A "small note" from a South Korean securities firm sent SK Hynix plunging 12%, pressuring the entire memory sector. The US military launched a new round of strikes against Iran, suddenly intensifying tensions in the Middle East and causing turbulence in global markets.

On Monday, before the US market opened, memory chip stocks fell across the board: Micron Technology down about 6%, Seagate Technology down about 4%, Western Digital down about 6%, SanDisk down about 7%. SK Hynix's stock price plunged 15.4%, marking its largest-ever single-day drop, and Samsung fell nearly 11%. The two heavyweight stocks combined to trigger the seventh circuit breaker of the year for South Korea's Kospi index. The immediate trigger was an earnings forecast that was 8% below market expectations, combined with a wave of profit-taking as the "good news" of its $26.5 billion ADR listing was exhausted. Deeper reasons include insufficient pricing elasticity for HBM, and a supply-demand scissors gap between capacity expansion and slowing demand, creating real cracks in the market's valuation logic for memory chips.

Crude oil prices rose sharply, and US Treasury yields climbed. According to CCTV News, US Central Command announced that at 5:00 PM Eastern Time on July 12, the US military began a new round of strikes against Iran, aiming "to continue degrading its ability to attack vessels freely transiting the Strait of Hormuz." In the early hours of July 13 local time, explosions were reported in multiple locations in Iran, including Bandar Abbas and the Sirik region. Meanwhile, precious metals like gold weakened broadly, and the US dollar strengthened.

This round of tensions coincides with a critical juncture for markets—the US earnings season is about to begin, with Goldman Sachs and JPMorgan Chase set to report results on Tuesday. Inflation data is also scheduled for release this week, clearly heightening market concerns that rising energy prices could further push up inflation.

- Pre-market US memory chip stocks fell across the board: Micron Technology down about 6%, Seagate Technology down about 4%, Western Digital down about 6%, SanDisk down about 7%.

- Europe's Stoxx 50 index opened down 0.5%, Germany's DAX index down 0.5%, the UK's FTSE 100 up 0.1%, France's CAC 40 index down 0.3%.

- Japan's Nikkei 225 index closed down 1.9% at 67,242.73 points. Japan's Topix index closed down 0.7% at 4,007.49 points. South Korea's KOSPI index closed down 8.9% at 6,806.93 points. SK Hynix's stock price plunged 15.4%, marking its largest-ever single-day drop.

- Nasdaq 100 index futures fell 1.3%, and European stock futures also indicated an opening drop of about 1%.

- US Treasuries were sold off across the board. The yield on the policy-sensitive 2-year Treasury note rose 2 basis points to 4.23%, its highest level since February 2025. Japanese and Australian government bond yields also fell.

- The US dollar strengthened across the board against G10 currencies. The US dollar index rose 0.2%.

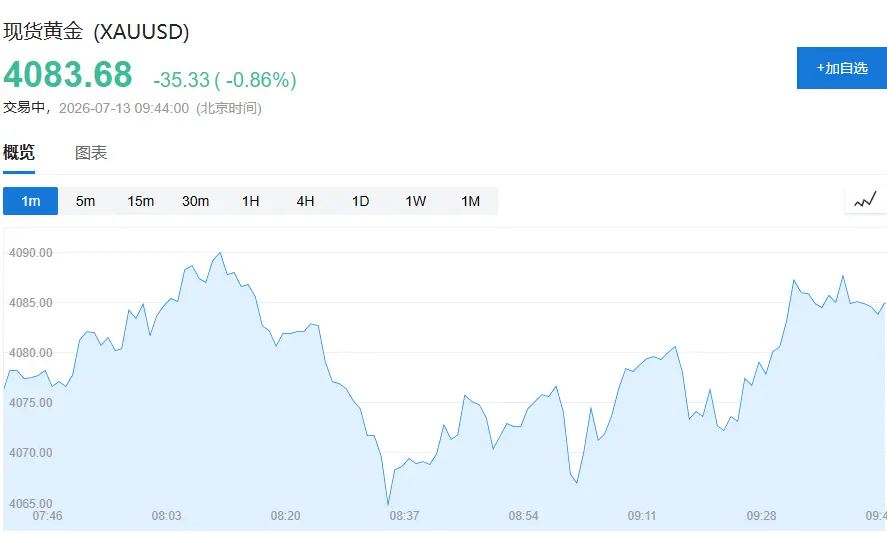

- Gold fell 1.3% to about $4,065 per ounce; silver fell nearly 3% to about $58.20 per ounce.

- The cryptocurrency market also weakened, with Bitcoin down over 2% to around $62,700, dragging down the broader crypto market.

Stock Markets Under Pressure Across the Board, South Korea Leads Declines

South Korea's KOSPI index closed down 8.9% at 6,806.93 points. SK Hynix's stock price plunged 15.4%, marking its largest-ever single-day drop. Japan's Nikkei 225 index closed down 1.9% at 67,242.73 points. Japan's Topix index closed down 0.7% at 4,007.49 points.

On the news front, South Korean President Lee Jae-myung stated that a "Future Response Fund" will be established to channel surplus tax revenue into productive future investment projects. Government support will be directed to three mega-projects: chips, AI data centers, and physical AI.

Part of SK Hynix's sharp pullback stemmed from profit-taking pressure following its American Depositary Receipts (ADRs) rising 13% on their New York debut last Friday. Korea Investment & Securities predicted that SK Hynix's second-quarter operating profit might be 8% lower than market expectations, citing the company's higher revenue proportion from High Bandwidth Memory (HBM) limiting its average selling price increase potential. The institution believes the upward momentum in the New York market has been fully digested, and the stock may face significant profit-taking and arbitrage unwinding, potentially closing with a long upper shadow.

Japan's Nikkei 225 opened 0.1% lower, with the loss later widening to 1%. Shoji Hirakawa, chief global strategist at Tokai Tokyo Intelligence Lab, said, "Further escalation in attacks between the US and Iran could act as a negative catalyst for the market. During periods of rising geopolitical risk, investors tend to favor sectors with strong profitability, which means semiconductor stocks may remain relatively resilient."

Crude Oil Surges, Market Worried About Inflation and Rate Hike Prospects

Uncertainty surrounding the Strait of Hormuz directly pushed oil prices higher. Brent crude rose over 3% to $78.50 per barrel; WTI crude futures gained up to 4.2% to $74.40 per barrel, one of the largest single-day gains recently.

The surge in oil prices has reignited inflation concerns. Oil had already posted its biggest weekly gain since mid-May the previous week. Traders subsequently made large bets on further monetary tightening by the Fed—interest rate swaps are now pricing in nearly 40 basis points of cumulative Fed rate hikes by December, a significant increase from around 15 basis points in early June.

The US Treasury market came under simultaneous pressure. The yield on the rate-sensitive 2-year Treasury note rose 3 basis points to 4.23%, a new high since February 2025; the 10-year yield also climbed 3 basis points to 4.59%. Australian and Japanese government bond yields also moved higher. Bloomberg strategist Mark Cranfield noted that if oil prices remain strong, US Treasuries will face further downward pressure, and the oil-bond-dollar linkage effect will continue to play out in the short term.

Gold Weakens, Dollar Strengthens

In contrast to crude oil, precious metals generally weakened. Spot gold fell 1.1% to $4,073 per ounce; silver dropped 1.8% to $58.82 per ounce; platinum and palladium also weakened.

Notably, gold has fallen more than a fifth since the Iran war erupted at the end of February, ending a three-year bull run. A wave of large-scale profit-taking once pushed the gold price below $4,000 for the first time since last November. The core logic behind gold's recent pressure is that rising oil prices boost inflation expectations, thereby strengthening rate hike expectations.

The US dollar, meanwhile, strengthened broadly. The Bloomberg Dollar Spot Index rose 0.2%, the euro fell 0.2% to $1.1397, and the yen fell 0.2% to 162.00 per dollar. Bitcoin, after initially falling, recovered some losses, trading around $64,175.

Focus This Week: Inflation Data, Earnings Season, and Central Bank Moves

Markets face multiple tests this week. US inflation data is due for release, and whether persistently rising energy prices can further push up CPI will be a key focal point. Fed Chairman Kevin Warsh will also make his first appearance before Congress for a hearing, marking his first public remarks since taking office. The market will closely watch his latest stance on the interest rate outlook.

Regarding the earnings season, Goldman Sachs and JPMorgan Chase will be the first to report results on Tuesday, marking the first major test of whether corporate profits can support the market rally driven by AI optimism. Asian markets will focus on China's second-quarter GDP growth data and the Bank of Korea's interest rate decision to assess the extent of economic drag from weak domestic demand.