Original Author: Sanqing, Foresight News

On March 24 (Eastern Time), the share price of stablecoin issuer Circle (CRCL) closed at $101.17 on the New York Stock Exchange, marking a single-day drop of over 20%, its largest single-day decline since going public. Its largest distribution partner, Coinbase (COIN), also fell nearly 10% in sync, closing at $181.04 on the Nasdaq.

The trigger for the sell-off was the leaked details of the latest draft text of the Clarity Act. The draft intends to prohibit digital asset service providers from "directly or indirectly" paying yields on stablecoin balances, and also bans any structural arrangements that are "economically or functionally equivalent to interest."

Image Source: Tweet by Eleanor Terrett, host of Crypto in America and former Fox Business reporter

On the same day, its competitor Tether announced that it had hired one of the Big Four accounting firms to conduct its first full financial audit (including the USDT reserves).

"Directly or Indirectly": Who Do These Five Words Block?

The draft text was submitted to crypto industry representatives for review in a closed-door meeting on March 24, with banking representatives to follow for review the next day. Reporter Eleanor Terrett disclosed the draft details on X, citing a related email.

USDC itself has never paid interest, and Circle, as the issuer, has never paid any yield to holders. So, what does the draft's prohibition on issuers paying interest have to do with Circle?

The draft's "scope" extends beyond the issuer. The entity actually paying yields to users is Coinbase.

According to the revenue-sharing structure disclosed in Circle's prospectus, 100% of the reserve interest for USDC held by users on the Coinbase platform belongs to Coinbase; for USDC circulating outside the platform, 50% of the reserve interest belongs to Coinbase.

Coinbase passes on the vast majority of the reserve proceeds obtained on-platform to users in the form of "USDC Rewards." According to an analysis by Columbia Law School, Coinbase's profit margin on USDC Rewards is extremely thin, retaining only about 20 to 25 basis points.

The "directly or indirectly" and "economically or functionally equivalent to interest" clauses in the Clarity Act draft are precisely designed to block this loophole.

This ban may have a limited financial impact on Coinbase, or could even be positive. Coinbase is both a shareholder of Circle and holds a pure profit share of 50% of the reserve income from off-platform USDC. Its commercial incentive to promote USDC will not disappear because of this.

However, USDC's competitors are not only USDT but also the US dollar itself.

USDC Rewards allowed USDC to play the de facto role of a "digital high-yield savings account." This has also been one of the drivers behind USDC's growth rate outpacing USDT's for two consecutive years. Once this channel is closed, users holding USDC would see yields drop to zero, reducing their willingness to hold it.

The path of demand contraction points to Circle. Weakened holding motivation on the retail end leads to a slowdown in the growth of the total circulating supply of USDC. The speed at which the reserve pool thickens subsequently decreases, and Circle's revenue growth story, built on the expectation of scale expansion, begins to loosen.

The draft also preserves an exemption for "activity-based rewards." Rewards linked to payments, transfers, or platform usage are still permitted. But this is a completely different product from the current "hold-to-earn" model.

Furthermore, the standard phrasing "economically or functionally equivalent to interest" is overly vague, leaving significant room for interpretation by future regulators. The boundaries of activity-based rewards also face the risk of being tightened.

Another Pressure on the Same Day

If the Clarity Act draft is dismantling Circle's growth flywheel, then the audit announcement made by Tether on the same day targets another competitive advantage of Circle.

USDC's long-term differentiation narrative has largely been built on compliance.

Circle regularly undergoes reserve attestations from top-tier accounting firms. During the years when regulatory uncertainty weighed on Tether, "We are the transparent and compliant one" was an extremely effective card for institutional clients and compliance-sensitive exchanges.

Tether, on the other hand, relied on quarterly attestations rather than full audits to respond to the outside world. S&P Global had previously assigned USDT a "weak" credit rating in 2025, warning of under-collateralization risks if Bitcoin prices fell further.

Additionally, the GENIUS Act requires large stablecoin issuers to undergo annual independent audits. Tether's hiring of a Big Four firm seems more like a response to this legal obligation. Regardless of the motive, the timing of this signal was enough to add to the market's negative sentiment.

USDC's growth rate has outpaced USDT's for two consecutive years. The narrative of compliance and transparency has been one of the most important drivers of this growth. Tether's hiring of a Big Four auditor has not yet begun, and the results are far from known. But if the audit is completed successfully, it is obvious that the compliance premium that Circle relies on to maintain its growth advantage will be compressed.

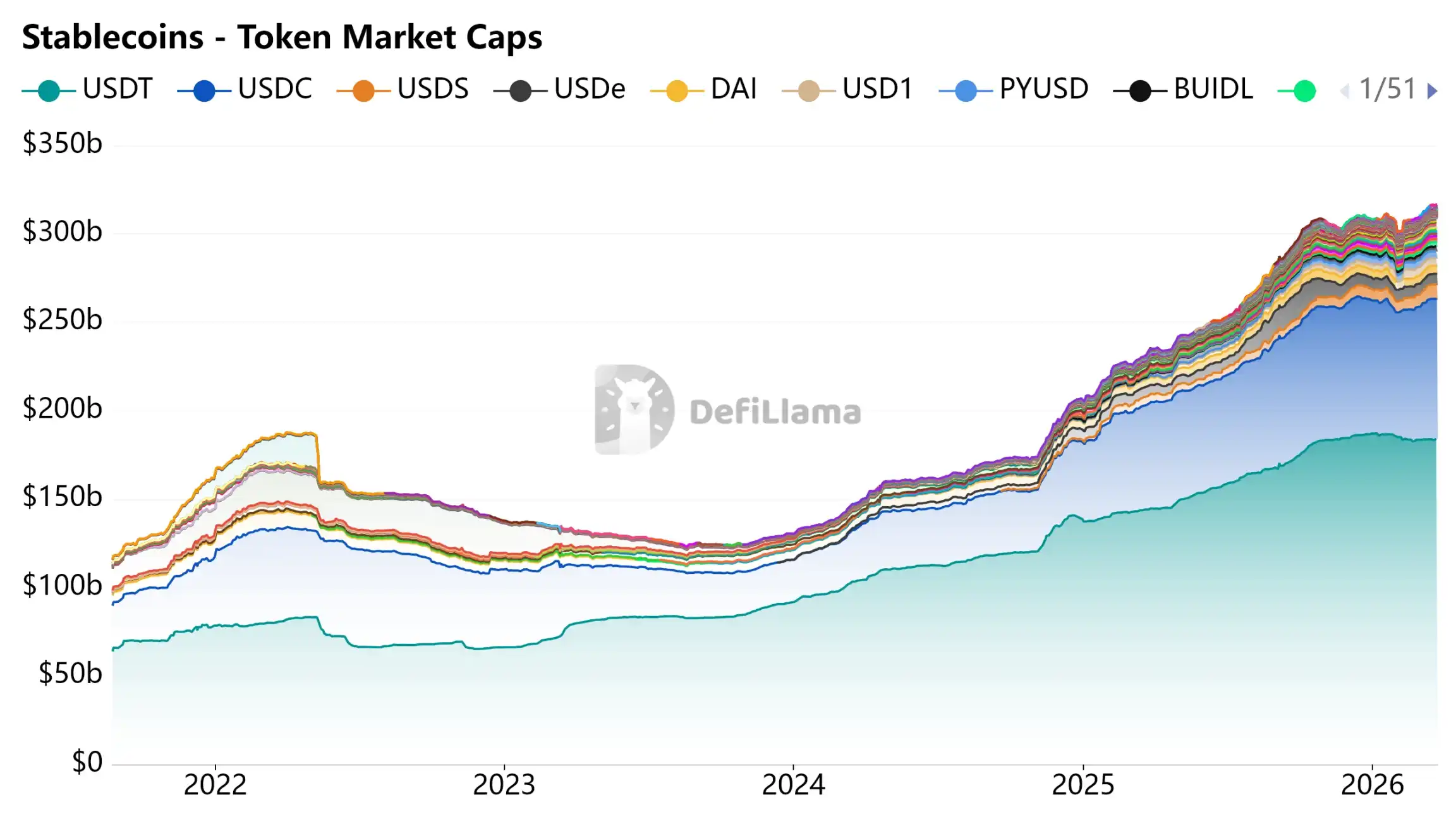

Image Source: DeFiLlama - Stablecoins

Payment Tool, Not Savings Account

Circle's value benefits from its growth model: yield incentives drive users to hold USDC, scale expansion leads to a thickening reserve pool, and reserve interest supports revenue growth. For this model to work, the premise is that stablecoins are allowed to play the role of an interest-bearing asset or savings deposit.

The Clarity Act draft is negating this premise at the legislative level.

Without yield incentives, the growth of USDC's scale must instead rely on natural penetration through real payment scenarios. This path is not impassable, but it is much slower and far more uncertain than yield-driven growth.

Compliance preserves Circle's license, but it does not preserve its growth model. The bankers' answer is clear: stablecoins can exist, but they cannot bear interest.