Author: @100y_eth (Four Pillars)

Compiled by: AididiaoJP, Foresight News

MicroStrategy (MSTR) recently sold 32 bitcoins (worth only $2.5 million), which triggered a market cap evaporation of over $100 billion in Bitcoin. STRC (its perpetual preferred stock) fell from a reference price of $100 to $94, and MSTR's stock price also dropped from $150 to $123.

MSTR, BTC, and STRC are deeply intertwined. In a bullish market, this structure is a powerful capital engine, allowing Strategy (MicroStrategy) to aggressively accumulate Bitcoin; but once the market deteriorates, as it has recently, the three form a vicious cycle of mutual negative feedback.

This reminds people of the LUNA-UST incident from years past. So, is the MSTR-STRC structure truly sustainable?

Key Takeaways

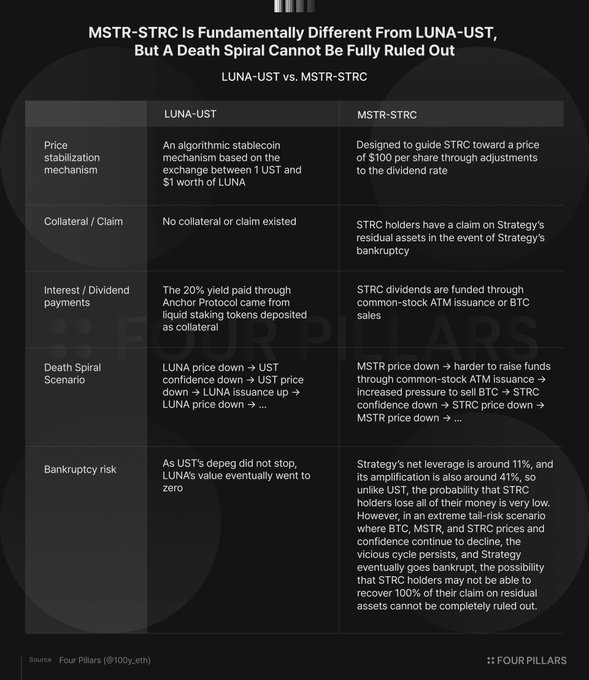

UST and STRC appear similar on the surface: their prices are anchored to a specific reference value, holders can obtain high yields, and both carry death spiral risks. However, they are fundamentally different in their price stabilization mechanisms, legal recourse rights, interest/dividend payment methods, and internal operational structures.

For Strategy to maintain sustainability, it must continuously raise funds. This relies on both market confidence and its own creditworthiness. In the worst-case scenario, even if it cannot continue financing, it will not experience a direct "death spiral" like LUNA-UST.

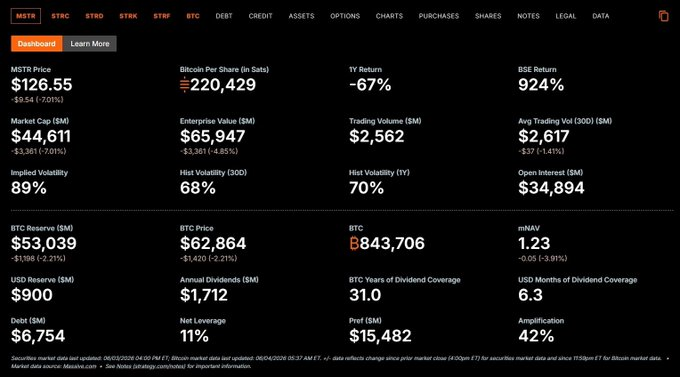

Strategy's current net leverage ratio is about 11%, with an amplification factor of approximately 42%. Even if MSTR and STRC enter a negative feedback loop, as long as the Bitcoin price remains above about $26,000, preferred shareholders still have a high probability of preserving their principal; and as long as Bitcoin does not fall below about $8,000, the probability of bankruptcy due to debt is very low.

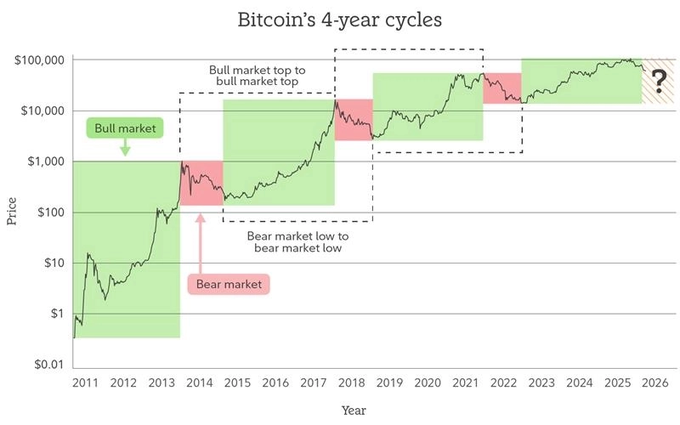

The next six months will be a critical period. According to Bitcoin's four-year cycle theory, a bottom could be seen in the second half of this year, and Strategy's US dollar reserves are only sufficient to last about six months. The core question is: can Strategy restart its capital engine through healthy deleveraging within these six months?

LUNA-UST Quick Recap

The LUNA-UST collapse was four years ago. Let's quickly review its operating mechanism.

Price Stabilization Mechanism

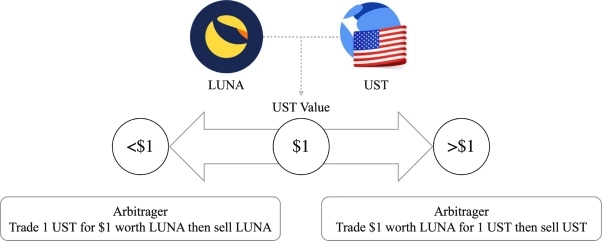

UST was an algorithmic stablecoin with no collateral, maintaining its $1 peg through an algorithm. The core rule was: 1 UST could always be exchanged for $1 worth of LUNA.

- When UST < $1: Users could burn UST worth less than $1 to receive $1 worth of LUNA. The arbitrage opportunity pushed the UST price back up while reducing UST supply.

- When UST > $1: Users could provide $1 worth of LUNA to receive more valuable UST. Arbitrage pushed the UST price down while increasing UST supply.

Vicious Cycle Scenario

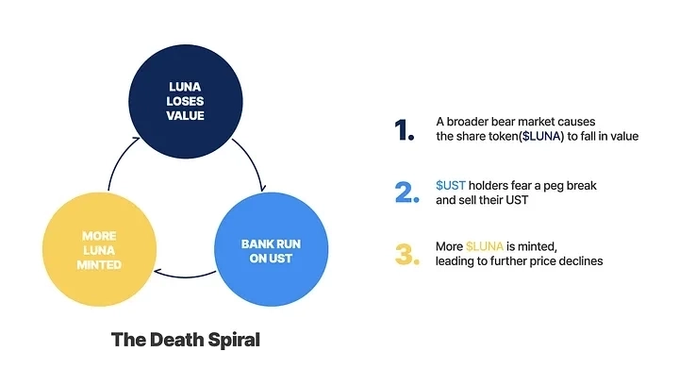

The more UST issued, the less LUNA supply, which should have been a positive driver for LUNA's price. Terraform Labs indeed amplified this effect by aggressively expanding UST use cases.

However, once confidence collapsed, the same mechanism reversed into a death spiral:

LUNA price drops → UST confidence collapses → UST price drops → LUNA massively increases supply → LUNA price drops further...

The LUNA-UST Collapse

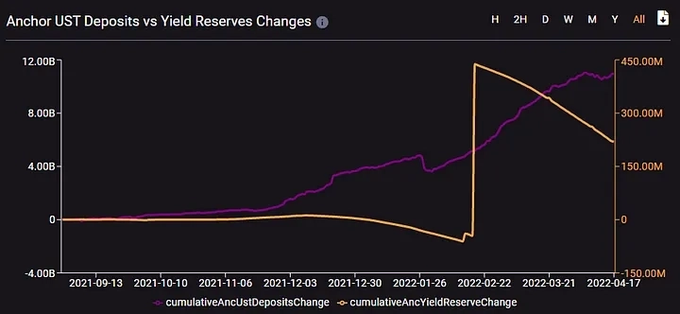

The direct trigger for the collapse was a loss of confidence. At the time, Terraform Labs was migrating UST liquidity on Curve from the 3pool to the 4pool, thinning liquidity in the 3pool. An attacker sold $85 million worth of UST, breaking the peg and triggering panic.

A large amount of UST was withdrawn from Anchor Protocol (which offered about 20% APY for deposits), instantly overwhelming the market with selling pressure. Before the crash, 71% of UST was deposited in Anchor. When the unsustainability of the 20% yield was exposed, even a $450 million injection by the Luna Foundation Guard was powerless to stop it.

Ultimately, LUNA supply exploded from about 350 million tokens to 65 trillion tokens (a 17,000-fold increase), with its price approaching zero.

Detailed Analysis of the MSTR-STRC Structure

Strategy's core goal is to increase BPS (Bitcoin per Share). To achieve this, it raises funds through various financial engineering tools like convertible bonds, perpetual preferred stock, and ordinary share ATM offerings, then uses the raised capital to accumulate more Bitcoin.

Financing Methods

- Ordinary Share ATM Offerings: Issuing small amounts of MSTR Class A ordinary shares for sale on the market. This causes ADSO (assuming fully diluted shares outstanding) dilution, but when mNAV > 1.22, it can actually increase BPS.

- Convertible Bonds: Low-interest borrowing with conversion options, but carries principal repayment pressure.

- Perpetual Preferred Stock: Dividends and liquidation priority are higher than ordinary shares but lower than creditors. No principal repayment pressure, but dividend burden is close to 10%. Current series include STRF, STRC, STRE, STRK, STRD, etc. Only STRK is convertible preferred stock; the others are non-convertible. Non-convertible preferred stock does not dilute ADSO and is Strategy's preferred financing method.

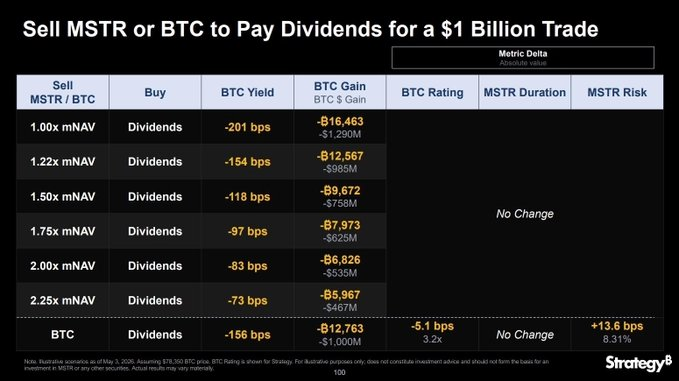

Strategy currently needs to pay about $1.712 billion in annual interest and dividends, primarily funded from its US dollar reserves, which are mainly replenished through ordinary share ATM offerings. Recently, it also paid dividends by selling 32 BTC, drawing market attention.

STRC Price Stabilization Mechanism

STRC is designed with a $100 reference price.

- When STRC > $100: Strategy can lower the dividend rate to depress the price, or issue more STRC to increase supply. It also holds the right to redeem at $101/share, effectively capping STRC's upside.

- When STRC < $100: Strategy can increase the dividend rate to push the price up. Simultaneously, STRC has a $100/share liquidation preference, providing price support.

Currently, STRC's annualized dividend rate is 11.50% (based on the $100 reference price).

Vicious Cycle Scenario

MSTR and STRC influence each other, forming a self-reinforcing feedback loop. A deteriorating market can lead to a vicious cycle:

MSTR price drops → mNAV decreases → Difficulty of ordinary share ATM financing increases → Pressure to sell BTC rises → STRC confidence drops → STRC price drops → MSTR price drops further...

However, the key difference is: Strategy is not obligated to pay STRC dividends in cash monthly. Cash payments require a board declaration and sufficient funds; otherwise, dividends can accumulate. Additionally, Strategy can theoretically lower the dividend rate to SOFR (Secured Overnight Financing Rate). In extreme cases, it can gradually reduce the dividend rate and defer payments until conditions improve.

LUNA-UST vs MSTR-STRC: Fundamental Differences

UST and STRC share three apparent similarities: price anchored to a specific level, holders can obtain high yields, and both carry death spiral risks. However, their internal operating mechanisms are entirely different.

Price Stabilization Mechanism

UST stabilized by adjusting LUNA supply; STRC stabilizes by adjusting its own dividend rate. UST's peg mechanism directly affected LUNA's price and supply, while STRC's mechanism does not directly affect MSTR's price and supply.

However, since STRC dividends are primarily funded by MSTR ATM offerings, if MSTR's value falls causing mNAV to drop below 1.22, Strategy's ability to maintain dividends would be questioned.

Collateral / Recourse Rights

UST was completely uncollateralized, and its price could go to zero; STRC, as preferred stock, is also uncollateralized, but in case of company bankruptcy, STRC holders have priority recourse rights to remaining assets (liquidation preference of $100/share).

Interest / Dividend Source

UST itself did not generate interest; the 20% yield came from Anchor Protocol's lending interest and staking rewards (natural market demand).

STRC dividends are primarily funded by ordinary share ATM offerings; in extreme cases, selling BTC is also possible. From a BPS perspective, ATM offerings are beneficial when mNAV > 1.22, while selling BTC is preferable when below 1.22. Overall, however, the "naturalness" of STRC's dividend source is weaker than Anchor's lending + staking rewards.

Death Spiral Differences

The LUNA-UST death spiral was direct and automatic: UST drop → LUNA supply increase → LUNA further drop.

The MSTR-STRC death spiral is more complex and has two major braking mechanisms: First, the direct linkage is weaker; MSTR does not automatically increase supply like a protocol to pay STRC dividends. Second, there are legal recourse rights; even in bankruptcy, STRC holders have recourse to remaining assets, providing downside price support.

The common catalyst for both remains "confidence." As long as investors maintain confidence in MSTR (or LUNA back then), the structure can operate; once confidence collapses, real problems emerge. MSTR selling 32 BTC is not a major event rationally, but emotionally, it could become the trigger for a loss of confidence.

Is the MSTR-STRC Structure Sustainable?

Sustained Fundraising Ability is Core

Strategy's current US dollar reserves are $900 million, with annual interest + dividend obligations of $1.712 billion. Without additional fundraising, reserves alone can sustain about 6.3 months.

If reserves are depleted, it could continue financing by issuing more shares / preferred stock, or sell BTC (theoretically sustainable for 31 years). However, the recent sale of just 32 BTC triggered a severe market reaction; the side effects of selling BTC are far greater than imagined.

Financing conditions are clear:

- MSTR ATM offerings require mNAV > 1.22; otherwise, they reduce BPS.

- STRC issuance requires the price to be maintained near $99-100; otherwise, financing costs become too high.

Both are highly dependent on market confidence: investors must believe in BTC's long-term appreciation and that Strategy can create value beyond simple holding. In the current market environment, raising funds through shares / preferred stock is difficult in the short term. Strategy can only rely on existing dollar reserves and wait for the market and confidence to recover.

What Happens in Bankruptcy?

Strategy's net leverage ratio is only 11% ((Debt - USD Reserves) / Bitcoin Reserves). The amplification factor including preferred stock is about 42%.

As long as the Bitcoin price does not fall below approximately $26,300 (the price corresponding to the total value of debt + preferred stock), preferred shareholders can preserve their principal through recourse to remaining assets. This is the biggest difference from LUNA-UST.

Convertible Bond Maturity Pressure

Strategy has no principal repayment obligation for perpetual preferred stock, but convertible bonds require principal repayment at maturity (current total debt $6.714 billion). Maturities begin in 2028. With current USD reserves of only $900 million, if unable to raise funds, it may need to sell BTC to repay debt. However, with a low net leverage ratio, the probability of bankruptcy due to debt is extremely low.

The Next Six Months are the Lifeline

If Bitcoin's four-year cycle theory still holds, a bottom could be seen in the second half of this year, and Strategy's dollar reserves happen to be sufficient for only about six months.

Within these six months, whether Strategy can restart its capital engine through healthy deleveraging will determine its future fate.

Although the title and images are somewhat sensational, the MSTR-STRC and LUNA-UST mechanisms are fundamentally different. The probability of a similar catastrophic collapse is extremely low.

The real question is: Can Strategy survive the challenging next six months, restart its capital engine through healthy deleveraging, or will it merely become an interesting experiment in Bitcoin's history?