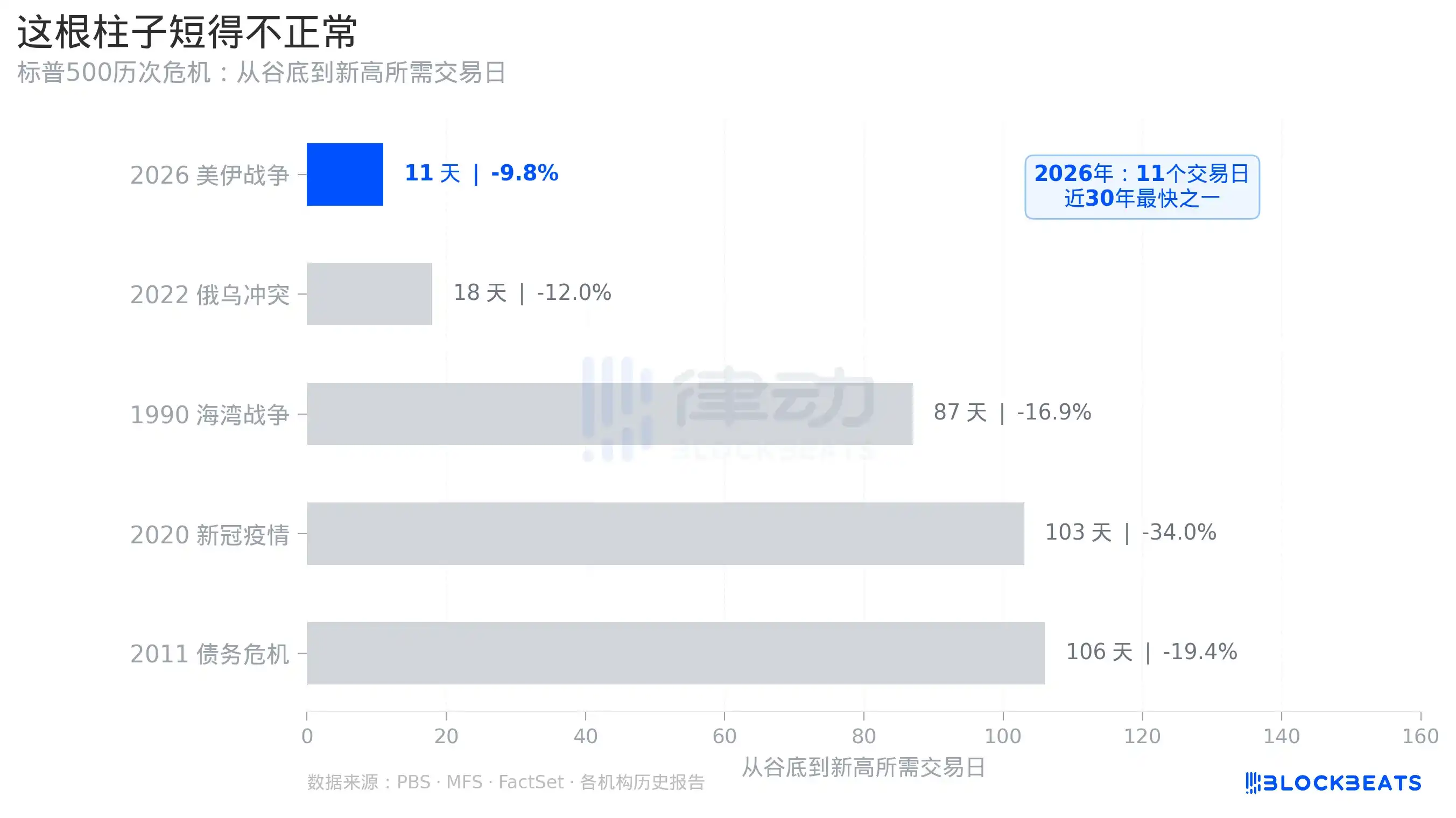

On April 15, the S&P 500 closed at 7,022.95 points, exactly 77 days after it last hit a record high. In those 77 days, the U.S. fought a war, oil prices broke above $100, and the stock market experienced its fastest 10% correction in five years. Then, it returned to a new high in about 11 trading days.

This number is worth pausing to think about. 11 trading days—this is an impossible speed in U.S. history following every crisis of a similar scale.

What 11 Trading Days Mean in History

Where does the speed of this recovery stand in the historical context?

According to a PBS report, JPMorgan strategists called this rebound "the fastest since the COVID-19 pandemic." Looking at the historical numbers, this statement is not an exaggeration.

During the COVID-19 pandemic in 2020, the market took about 103 trading days to rebound from the low on March 23 to a new high on August 18. During the Gulf War in 1990, it took about 87 trading days from the low at the end of October to return to the previous high in February 1991. During the U.S. debt crisis in 2011, it took about 106 trading days from the low in October of that year to a new high in March 2012.

This recovery from the 2026 Iran War: 11 trading days.

It should be noted that the magnitude of this correction (about 10%) was much smaller than during the COVID-19 period (about 34%) and 2011 (about 19%). But even compared to the 2022 Russia-Ukraine conflict, which had a similar decline, that recovery took about 18 trading days. Eleven days is still an outlier.

The narrative of this correction has always been "ceasefire expectations," not "deteriorating economic fundamentals." The market fell due to uncertainty, not profits. When ceasefire news actually emerged, the uncertainty pricing was quickly erased, without waiting for quarterly reports to rebuild confidence.

The Word "Ceasefire" Drove the Rally—Twice

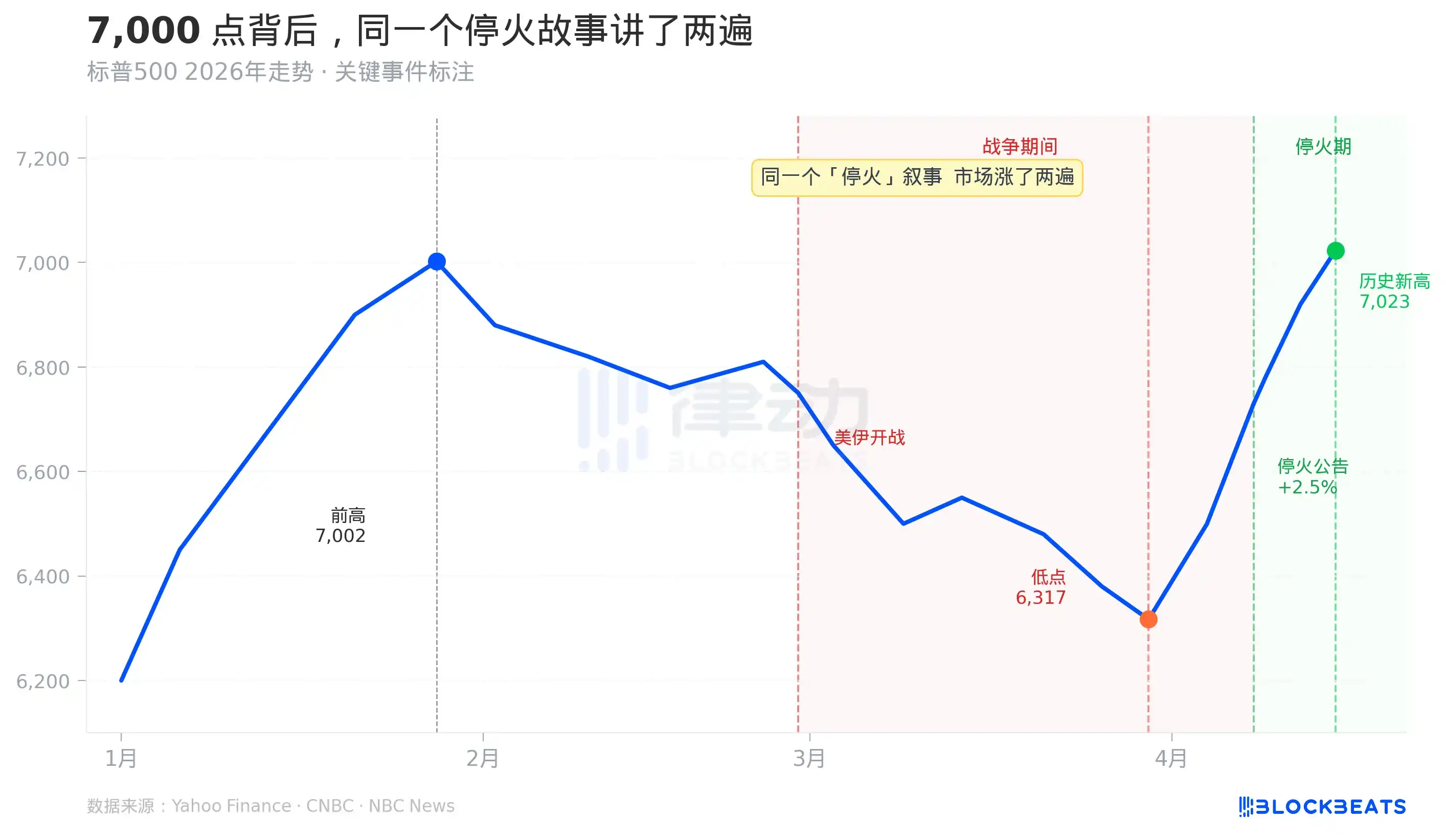

To understand the speed of this recovery, it’s necessary to first clarify the news timeline.

On February 28, the U.S. and Israel launched military strikes against Iran. The S&P 500 began falling from its previous high of 7,002 points on January 28, dropping to 6,316 points by March 30, a maximum drop of nearly 10%. By Wall Street's definition, this was right on the edge of a "correction."

But during this decline, something strange happened. On March 24, rumors about the "possible unblocking of the Strait of Hormuz" circulated in the market, and the S&P rebounded that day. This was the first "ceasefire pricing." The rumors were later disproven, and the market continued to fall.

On April 8, Trump announced a two-week temporary ceasefire on social media, and Iran also accepted Pakistan's mediation proposal. The S&P 500 surged 2.5% in a single day. This was the second "ceasefire pricing," at a higher price, for almost exactly the same reason.

As shown in Chart 1, the two sharp rallies correspond to symmetrical event annotations, both labeled "increased possibility of ceasefire." It rose the first time, and then rose again the second time. As of April 15, when the new record high was set, the two-week temporary ceasefire agreement had not yet expired, and not a word of a permanent peace agreement had been signed.

What scenario is the market pricing in? Not "the end of the war," but "the possibility that the war could end." This expectation was priced—twice.

The Fear Index Is Lower Than Before the War

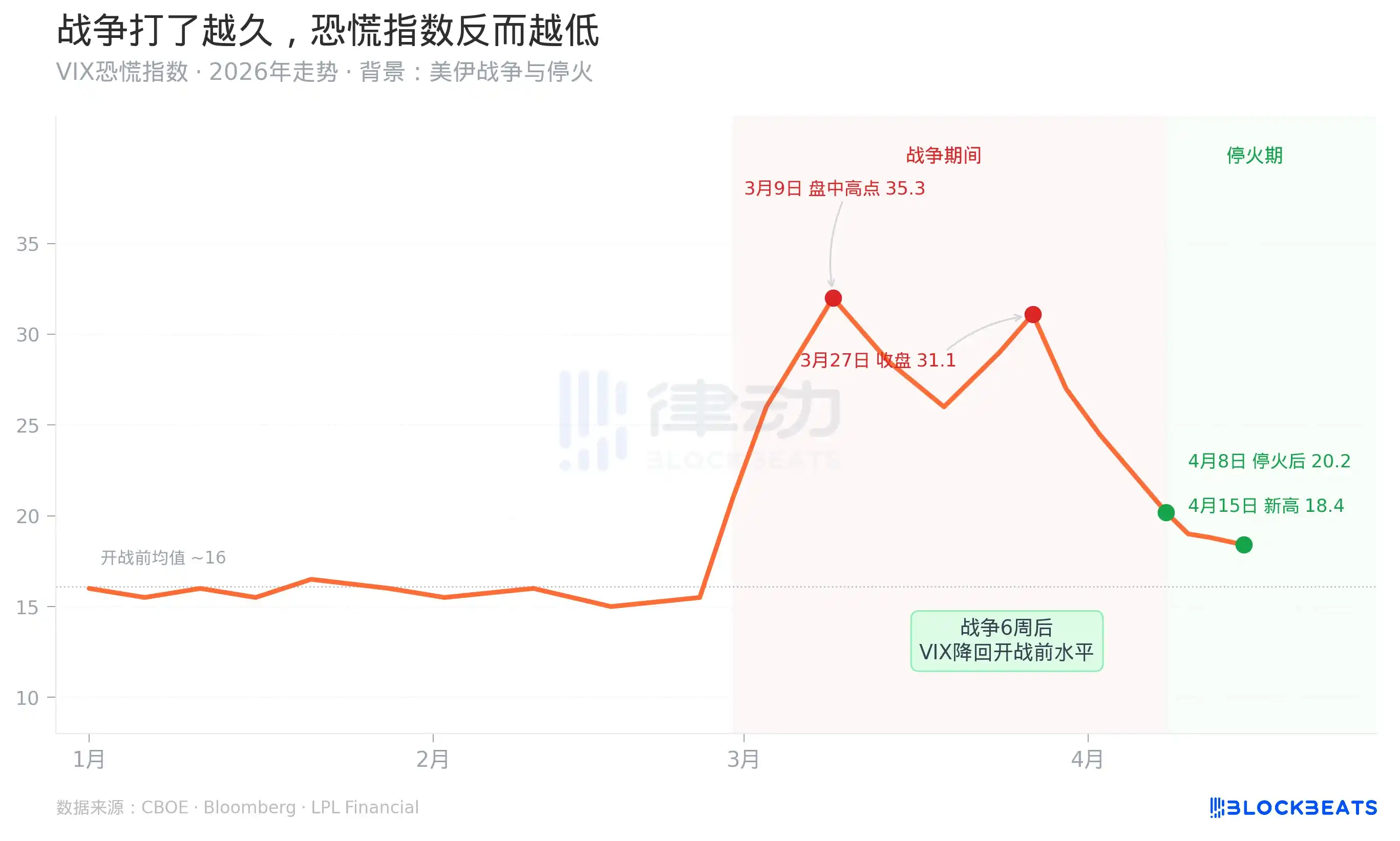

Even more counterintuitive is the number for the VIX, the index Wall Street uses to measure market panic.

When the war started on February 28, the VIX jumped from around 16 to touch 35.3 intraday on March 9. This aligns with common sense: war is a risk, and the market prices in uncertainty.

But the subsequent trend defies common sense. Starting from March 9, even as the war continued, oil prices rose, and the Senate voted on whether to authorize war powers, the VIX steadily declined. By April 15, the day the S&P hit its new record high, the VIX closed at around 18.4, lower than its level before the war started on February 28.

What does this mean? It means the market has reclassified this war from a "source of uncertainty" to a "calculable risk." Within six weeks, an ongoing war went from a "panic event" to "quarterly raw material."

This was achieved by a very specific financial mechanism. According to a CNBC report, JPMorgan's Q1 2026 trading division revenue reached $11.6 billion, a historical record, up 20% year-over-year. Fixed income division revenue was $7.1 billion, primarily driven by commodities, currency, and emerging market trading—precisely the areas where the Iran war generated the most "volatility."

In other words, while ordinary investors were feeling fear, professional institutions were harvesting volatility as profit. The more efficiently this mechanism operates, the more inclined the market is to "digest" the war, and the faster the VIX falls.

The Commercialization of Volatility

On April 15, the same day the S&P 500 hit a record high, the Pentagon announced the deployment of an additional 10,000 troops to the Middle East, and the Senate rejected the war powers authorization bill for the fourth time. These two things happened on the same day, and the market had no reaction to them.

As shown in Chart 4, the bar for JPMorgan's Q1 2026 trading revenue is significantly higher than the previous eight quarters. This isn't a marginal improvement; it's a jump.

Supporting this jump are the profits hedge funds and market makers made from war volatility. According to Goldman Sachs Prime Brokerage data, as of April 14, the net long positions of U.S. hedge funds had turned positive for the first time since the end of 2025. During the same period, according to FINRA data cited by Atwater Malick, U.S. stock margin debt hit a record high of $1.28 trillion, up 36% year-over-year.

Three signals appeared simultaneously: hedge funds shifting from short to long, record leverage, and the market hitting record highs. This is a standard "trading on optimism" pattern.

Understanding this pattern involves looking at the financial infrastructure layer. When Wall Street's market makers, derivatives markets, and hedge funds are sufficiently mature, geopolitical shocks are no longer exogenous, unmeasurable risks but rather raw materials that can be priced, hedged, and commercialized. The Iran war, for JPMorgan's trading desk, is not a threat but an opportunity. The same goes for hedge funds that positioned correctly.

This is the true meaning of the "two screens, two worlds" on April 15. The Pentagon is prolonging the war; the market is pricing the end of the war. These two things are not contradictory because, for market makers, how long the war lasts is not important; whether the volatility is large enough is.

Of course, this mechanism has its fragility. The new high in 11 trading days implies an assumption: the two-week ceasefire will be smoothly extended, Iran nuclear negotiations will proceed as expected, and oil prices will fall. If any of these assumptions prove wrong, there is little buffer in the current pricing. The $1.28 trillion in leveraged funds is also an amplifier on the way down.

7,000 points is a price that only holds in the most optimistic scenario.