toward the center of global finance. Recent CFTC actions haven't resolved all regulatory questions, especially for permissionless on-chain platforms, but they do mark a significant shift.

The U.S. is beginning to embrace this product, not reject it. Hyperliquid sits at the center of this shift. It combines the best attributes of DeFi (open access, 24/7 markets, transparent settlement, and high alignment of interests among parties) with a product that looks increasingly more suited to modern trading than its competing instruments.

The question is no longer whether perpetual contracts matter beyond crypto—the market has answered that.

The question is whether the infrastructure the blockchain industry built first can become the place where an increasing amount of risk pricing, trading, and price discovery happens for the rest of finance.