Original Author / 10x Research

Compiled / Odaily Planet Daily Golem(@web 3_golem)

This article explores the impact of the CLARITY Act on DeFi and analyzes the potential risks for winners and losers in terms of investment if the bill is implemented. While there are clear structural beneficiaries, the final outcome is not one where only one company can benefit. At the same time, investors should also pay close attention to new adverse factors that could affect the overall landscape.

The latest CLARITY proposal effectively ends the narrative of stablecoins as savings products. While revenue sharing is still allowed, the path to passing earnings on to the end user has been cut off. Coinbase can continue to profit from USDC, but it has lost its most powerful growth lever—offering yields to users, which constitutes a structural headwind to its distribution model. Meanwhile, Circle now needs to prove that its arrangements are legitimate profit-sharing, not a circumvention of yields, which brings higher legal risks, potential contract restructuring, and ongoing regulatory scrutiny.

In essence, this is about control over money markets. Stablecoins are strictly defined as payment instruments rather than interest-bearing assets, effectively isolating yields within banks and regulated financial instruments (such as money market funds and ETFs like IQMM), representing a re-centralization of yield.

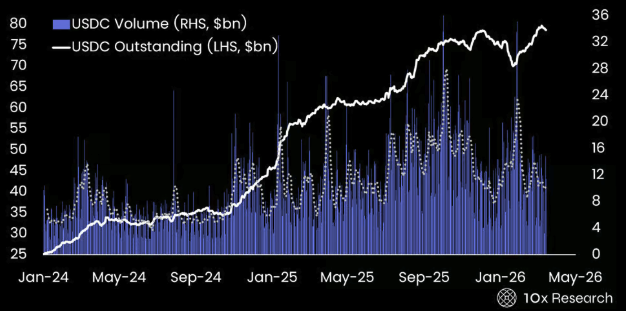

USDC Outstanding Balance vs. USDC Trading Volume

CLARITY Act Implementation Will Be Unfavorable for DeFi

Although the CLARITY framework is structurally favorable to Circle, supporting USDC adoption and valuation, even at the cost of reduced flexibility (e.g., yield sharing, incentive mechanisms) and short-term margin compression, it also presents significant headwinds for DeFi. Many DeFi tokens and activities may require registration and compliance reviews, especially where governance and fee-generation mechanisms resemble equity structures.

Some argue that the CLARITY framework could be beneficial for DeFi, as the yield ban would drive users towards DeFi lending. However, this view presupposes that DeFi remains unaffected by regulation. In reality, the CLARITY framework is likely to extend to front-end interfaces and restrict how stablecoins can be used in DeFi.

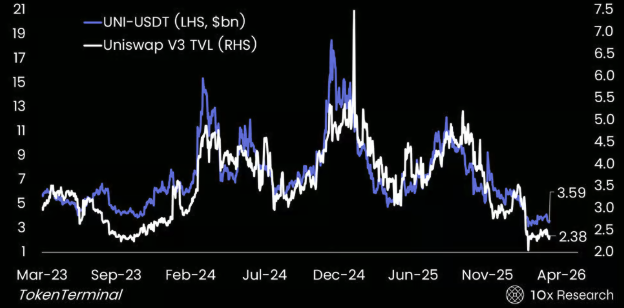

UNI-USDT vs. Uniswap V3 TVL – Weak DeFi Momentum

10x's view is that DeFi is not a beneficiary, but a victim. Structurally, this is bearish for DeFi tokens, as reduced flexibility, increased compliance, and potential restrictions on stablecoin usage will pressure liquidity, activity, and ultimately valuations.

The key overlap lies with stablecoins. Both Circle (CRCL) and Uniswap rely heavily on USDC as core liquidity for trading and settlement. For Uniswap, stricter regulation could pressure front-end interfaces, token listings, liquidity incentive mechanisms, and potentially introduce KYC and compliance layers. This would directly impact fee revenue, token velocity, and permissionless access, potentially leading to decreased trading volume, reduced composability, and shrinking liquidity pools.

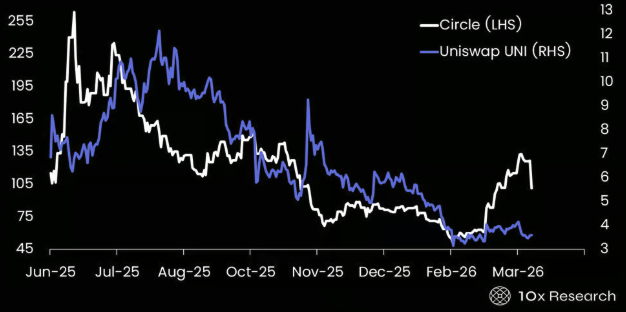

CRCL (White) vs. UNI-USDT (Indigo) – Circle is Decoupling from DeFi

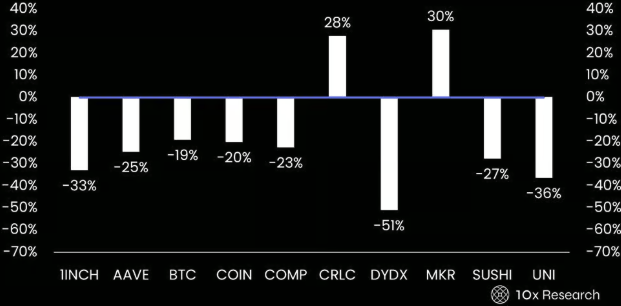

Under the CLARITY Act, the assets most vulnerable are DeFi tokens and governance tokens linked to fee revenue. DEX tokens such as UNI, SUSHI, DYDX, 1INCH, and CAKE face direct risk because their governance-plus-revenue models resemble equity and may require regulated front-ends. Similarly, lending and yield protocols like AAVE and COMP come under scrutiny for their interest-bearing structures and revenue-sharing mechanisms, which could be classified as unregistered financial products.

MKR to Become a Beneficiary in the Yield Re-centralization Trend

The market seems to have largely priced in these factors, so a structural revaluation driven solely by the CLARITY Act is unlikely. MKR has outperformed USDT in 2026, benefiting from its unique positioning in the evolving yield landscape. Unlike most DeFi tokens, Maker captures real yield by investing in US Treasuries and other real-world assets, which is ultimately distributed to MKR holders through a surplus mechanism.

In a regulatory environment where user-level stablecoin yields are increasingly restricted, value is concentrating at the issuer or protocol level, and Maker's structure already positions it to benefit from this shift. Consequently, MKR is priced more as a yield-generating "crypto market equity" rather than a speculative DeFi token. MKR/USDT also appears to be an indicator leading CRCL.

MKR/USDT (White) vs. CRCL (Indigo)

Meanwhile, MKR stands in contrast to stablecoins like USDT, which, while large, do not directly pass economic value to token holders. This creates a structural divergence, especially as high interest rates continue to support Maker's revenue streams.

Importantly, MKR is more of an exception. While most DeFi tokens face headwinds from tightening regulation and restrictions on stablecoin usage, Maker's early integration of real-world assets and its semi-compliant structure make it a beneficiary of the yield re-centralization trend.

More broadly, most DeFi protocols rely on USDC as collateral and settlement infrastructure. If regulation limits how USDC can be used in DeFi, liquidity could decline, trading volume could decrease, and token valuations would come under pressure.

Ultimately, the CLARITY Act may not just regulate crypto, it reshapes the entire DeFi ecosystem. The beneficiaries are likely to be compliant infrastructure providers like Circle, exchanges, and custodians (BitGo), while the losers are tokens associated with permissionless finance and fee extraction. In this context, any token that behaves like equity in a financial protocol (e.g., Uniswap) and is unregulated will face structural downside risk under such a framework.

Is Circle Still Worth Investing In?

According to the latest discussions, the CLARITY Act proposal would prohibit platforms from providing yields to stablecoin holders, directly or indirectly, especially in ways similar to bank deposits. This restriction would apply broadly to digital asset service providers, including exchanges, brokers, and their affiliates, and explicitly target any structure that is "economically or functionally equivalent" to interest.

While the bill allows for activity-based rewards, such as loyalty programs, promotions, or subscription plans, these rewards must not be linked in any way to balances or transaction size, thereby mimicking interest income. In practice, this severely limits how incentives can be structured and clearly draws a line: stablecoins must not operate as interest-bearing deposit accounts.

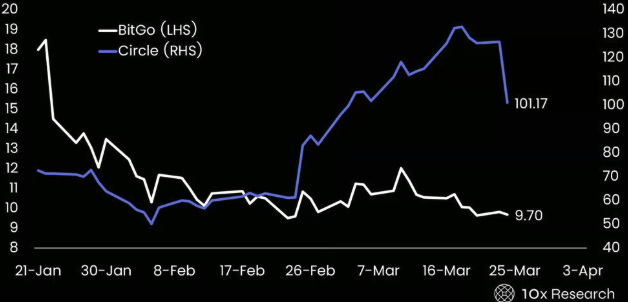

Circle appears to have become a structural winner, while Coinbase faces structural headwinds, and BitGo sits somewhere in between. BitGo's market cap has fallen from about $2-2.5 billion at IPO to about $1.14 billion, making its valuation more attractive as a result. Based on trailing twelve-month performance, the company earned about $57 million, with a P/E ratio of 20x, which is not expensive for a regulated crypto infrastructure provider with a solid institutional position.

BitGo vs. Circle – BitGo's stock fell ~50% rapidly post-IPO

However, earnings quality remains a key constraint. Its reported revenue is inflated by gross transaction volume, while actual profit margins are low (net profit margin below 1%), making BitGo's structure closer to a low-margin custody and execution platform rather than a high-margin balance sheet model like Circle or Tether.

Thus, although BitGo's valuation has become more reasonable after the drop, with improved asymmetry and more limited downside, it remains a low-beta infrastructure company, not a candidate for valuation re-rating. In contrast, Circle still presents a stronger investment opportunity, where changes in regulatory policy could significantly alter its margins and valuation.

Tether hiring a top-tier (Big Four level) auditor would mark a significant step forward in its institutional credibility, indicating improved transparency, governance, and preparedness to operate within a stricter financial regulatory framework. While this does not guarantee a successful listing, it clearly lowers one of the key listing thresholds and could signal a future listing possibility if the regulatory environment becomes more favorable.

This move would have a direct impact on Circle: Increased competition from a more institutionalized Tether could compress Circle's relative valuation premium, but it would also validate the overall effectiveness of the stablecoin model and potentially expand its total addressable market. In this sense, a more transparent and institutionally-aligned Tether would both challenge Circle's market position and reinforce the broader thesis of stablecoins becoming core financial infrastructure.

Even post-CLARITY Act, Circle is unlikely to achieve Tether-like profit margins, but the gap between the two could narrow significantly. Tether's higher margins are due to it retaining almost all reserve earnings, facing fewer regulatory restrictions, and having minimal revenue sharing. Even under the CLARITY framework, which restricts yield pass-through, Circle will still face higher compliance costs, stricter reserve requirements, and likely continued (though renegotiated) revenue sharing with distribution partners like Coinbase.

The CLARITY Act clearly has the potential to improve Circle's profit margins. If yields cannot be passed to users, issuers retain more economic benefit, and Circle's bargaining power in renegotiations increases. Combined with scale and institutional user adoption, this could drive significant margin improvement, gradually moving from the current teens to above 20%.

Circle's valuation is reasonable if USDC continues to grow at a similar pace. Over the past 18 months, USDC's circulation has increased by approximately $46 billion to $79 billion, indicating high adoption rates for USDC. As a settlement and liquidity layer, Circle currently generates approximately $3.2 billion in gross revenue based on a 4% reserve yield, with net revenue of approximately $2.0-$2.3 billion after revenue sharing and costs.

If USDC scales to $1.2-$1.5 trillion, gross revenue could increase to $48-$60 billion; if margins improve to 20%-25%, net income could reach $10-$14 billion. Applying a P/E ratio of 25-30x yields a valuation range of approximately $250-$420 billion, higher than the current market cap of ~$24.5 billion.

However, this valuation framework is highly dependent on continued USDC growth. Recent data shows that USDC supply has begun to stagnate, suggesting the market is already anticipating its growth rate to re-accelerate. Therefore, investing in Circle is no longer just about a valuation re-rating driven by regulatory tailwinds, but increasingly reliant on growth; continued expansion of USDC and improved economics need to materialize to support current share price levels.

10x's base target price for the next 12 months is $120, with potential upside to $150 if USDC growth re-accelerates and margins improve significantly; but there is downside risk to $80 if growth stalls and the current economic situation persists.

Summary

The CLARITY Act accelerates the trend of stablecoins transitioning into regulated products, especially when combined with developments like the GENIUS ETF framework and Treasury-backed structures. The end result is a shift of stablecoin reserves towards regulated money market products. This dynamic is structurally positive for infrastructure players like Circle, but negative for yield-dependent DeFi tokens and protocols.

Prior to the CLARITY Act (if passed), stablecoins were hybrid instruments, functioning as both payment tools and yield generators, while also being core collateral in DeFi. Under the proposed framework, this model shifts fundamentally: stablecoins are defined solely as payment instruments, while yield is confined to regulated products.

This creates a clear reallocation of value. Potential winners include Circle, Treasury-backed ETF structures, and custodians or other compliant financial infrastructure; on the other hand, Coinbase faces reduced monetization flexibility, and DeFi yield protocols and "earn" products face structural headwinds.

In effect, the OCC is not just restricting yield, it is redefining who gets the yield. The result is an economic value transfer from crypto-native channels (Coinbase and DeFi) to regulated financial infrastructure.

The main beneficiaries of the CLARITY Act are likely Circle, MKR, and BitGo, although BitGo's margins remain low, its ~50% drop post-IPO makes its valuation more attractive. On the other hand, Coinbase and a range of DeFi protocols, including 1inch, Aave, COMP, dYdX, Sushi, and Uniswap, are structurally disadvantaged. To some extent, the market has already begun to digest these changes, making the CLARITY Act less of a new catalyst and more of a reinforcement of existing trends.

Year-to-Date Performance of Major DeFi Cryptocurrencies – Winners and Losers