PayPal is starting a bank.

On December 15, the global payments giant with 430 million active users formally applied to the Federal Deposit Insurance Corporation (FDIC) and the Utah Department of Financial Institutions to establish an industrial bank (ILC) named "PayPal Bank".

However, just three months earlier, on September 24, PayPal had announced a major deal, selling off a massive $7 billion portfolio of "Buy Now, Pay Later" loan assets to the investment firm Blue Owl.

During the earnings call at that time, CFO Jamie Miller emphatically assured Wall Street that PayPal's strategy was to "maintain a light balance sheet," to free up capital and improve efficiency.

These two actions seem contradictory. On one hand, they pursue being "light," yet on the other, they apply for a bank charter. It's important to remember that running a bank is one of the "heaviest" businesses in the world—requiring massive capital reserves, submitting to the most stringent regulations, and bearing the risks of deposits and loans yourself.

Behind this convoluted decision must lie a compromise driven by some urgent necessity. This isn't a routine business expansion; it's more like a desperate beachhead assault on a regulatory red line.

PayPal's official reason for starting a bank is "to provide lower-cost loan funding to small businesses." But this justification doesn't hold up to scrutiny.

Data shows that since 2013, PayPal has cumulatively provided over $30 billion in loans to 420,000 small businesses worldwide. This means that for the past 12 years without a bank charter, PayPal has still managed to run a thriving lending business. So why choose this specific moment to apply for a bank charter?

To answer this, we first need to understand: Who actually issued those $30 billion in loans?

In Lending, PayPal is Just a "Sublessor"

PayPal's official press releases boast impressive lending data, but they often deliberately obscure a core fact. For every single one of those $30 billion in loans, the actual lender was not PayPal, but a bank based in Salt Lake City, Utah, called WebBank.

Most people have probably never heard of WebBank. This bank is extremely secretive; it doesn't operate consumer-facing branches, doesn't advertise, and even its website is minimal. But in the hidden corners of American fintech, it's an unavoidable behemoth.

The lending behind PayPal's Working Capital and Business Loan products, the installment plans from star company Affirm, and the personal loan platform Upgrade—all of these are backed by WebBank.

This involves a business model called "Banking as a Service" (BaaS): PayPal handles customer acquisition, risk control, and user experience, while WebBank is responsible for just one thing—providing the charter.

Using a more通俗的比喻, PayPal in this business is merely a "sublessor"; the actual property deed is held by WebBank.

For a tech company like PayPal, this was once a perfect solution. Applying for a bank charter is too difficult, slow, and expensive, and obtaining lending licenses in all 50 U.S. states is an administrative nightmare of epic proportions. Renting WebBank's charter was like a VIP fast pass.

But the biggest risk of "renting" to do business is that the landlord can stop renting at any time, or even sell or demolish the property.

In April 2024, a black swan event sent chills down the spines of all U.S. fintech companies. A BaaS intermediary company named Synapse suddenly filed for bankruptcy, directly leading to over 100,000 users having $265 million frozen, with even $96 million simply disappearing. Some people lost their life savings.

This disaster made everyone realize that the "sublessor" model has significant vulnerabilities. If something goes wrong in the middle of the chain, the user trust you've painstakingly built can collapse overnight. Regulatory agencies began严厉审查 the BaaS model, with several banks fined and restricted for BaaS compliance issues.

For PayPal, even though they partner with WebBank and not Synapse, the risk logic is the same. If WebBank has problems, PayPal's lending business is paralyzed; if WebBank adjusts合作条款, PayPal has no bargaining power; if regulators force WebBank to tighten cooperation, PayPal can only passively accept it. This is the "sublessor's" dilemma: you work hard to run the business, but your lifeline is in someone else's hands.

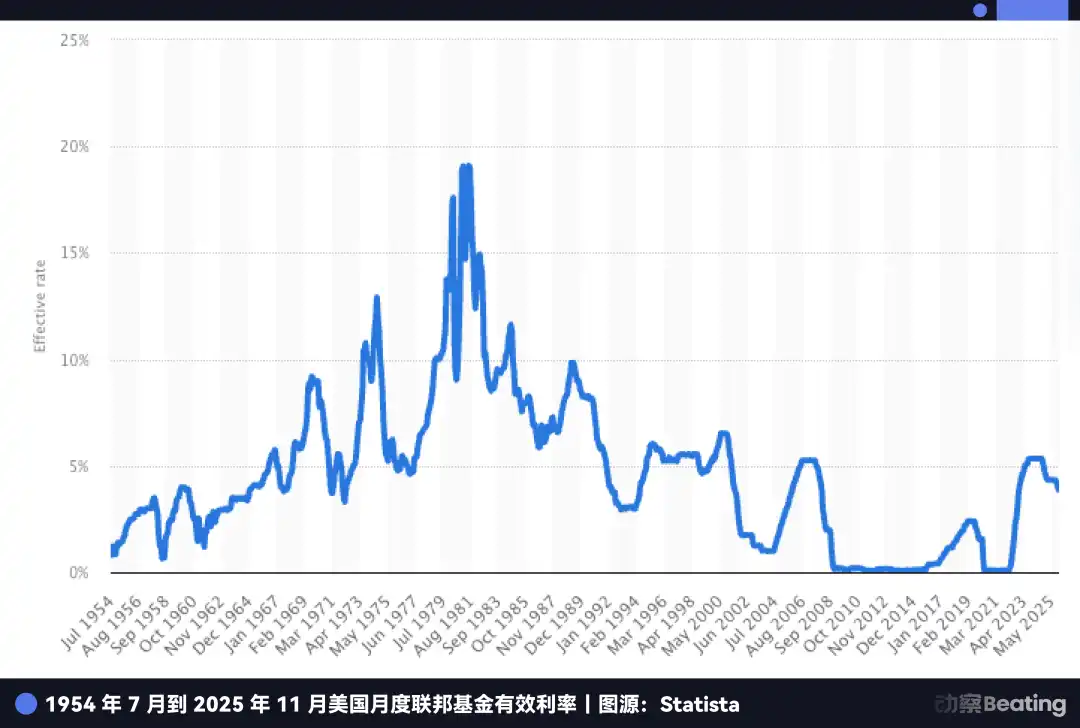

Beyond this, what made management下定决心 to go it alone was another, more赤裸的诱惑: the暴利 of the high-interest era.

During the decade of zero interest rates, being a bank wasn't a particularly sexy business because the net interest margin was too thin. But today, it's completely different.

Even though the Fed has started cutting rates, the U.S. benchmark interest rate remains at a historically high level around 4.5%. This means deposits themselves are a gold mine.

Look at PayPal's current awkward situation: It has a massive pool of funds from its 430 million active users. This money sits in users' PayPal accounts, and PayPal then has to deposit these funds with partner banks.

Those partner banks take this low-cost money and buy U.S. Treasuries yielding 5% or issue higher-interest loans, making enormous profits, while PayPal only gets scraps from the table.

If PayPal gets its own bank charter, it can directly turn the idle funds of those 430 million users into its own low-cost deposits. Then, it can buy Treasuries with one hand and issue loans with the other—keeping all the interest margin profits for itself. In the current high-interest window, this represents a difference of billions of dollars in profit.

But if the goal was just to break free from WebBank, PayPal should have acted long ago. Why wait until 2025?

This brings us to another, more urgent and potentially fatal anxiety deep within PayPal: stablecoins.

With Stablecoins, PayPal is Still a "Sublessor"

If being a "sublessor" in the lending business only meant PayPal made less money and worried more, in the stablecoin battlefield, this dependency is evolving into a genuine survival crisis.

In 2025, PayPal's stablecoin, PYUSD, experienced explosive growth, its market cap tripling in three months to soar to $3.8 billion. Even YouTube announced the integration of PYUSD payments in December.

But behind these lively battle reports is a fact PayPal similarly won't emphasize in its press releases: PYUSD is not issued by PayPal itself, but through a partnership with the New York-based company Paxos.

This is another familiar "white-label" story. PayPal is just the brand licensor—like Nike authorizing a factory to produce shoes instead of running its own factory.

In the past, this seemed more like a business division of labor: PayPal held the product and traffic, Paxos handled compliance and issuance. Everyone ate from their own plate.

But on December 12, 2025, this division began to change flavor. The Office of the Comptroller of the Currency (OCC) gave "conditional approval" for national trust bank charters to several institutions, including Paxos.

This isn't a traditional "commercial bank" that can take deposits and get FDIC insurance, but it signifies that Paxos is moving from being a contract manufacturer to a recognized issuer that can step into the spotlight.

Place this within the framework of the proposed《GENIUS Act》, and you understand why PayPal is急. The bill allows regulated banking systems to issue payment stablecoins through subsidiaries. The power to issue and the profit chain will increasingly concentrate in the hands of those "with a charter."

Before, PayPal could treat stablecoins as an outsourced module. Now, if the outsourcer gains a stronger regulatory身份, it's no longer just a supplier; it can become a replaceable partner, even a potential competitor.

PayPal's尴尬 lies in the fact that it controls neither the issuance infrastructure nor the regulatory身份.

The advancement of USDC and the OCC's move on trust charters are both reminders: the stablecoin battle won't ultimately be about who issues first, but about who can hold the reins of issuance, custody, settlement, and compliance in their own hands.

Therefore, PayPal's move is less about wanting to be a bank and more about acquiring an entry ticket. Otherwise, it risks being permanently left standing outside the arena.

Even more critically, stablecoins pose an existential threat to PayPal's core business.

PayPal's most profitable business is e-commerce payments, relying on charging a 2.29~3.49% transaction fee. But the logic of stablecoins is completely different; they charge almost no transaction fees, making money from the interest earned on the Treasury holdings backing the user's deposited funds.

When Amazon starts accepting USDC, when Shopify enables stablecoin payments, merchants will face a simple calculation: if they can use near-zero-cost stablecoins, why pay PayPal a 2.5% toll?

Currently, e-commerce payments account for over half of PayPal's business revenue. Over the past two years, it has watched its market share slide from 54.8% to 40%. If it doesn't seize the initiative on stablecoins, PayPal's moat will be completely filled in.

PayPal's current situation is reminiscent of Apple when it launched its Apple Pay Later business. In 2024, Apple, lacking a bank charter, found itself constrained by Goldman Sachs at every turn and ultimately shut down the service, retreating to its core hardware domain. Apple could retreat because finance was just a nice-to-have; hardware is its core competency.

But PayPal has nowhere to retreat.

It has no phone, no operating system, no hardware ecosystem. Finance is its everything, its only granary. Apple's retreat was a strategic contraction; if PayPal dares to retreat, it faces death.

Therefore, PayPal must advance. It must obtain that bank charter and bring the issuance rights, control, and profit rights of stablecoins back under its own roof.

But starting a bank in the U.S. is incredibly difficult, especially for a tech company carrying $7 billion in loan assets. The regulatory审批门槛 is dauntingly high.

Thus, to obtain this ticket to the future, PayPal orchestrated a masterful piece of financial engineering.

PayPal's Cicada Shedding Its Shell

Now, let's return to the contradiction mentioned at the beginning of the article.

On September 24, PayPal announced the sale of $7 billion in "Buy Now, Pay Later" loans to Blue Owl, with the CFO loudly proclaiming the goal to "become lighter." At the time, most Wall Street analysts assumed this was just window dressing for the financial statements, to make the cash flow look prettier.

But if you view this event alongside the bank charter application three months later, you see it's not a contradiction but a carefully designed one-two punch.

If it hadn't sold those $7 billion in receivables, PayPal's chances of successfully obtaining a bank charter would have been almost zero.

Why? Because in the U.S., applying for a bank charter requires passing an extremely rigorous "physical exam." The regulator (FDIC) holds a ruler called the "capital adequacy ratio."

The logic is simple: the more high-risk assets (like loans) you have on your balance sheet, the more capital reserves you must hold to抵御风险.

Imagine if PayPal knocked on the FDIC's door carrying this $7 billion loan burden. The regulator would immediately see the heavy包袱: "You're carrying all these risky assets; what if they go bad? Do you have enough money to cover the losses?" This wouldn't just mean PayPal needing to post astronomical sums in保证金; it could directly lead to a rejected application.

Therefore, PayPal had to undergo a comprehensive瘦身 before the exam.

This sale to Blue Owl is known in financial jargon as a forward flow agreement. The design is very shrewd. PayPal offloaded the future receivables from loans issued over the next two years (the "printed money") and the default risk entirely onto Blue Owl. But it very cleverly retained the underwriting rights and customer relationships—it kept the "money printing press" for itself.

From the user's perspective, they are still borrowing from PayPal, still repaying through PayPal's App—the experience is unchanged. But on the FDIC's exam report, PayPal's balance sheet instantly appears clean and lean.

Through this move of the cicada shedding its shell, PayPal completed an identity transformation. It went from a lender burdened with heavy default risk to a mere passerby earning risk-free service fees.

This kind of deliberate asset shuffle to pass regulatory审批 isn't unheard of on Wall Street, but doing it so decisively and on such a scale is rare. It precisely proves the determination of PayPal's management: even if it means giving up the fat meat (loan interest) for others to eat, it must secure that longer-term meal ticket.

Moreover, the window for this gamble is closing fast. The reason PayPal is so urgent is that the "backdoor" it has its eye on is being closed, even welded shut, by regulators.

The Soon-to-Close Backdoor

The charter PayPal is applying for is called an "Industrial Loan Company" (ILC). If you're not deeply involved in finance, you've probably never heard of it. But it is the most bizarre and coveted entity in the U.S. financial regulatory system.

Looking at the list of companies with ILC charters creates a strong sense of incongruity: BMW, Toyota, Harley-Davidson, Target...

You might ask: Why are these car sellers and department stores opening banks?

This is the magic of the ILC. It is the only "regulatory loophole" in the U.S. legal system that allows non-financial giants to legally open a bank.

This loophole originated from the Competitive Equality Banking Act (CEBA) passed in 1987. Although the law is named "Equality," it left an extremely unequal privilege: it exempted the parent companies of ILCs from the obligation to register as "bank holding companies."

If you apply for a regular bank charter, the parent company must submit to the Fed's head-to-toe穿透式监管. But if you hold an ILC charter, the parent company (like PayPal) is not subject to Federal Reserve jurisdiction, needing only to answer to the FDIC and state-level regulation in Utah.

This means you enjoy the national-level privileges of a bank—taking deposits, accessing the federal payment system—while perfectly avoiding Fed interference in your commercial empire.

This is所谓的监管套利. Even more enticing is that it allows "mixed operation." This is how BMW and Harley-Davidson play it: vertical integration within their industry chain.

BMW Bank doesn't need physical counters because its business is perfectly embedded in the car-buying process. When you decide to buy a BMW, the sales system automatically connects to BMW Bank's loan services.

For BMW, it makes profit both from your car purchase and from the interest on the car loan. Harley-Davidson is even more so; its bank can even provide loans to motorcycle enthusiasts rejected by traditional banks, because only Harley itself knows that these die-hard fans actually have low default rates.

This is the ultimate form PayPal dreams of: payments on the left hand, banking on the right hand, with stablecoins in the middle—not letting any outsider插手.

Reading this, you must wonder: If this loophole is so good, why didn't Walmart or Amazon apply for this charter and open their own banks?

Because the traditional banking world despises this backdoor.

Bankers believe that allowing commercial giants with massive user data to open banks is a dimensional打击. In 2005, Walmart applied for an ILC charter, triggering a collective uprising across the American banking industry. Banking associations lobbied Congress furiously, arguing that if Walmart Bank used its supermarket data advantage to offer cheap loans only to Walmart shoppers, how could community banks survive?

Under immense public pressure, Walmart was forced to withdraw its application in 2007. This event directly led to regulators "freezing" the ILC. From 2006 to 2019—a full 13 years—the FDIC did not approve a single application from a commercial company. It wasn't until 2020 that Square (now Block) barely broke the deadlock.

But now, this barely reopened backdoor faces the risk of being permanently closed again.

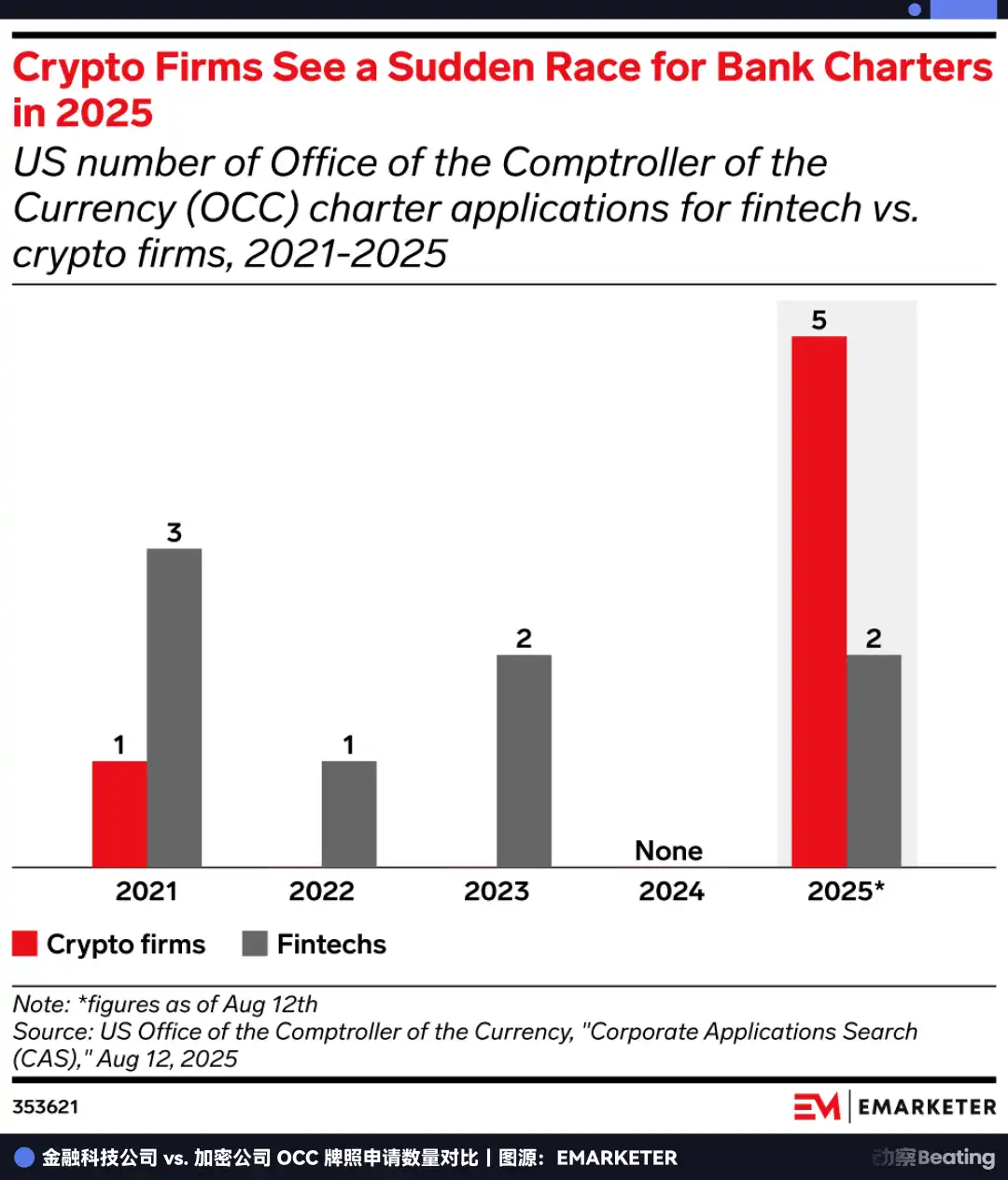

In July 2025, the FDIC suddenly released a notice of proposed rulemaking regarding the ILC framework, seen as a strong signal of regulatory tightening. Meanwhile, related legislative proposals in Congress have never stopped.

Thus, a mad rush for charters began. In 2025, U.S. bank charter applications hit a historical peak of 20, with the OCC (Office of the Comptroller of the Currency) alone receiving 14 applications—equivalent to the total of the previous four years combined.

Everyone knows this is the last chance before the door closes. PayPal is racing against the regulators. If you don't rush in before the loophole is彻底堵死 by law, this door might close forever.

A Breakthrough for Survival

The charter PayPal is going to such lengths to obtain is essentially an "option."

Its current value is certain: independently issuing loans and profiting from the interest margin in a high-rate environment. But its future value lies in qualifying PayPal to enter currently forbidden but highly imaginative territories.

Look at the business Wall Street covets most. It's not payments; it's asset management.

Without a bank charter, PayPal could only act as a simple passerby deity, moving funds for users. But once it possesses an ILC charter, it gains a legitimate custodian身份.

This means PayPal can rightfully custody Bitcoin, Ethereum, and even future RWA assets for its 430 million users. Going a step further, under the future《GENIUS Act》framework, banks might be the only permitted legal入口 connecting to DeFi protocols.

Imagine a future where a "High-Yield Savings" button appears in PayPal's App, connecting in the backend to on-chain protocols like Aave or Compound, with PayPal Bank bridging the insurmountable compliance barrier in between. This would彻底打破 the wall between Web2 payments and Web3 finance.

On this dimension, PayPal is no longer competing with Stripe on fees; it's building a financial operating system for the crypto era. It's attempting to evolve from processing transactions to managing assets. Transactions are linear and have a ceiling; asset management is an infinite game.

Understanding this layer allows you to grasp why PayPal is launching this charge at the end of 2025.

It is acutely aware that it is caught in the cracks of the era. Behind it is the fear of its traditional payment business profits being zeroed out by stablecoins. Ahead is the urgency of the ILC regulatory backdoor being permanently welded shut.

To squeeze through this door, it had to sell $7 billion in assets in September to刮骨疗毒, solely to换取 the entry ticket that determines its survival.

If you stretch the timeline back 27 years, you see a轮回 filled with宿命感.

In 1998, when Peter Thiel and Elon Musk founded the precursor to PayPal, their mission was to "challenge the banks," to use electronic money to destroy those old, inefficient financial institutions.

Twenty-seven years later, this former "dragon-slaying youth" is straining every muscle to "become the bank."

In the business world, there are no fairy tales, only survival. On the eve of cryptocurrency重构 the financial order, continuing to be an "ex-giant"游离于 the system之外 means certain death. Only by obtaining that身份, even if through "using the backdoor," can it survive into the next era.

This is a生死突围 that must be completed before the window closes.

If it wins the bet, it becomes the J.P. Morgan of the Web3 era. If it loses, it becomes merely a relic of the previous internet age.

Time is running out for PayPal.