The U.S. Federal Reserve is now operating at a financial loss, and is months away from having negative tangible equity for the first time in modern history.

This article explores how we got here and to what extent any of this matters for savers and investors.

Commercial Bank Assets and Liabilities

A commercial bank has a considerable amount of both assets and liabilities. In order to remain solvent, the asset side must exceed the liability side, and they have various regulations placed on them to try to keep them as solvent as possible.

For a typical bank, their liabilities mainly consist of deposits. Individuals or businesses deposit money at the bank, and those deposits in various forms (checking accounts, savings accounts, certificates of deposit, and so forth) are considered liabilities or “IOUs” for the bank and assets for the depositors. That serves as the source of financing for banks; they are basically borrowing from depositors at very low rates.

On the other side of the ledger, bank assets consist of various loans, securities, and cash that they hold at their central bank. The loans and securities can include mortgage loans, business loans, personal loans, credit card loans, various Treasury securities, and other more complex securities.

To use Bank of America (BAC) as an example, they have $3.051 trillion in assets and $2.778 trillion in liabilities as of the end of 2022. Their assets exceed their liabilities, meaning they have positive shareholder equity. Even when we factor out some intangible items, mainly referring to their $69 billion in goodwill, their equity is still positive.

And importantly, Bank of America’s assets generate a much higher average yield than their liabilities, so they have positive interest income. They pay a small amount of interest income to their depositors, and collect way more interest income on their various assets.

Central Bank Assets and Liabilities

A central bank has a rather similar balance sheet structure to a normal commercial bank, with assets and liabilities as well. For the United States, the central bank is called the Federal Reserve.

Liabilities of the Federal Reserve consist mainly of bank deposits and banknotes. Much like how individuals and businesses deposit their cash at a commercial bank, commercial banks deposit their cash at the Federal Reserve. These deposits, known as “reserves” are assets for the banks and liabilities for the Federal Reserve, and the Federal Reserve pays interest on them. The U.S. Treasury Department also maintains a cash account at the Federal Reserve, and this represents basically the checking account of the federal government. Reverse repo operations are also liabilities of the Federal Reserve, and they pay sizable interest rates. Lastly, all physical cash dollars are liabilities of the Federal Reserve. These are bearer assets that are kind of like having a deposit at the Fed, except they are physical and can be traded around. The Fed pays no interest on its physical bank note liabilities, and gets to set the rate it pays on its bank reserve and reverse repo liabilities.

Assets of the Federal Reserve consist mainly of Treasuries and mortgage-backed securities, and most of those came from prior rounds of quantitative easing. To perform quantitative easing, the Federal Reserve created more liabilities (bank reserves) for itself and used those to buy more assets (Treasuries and MBS) for itself. At the time they did this, Treasuries and MBS paid higher interest rates than bank reserves.

The Federal Reserve has a small number of other items that count as assets or liabilities, but those listed above represent the vast majority of the balance sheet. In 2021, the Federal Reserve earned $100 billion in net interest income. Some of it went to pay for operating expenses of the Federal Reserve, and some of it was paid out as a dividend to the shareholders of the Federal Reserve (which are the commercial banks themselves). The majority of the profit was handed to the U.S. Treasury. By law, that’s how it works, and the Federal Reserve is a source of profit for the U.S. federal government.

And that detail is actually pretty important. A central bank is “supposed” to be mostly independent from their government. They are overseen by the government, but not funded by the government. If a central bank loses its independence, and for example a president can tell the central bank to do whatever he wants, then a country has basically lost its guardrails against hyperinflation. Central bank independence, while not perfect, is an attempt to partially decentralize control of the financial system so that it’s harder to manipulate for short-term political reasons such as elections.

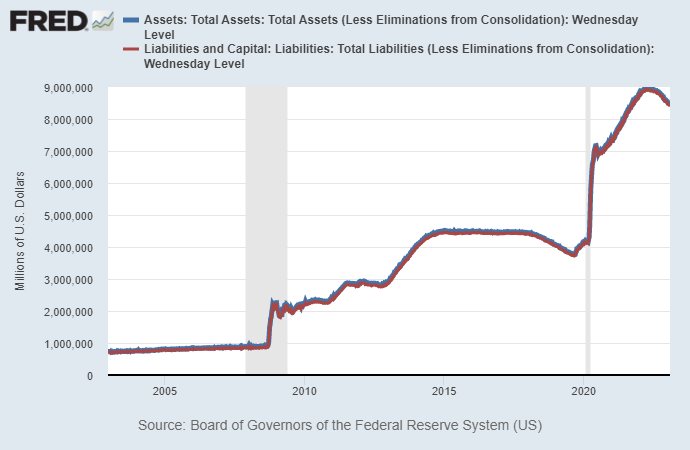

This chart shows the Fed’s assets in blue and liabilities in red, and by extension also shows how thin their equity is:

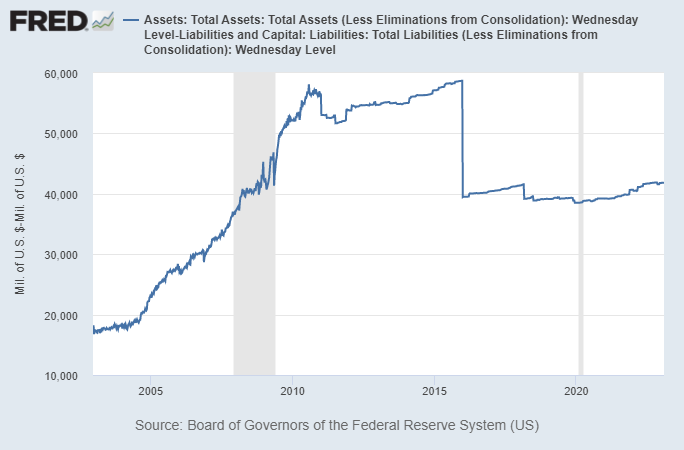

This chart shows the Fed’s equity over time, which is the difference between the two lines in the chart above. It is currently $41.8 billion, at least on paper:

How They Became Unprofitable

In September 2022, the Federal Reserve began operating at a loss.

This is because they had raised interest rates unusually quickly throughout the year, including on their own liabilities. Meanwhile, most of their assets are long-duration, meaning that their various U.S. Treasuries and mortgage-backed securities are locked in at lower fixed-rate interest rates and don’t adjust upwards. As a result, the Federal Reserve is now paying out more interest in liabilities than it is earning on its assets.

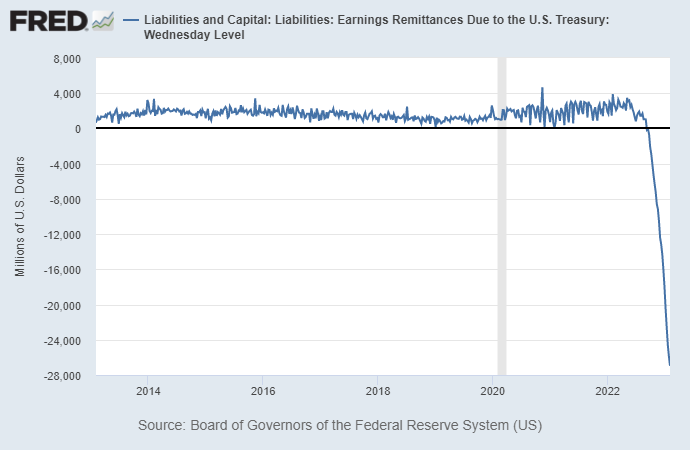

This St. Louis Fed chart shows the Federal Reserve’s weekly remittances to the Treasury Department, and it looks very “doomy”:

However, the chart is flawed because it changes its calculation method mid-chart once it turns negative. The smaller positive numbers show how much the Fed was sending every week (around $2 billion on average) but when it turns negative, it switches to a cumulative calculation and thus falls off like a cliff.

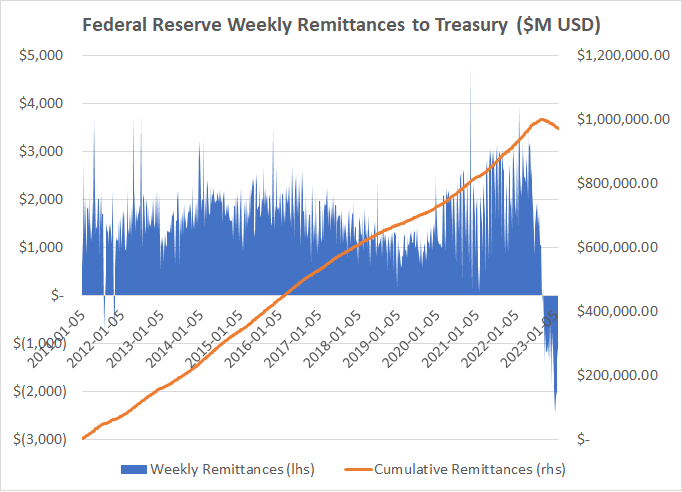

Here’s an adjusted version of the chart, using the same data from the St. Louis Fed, that I put together. It shows the weekly figures consistently in blue on the left axis and the cumulative amount since January 2011 consistently in orange on the right axis. It gives a better idea of what’s actually going on:

From January 2011 until September 2022, the Federal Reserve paid approximately $1 trillion in cumulative remittances to the U.S. Treasury, which was a nice revenue source for the government. Now, those payments aren’t flowing anymore.

In a few months, the Federal Reserve will have lost enough money from this negative net interest income, that it will have negative tangible equity. In other words, its financial liabilities will exceed its financial assets. However, thanks to some accounting gimmicks, their reported equity is basically unchanged.

When the Federal Reserve operates at a loss, it doesn’t send a remittance to the Treasury. Furthermore, they make a note of how much they lost, and if they ever become profitable again in the future, they get to pay back their cumulative losses to themselves with those profits, before they would return to sending remittances to the Treasury.

So, in order for the federal government to get any part of this lucrative $100+ billion/year income stream back, first the Federal Reserve needs to become profitable, and second the Federal Reserve has to maintain that profitability long enough to have paid back all of its cumulative losses. At that point, it would resume paying remittances to the Treasury.

Normally, when the Federal Reserve’s net income is positive, the amount of money that they owe to the Treasury Department is listed as a liability, since they are about to hand it over as a remittance. However, by accumulating losses, this liability becomes negative. And what is a negative liability? An asset!

Here’s how the Federal Reserve describes the issue on their weekly balance sheet report:

The Federal Reserve Banks remit residual net earnings to the U.S. Treasury after providing for the costs of operations, payment of dividends, and the amount necessary to maintain each Federal Reserve Bank’s allotted surplus cap. Positive amounts represent the estimated weekly remittances due to U.S. Treasury. Negative amounts represent the cumulative deferred asset position, which is incurred during a period when earnings are not sufficient to provide for the cost of operations, payment of dividends, and maintaining surplus. The deferred asset is the amount of net earnings that the Federal Reserve Banks need to realize before remittances to the U.S. Treasury resume.

So, the Fed’s cumulative losses become negative liabilities, and thus are referred to as deferred assets. These deferred assets represent the total amount of money that the Fed gets to pay themselves back if they ever become profitable again.

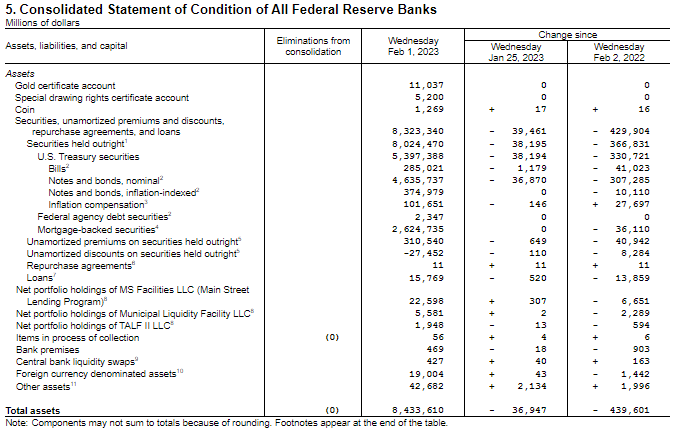

The Fed’s assets:

The Fed’s liabilities:

Right now, the Fed’s assets officially exceed their liabilities by $41.8 billion. However, this includes $27 billion in deferred assets (negative liabilities), and the deferred assets continue to pile up each week. In a matter of months, the deferred assets will exceed $41.8 billion, meaning that the Federal Reserve will have negative tangible equity.

The only thing that will be keeping their assets at a higher level than their liabilities on paper, are these placeholder deferred assets that represent the fact that the Federal Reserve can pay itself back first before resuming remittances, if it ever becomes profitable again.

What Does It Mean?

Alright, so the central bank that underpins the global reserve currency is operating at a loss and is about to have negative tangible equity. That’s… awkward. But what does it mean in practice?

If we go all the way back to 1934, we find a similar situation. From 1913 when the Federal Reserve was created until 1933, the Federal Reserve was required to hold gold as an asset in order to support the redeem-ability of its dollar banknotes at $20.67 per ounce of gold. In 1933, U.S. federal government ended redeem-ability of the dollar for gold, and in 1934 forced the Federal Reserve to hand over all of its gold to the U.S. Treasury Department.

However, the problem was that if the Federal Reserve did that, it would have negative equity, since it would still have the same liabilities but would lose a big chunk of its assets. And if it has major negative equity, then it’s not really an independent central bank as it is supposed to be; it’s just an arm of the government. So, in order to avoid rendering the Fed insolvent (and thus dependent) with that action, the Treasury also gave the Fed an equal amount of gold certificates that equaled the value of the gold they were handing over to the Treasury. It was just a “trade”, in other words.

The gold certificates theoretically represent a claim to the gold, but are non-redeemable, and thus don’t really mean anything. A non-redeemable certificate for something is like a mother giving her child a pretend toy steering wheel in the back seat of a car to have fun and think he is driving, while the mother actually drives the car.

But from a legal accounting perspective, those gold certificates kept the Federal Reserve solvent by avoiding any reduction in official value from the asset side of their balance sheet, and have been held by the Fed for almost 90 years now. They’re just accounting placeholders. And due to decades of inflation, the gold certificates which were once a core part of the Federal Reserve’s balance sheet, are now a tiny component of the balance sheet and don’t matter anymore.

So, what happens when the Federal Reserve’s tangible equity turns negative later in 2023? Nothing. At least not immediately.

Unlike a commercial bank, a central bank can just keep functioning with negative equity and indefinite losses. Positive equity is just an imaginary line to preserve the idea of central bank independence, and can be maintained with accounting gimmicks. It’s like standing somewhere deep out in the wilderness right on some unguarded part of the border between Canada and the United States; the line might as well not even be there. Deferred assets are the modern equivalent of non-redeemable gold certificates.

Or, to quote Matthew McConaughey’s character from Wolf of Wall Street:

Fugahzi, fugayzi, it’s a whazzy, it’s a whoozy, it’s a [whistle], it’s FAIRY DUST! It doesn’t exist. It’s never landed. It’s no matter. It’s not on the elemental chart. It’s not fucking real. Alright?

Fed Broke Fugazi

The financial system in the United States, and for most of the rest of the world for that matter, can basically be thought of as an Excel spreadsheet managed by the Federal Reserve. That’s all it really is. Some of the cells on the spreadsheet are assets, and some of the cells are liabilities. It’s just a ledger that they administrate, and that we all use. They do, however, have to follow certain laws regarding the administration of their ledger.

Commercial banks manage their own ledgers, which are sub-ledgers of the Federal Reserve, since the cash assets of commercial banks are listed on the Federal Reserve’s spreadsheet as liabilities.

Okay But Seriously, What Does it Mean?

The Federal Reserve’s soon-to-be negative tangible net equity won’t matter at first, and for most people won’t even be noticed. However, over the long-term, this is actually somewhat relevant.

Firstly, the Treasury just lost a $100+ billion annual revenue source. That might not sound like much these days, but it’s about four times the size of NASA’s annual budget. The federal government just lost four NASA’s worth of income. Since spending likely won’t be cut on anything to make up for this, this represents an extra $100+ billion in debt that the federal government has to issue each year as long as this income source is gone.

Secondly, this is pretty good for U.S. commercial bank profitability, all else being equal. The money that used to flow to the U.S. Treasury in remittances is now instead flowing to the U.S. commercial banking system and money market funds. The interest-bearing liabilities for the Federal Reserve are interest-bearing assets for U.S. banks, money market funds, and entities like that.

Thirdly, the longer this goes on, the more it could raise political pressure. Politicians, such as perhaps Senator Warren given her track record of prior commentary, could criticize the Federal Reserve for paying out tens of billions of dollars of interest to banks for their risk-free reserve balances, and paying a lot of interest for reverse repo activity as well. The problem, however, is that the reason that the Federal Reserve is paying such high interest on its liabilities, is because that is a key mechanism for how the Federal Reserve controls short-term interest rates these days. If they want to maintain control over the price of money, this is a key part of how they do it. They are basically “paying banks not to lend” to try to curtail bank lending, in a manner of speaking. More precisely, they are using interest rates on bank reserves as a floor for the interest rate that banks would charge borrowers for any type of loan.

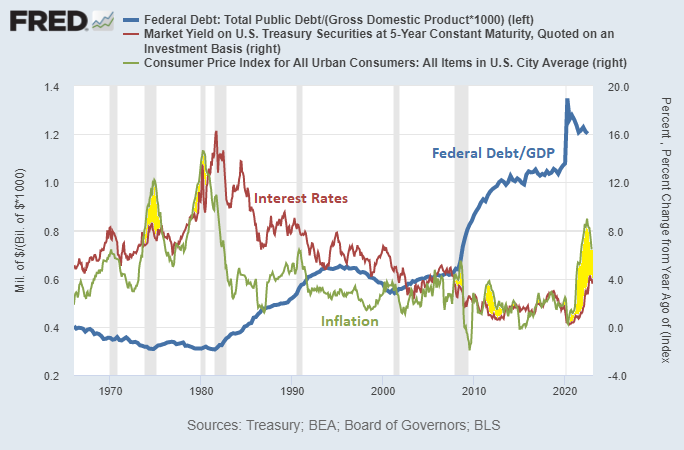

By the end of this decade, I have considerable concerns regarding a fiscal spiral occurring in the United States and other developed countries, meaning that a combination of high deficits, high debts, and high interest rates on those debts, will all work together to create structural inflation and money supply growth. The Federal Reserve entering into negative tangible equity is just another piece of that process unfolding, since it contributes to larger federal deficits by taking away Treasury remittances.

For decades, structurally higher debt-to-GDP levels in the United States were offset by declining interest rates on that debt, which kept absolute interest expense by the federal government from growing. However, now interest rates are potentially trending sideways and deficits and debts continue to pile up:

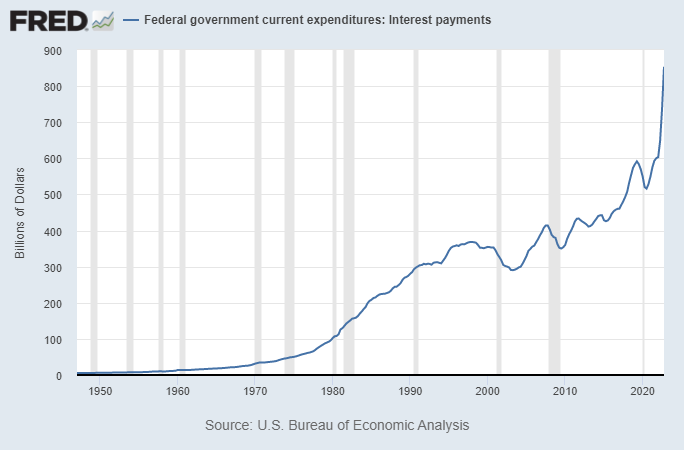

As a result, absolute interest expense on the federal government’s debt is breaking out after a period of consolidation:

In a future article in the upcoming months, I plan to write about the relationship between interest rates and inflation, to specifically analyze under which conditions higher interest rates can quell inflation and under which conditions higher interest rates can actually exacerbate inflation.

In the meantime, for a breakdown on how money creation works in the modern financial system, my article “Banks, QE and Money-Printing” is worth a read.