Data Note:BTC uses the spot price of approximately $60,005 on June 28. Company holdings and share capital are based on Strive's latest SEC filing submitted on June 22, with data as of June 18. Market prices and company disclosure times are not perfectly synchronized. Calculations of coverage ratios in this article are snapshot estimates.

1. Summary

On June 16, Strive switched SATA's dividend distribution frequency from monthly to each business day.

Strive calls this the first listed security in the US market to pay dividends on each business day. SATA's current annualized dividend yield is 13%; for July 2026, it has declared a daily dividend per share of $0.0493 for 22 business days, totaling $1.0846 monthly.

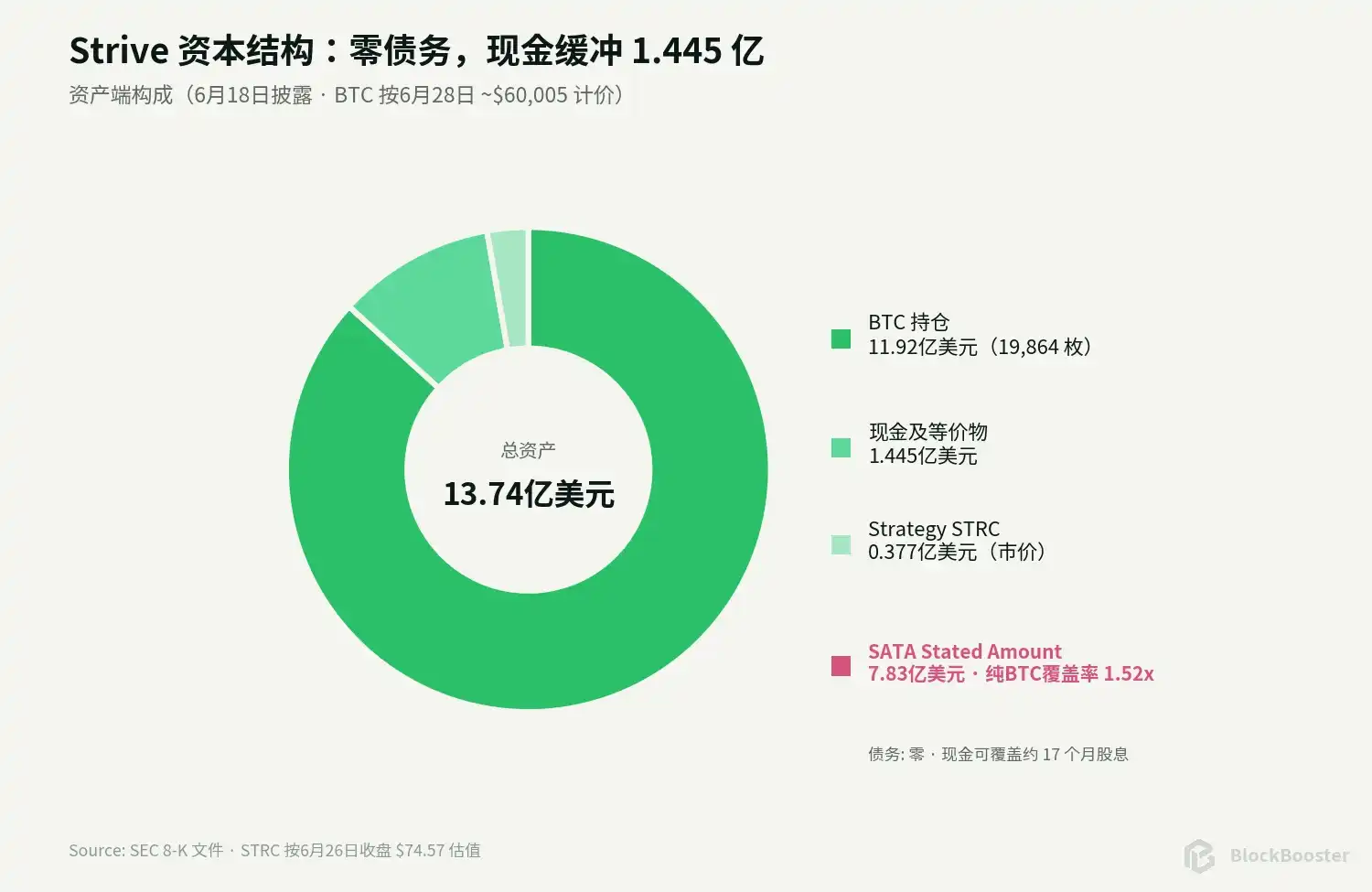

As of June 18, Strive holds 19,864 BTC, $144.5 million in cash, and 505,000 shares of Strategy's STRC Preferred Stock; SATA has 7,829,502 shares issued. Based on a $100 stated amount per share, the principal amount of the preferred stock is approximately $783 million. Using the June 28 BTC price of approximately $60,005, the BTC holding value is about $1.192 billion.

The article's conclusions are as follows:

First, SATA is a layer of corporate preferred equity without a maturity date, whose dividends are deferrable but cumulative. SATA ranks senior to common stock in liquidation but remains junior to company creditors and does not have a direct lien on any specific batch of BTC. Legally, it bears the risk of Strive's corporate credit + BTC balance sheet risk.

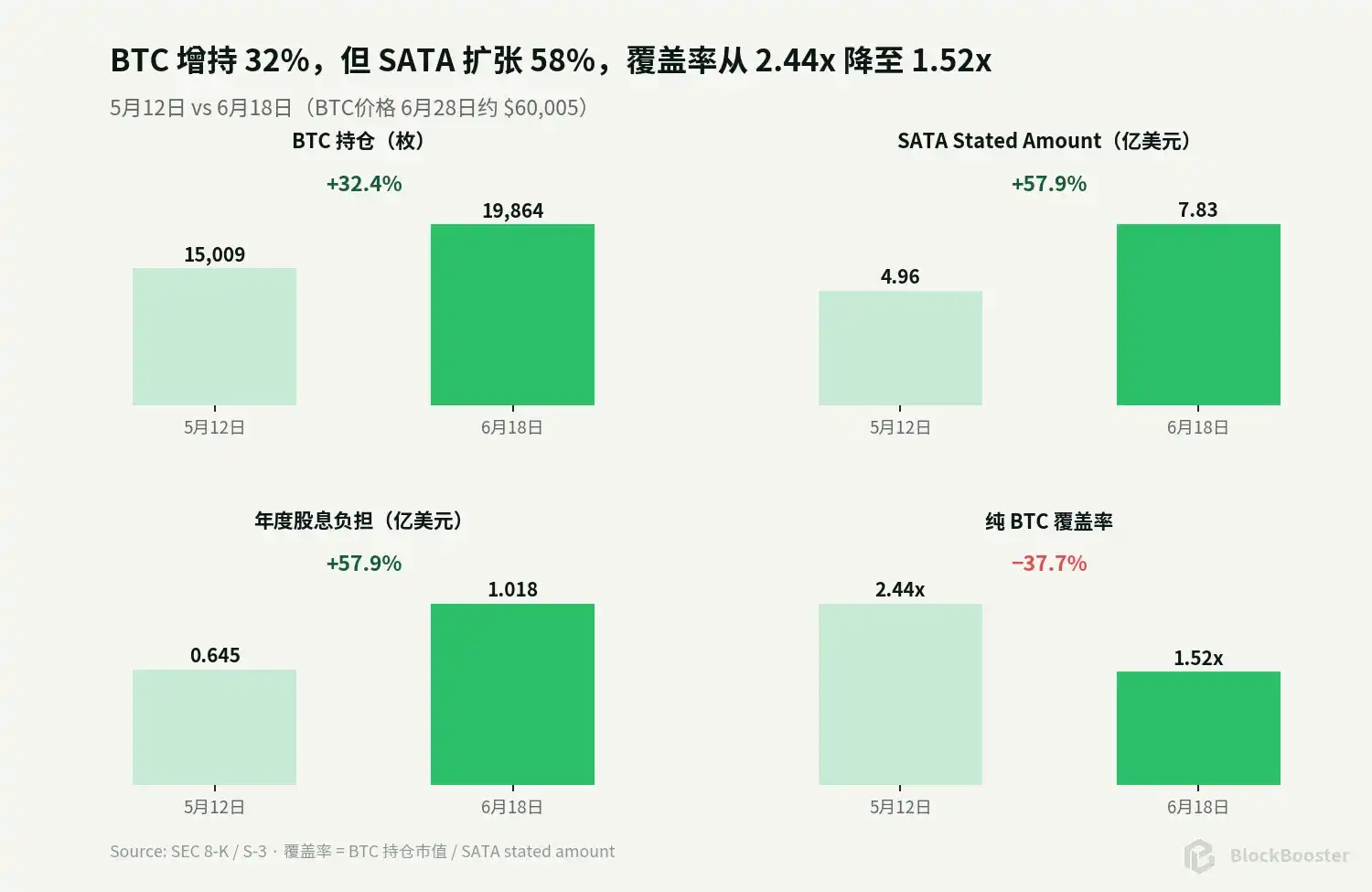

Second, Strive's BTC count continues to grow, but SATA is expanding faster, with coverage ratios significantly compressed compared to May. From May 12 to June 18, BTC holdings increased from 15,009 to 19,864, a rise of about 32.4%; SATA shares increased from 4,959,500 to 7,829,502, a rise of about 57.9%. During the same period, BTC fell from approximately $80,624 to approximately $60,005. The result is that the pure BTC coverage ratio to SATA stated amount decreased from about 2.44x to about 1.52x. If BTC falls another approximately 34.3%, to about $39,416, the pure BTC coverage would drop to 1x.

Third, the cash buffer is substantial but cannot be conflated with collateral. Strive's latest disclosed cash is $144.5 million; valuing the 505,000 STRC shares at STRC's closing price of $74.57 on June 26 gives a value of approximately $37.66 million. The coverage ratio of liquid assets to SATA stated amount is approximately 1.76x.

Fourth, SATA has been repriced by the secondary market. SATA closed at $87.75 on June 26, a 12.25% discount to the $100 stated amount. Based on the $13 annual dividend, the static current yield is approximately 14.81%. Using the latest SOFR of approximately 3.64% as a benchmark, SATA's market current yield spread is approximately 1,117 basis points.

Fifth, daily distribution improves the granularity of cash flow, not the stability of principal. SATA fell from $97.38 on June 22 to $87.75 on June 26, a drop of about 9.9% over four trading days. This single price decline has offset about nine months of stated dividends. Daily distribution can soften the gap at monthly ex-dividend dates and reduce dividend capture trades, but it does not turn a perpetual preferred stock into a money market fund.

Therefore, the most noteworthy aspect of SATA is not "13% daily distribution," but rather that it slices the balance sheet of a BTC treasury company into two layers: common stockholders absorb residual volatility, while preferred stockholders receive prioritized cash flow, while bearing company credit risk, perpetual duration risk, financing channel risk, and BTC valuation risk.

2. Background

2.1 Latest Capital Structure

Strive bought more BTC, but did not increase the dollar value of BTC assets; meanwhile, the preferred stock principal and annual dividend burden are rising rapidly.

From May 12 to the present, BTC count increased by about 4,855, but the price fell by about a quarter, offsetting the quantity increase. The dollar value of BTC holdings changed from about $1.210 billion to about $1.192 billion; SATA stated amount, however, increased from about $496 million to about $783 million. This is precisely why the coverage ratio compressed from 2.44x to 1.52x.

2.2 What Dividends Depend On

SATA's current annual cash dividend burden is approximately: $782.95 million × 13% ≈ $101.8 million/year

Strive's payment of SATA dividends primarily relies on the following sources:

- Proceeds from ATM offerings of SATA or common stock;

- Existing cash reserves;

- Sale or liquidation of other securities;

- Sale of BTC if necessary;

- Future operational income or other financing that may arise.

Therefore, SATA is a cash flow commitment highly sensitive to the continuous openness of capital markets. When the market is willing to absorb new shares at prices close to or above $100, Strive can use the financing to expand BTC reserves and maintain dividends; when SATA trades significantly below $100, the economics of new financing deteriorate markedly.

Taking the current $87.75 as an example, if the company issues one share of SATA near this price, it receives only about $87.75 in gross proceeds but adds $100 to the stated amount and assumes a $13 annual dividend. Simply based on the proceeds, the financing cash cost is approximately: $13 ÷ $87.75 ≈ 14.81%

If the raised funds are primarily used to buy BTC, each new $87.75 in assets corresponds to $100 in preferred stock stated amount, diluting the pure asset coverage ratio. Continued aggressive ATM issuance at this point is only reasonable if management believes BTC's future returns, common stock financing, or market price recovery can compensate for the deteriorating structure.

2.3 Duration of Cash Coverage

Based on $144.5 million in cash and the approximately $101.8 million annual SATA dividend burden, ignoring operational expenses and new issuances, the cash can cover dividends for about 17.0 months.

If we include the STRC holdings, valued at the current market price of approximately $37.66 million, the dividend coverage duration could increase a bit more. But this figure is not "how long the company can survive":

- The company still has employee, listing, audit, legal, and trading expenses;

- Continued issuance of SATA increases the annual dividend burden;

- STRC may depreciate simultaneously with BTC declines and credit tightening;

- Cash is not specifically segregated for SATA holders;

- Management can use funds to continue purchasing BTC or for other corporate purposes.

The cash buffer indeed lowers the probability of forced BTC sales in the short term but does not eliminate financing dependence.

3. What SATA's Daily Distribution Changes

3.1 Actual Daily Amount

The formal declaration for July 2026 is:

- Each business day per share: $0.0493;

- Total of 22 business days;

- Monthly total per share: $1.0846.

Based on the current 7,829,502 shares, if the share count remains unchanged throughout the month, the July cash dividend would be approximately $8.49 million.

3.2 It Does Reduce Dividend Calendar Trading

Traditional monthly or quarterly preferred stocks accumulate accrued dividends before the ex-dividend date and experience a visible price adjustment on that date. Splitting one month's cash into daily business-day payments can:

- Reduce the single ex-dividend amount;

- Decrease dividend capture trades centered on a single ex-dividend date;

- Smooth cash returns more evenly;

- Facilitate holders wishing to frequently reinvest or cover expenses.

This is a genuine product innovation for SATA.

3.3 But Daily Distribution Does Not Eliminate Price Risk

SATA closed at approximately $97.38 on June 22 and at $87.75 on June 26, a decline of about 9.9% over four trading days, a per-share loss of $9.63. Based on the $13 annual dividend, this is equivalent to about 8.9 months of stated dividends.

During the same period, STRC fell from approximately $88.79 to $74.57, a drop of about 16.0%. SATA's relative decline was smaller, suggesting its higher coupon, cleaner balance sheet, and product novelty might still command some premium.

Daily distribution smooths cash flow but does not smooth credit price.

4. How BTC Price Changes Alter the Safety Margin

The following stress test starts from the current snapshot:

- BTC: 19,864;

- Current BTC price: ~$60,005;

- SATA stated amount: ~$782.95 million;

- Cash: $144.5 million;

- STRC holdings at current market price: ~$37.66 million.

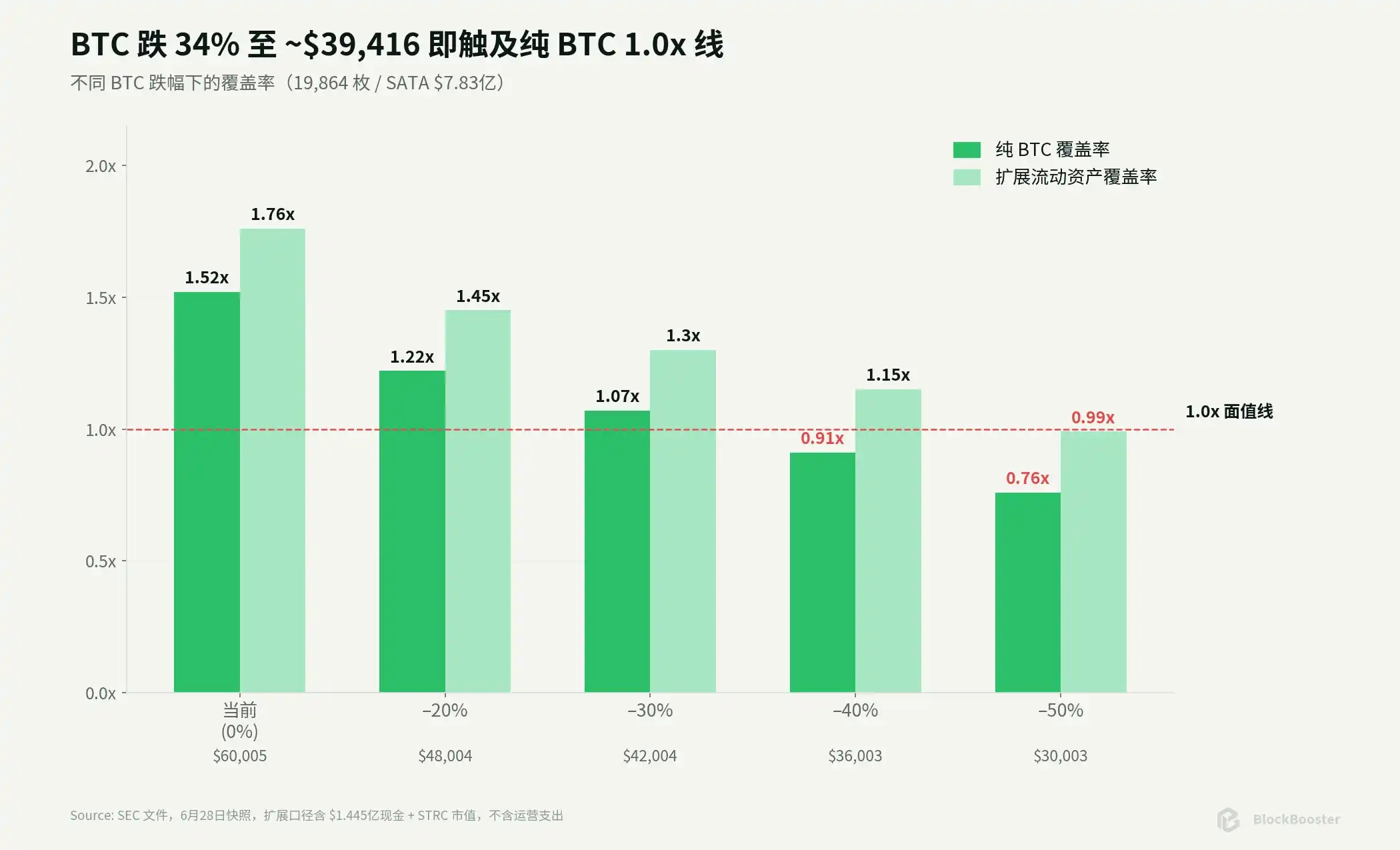

"Pure BTC coverage" only compares BTC value to SATA stated amount; "Extended liquid asset coverage" mechanically adds cash and STRC at current market value. This does not represent legal collateral and does not assume STRC declines in sync with BTC.

*The extended calculation assumes cash and STRC value remain constant, which is overly optimistic in a BTC crash scenario.

The price at which pure BTC coverage falls to 1.0x is approximately:

$782.95 million ÷ 19,864 ≈ $39,416/BTC

Relative to the current ~$60,005, this is a decline of about 34.3%. A 1.52x coverage cannot be considered robust tail protection.

But one cannot simplistically say that SATA will "default" as soon as BTC hits $39,416. SATA is a preferred stock, not a bond with a maturity date; the company still possesses cash, other assets, financing capabilities, and options to adjust capital allocation. What is more likely to happen is:

- SATA's market price falls significantly in advance;

- ATM issuance efficiency declines;

- Management increases the coupon to stabilize the price, ironically increasing the cash burden;

- The company reduces BTC purchases, sells other assets or BTC;

- In extreme cases, it defers dividends.

Credit deterioration is a continuous process, not a mechanical default triggered by crossing a single price line.

5. Key Risks

5.1 Below-Par ATM Reflexivity

When SATA trades above or near $100, issuance can raise funds relatively efficiently; when SATA falls to $87.75, continued issuance exchanges cash below the stated amount for higher preferred stock principal and dividend burden.

A potential negative feedback loop: SATA price falls → financing cost rises → proceeds per share raised decrease → coverage ratio deteriorates → market demands higher yield → SATA price continues to fall.

The company can pause or slow the ATM, thereby stopping mechanical dilution, but at the cost of reduced BTC purchase speed, a weaker capital markets narrative, and increased reliance on existing cash.

5.2 Cash Flow & Financing Channel Risk

Current cash is sufficient to cover about 17 months of static dividends, but this calculation excludes operational costs and future SATA additions. If capital markets close, the company will ultimately have to choose between reducing BTC purchases, selling securities, selling BTC, or deferring dividends.

5.3 Dividend Rate Governance & Cash Cost Stickiness

The board can adjust the coupon rate monthly, but the current low price limits downward adjustment room. The weaker the price, the higher the yield the market demands; the higher the coupon, the greater the company's cash burden. This is an inherent credit reflexivity.

5.4 Preferred Stock Is Not a Bond

Cumulative deferral protects holders, but a dividend suspension is not equivalent to a bond default. Investors may not receive timely cash and may not possess creditors' rights to remedies. In liquidation, creditors and other senior claimants must still be satisfied first.

6. Relative Value

6.1 SATA vs. STRC: Which Is Cheaper?

Current static current yields:

- SATA: ~14.81%;

- STRC: ~15.42%.

This spread must be considered alongside the following factors:

- Strategy is larger, has deeper financing channels, and higher USD reserves;

- But Strategy has approximately $6.7 billion in convertible notes and ~$15.5 billion in nominal preferred stock size, with a more complex capital structure;

- Strive's latest full disclosure shows zero debt, but the company has a short history, is smaller, and has weaker liquidity;

- SATA has a higher coupon and daily distribution, but its coverage is declining rapidly;

- Both have perpetual duration, issuer call rights, and BTC tail risk.

Therefore, one cannot conclude SATA is definitely superior to STRC based solely on "Strive has zero debt," nor can one conclude STRC is a better deal based solely on its higher yield. A 61bp gap is already narrow; the actual choice depends on which risk an investor fears more: complex debt structure or the financing and liquidity risk of a small issuer.

6.2 When Might Relative Value Arise for SATA?

Focus on four types of misalignment:

- Price falls, fundamentals unchanged: If SATA falls while BTC coverage, cash, and ATM conditions do not worsen further, rising yield may create value;

- Coverage continues to worsen, price remains static: If SATA share count grows much faster than BTC, yet the market still trades it near par, risk may be underestimated;

- SATA vs. STRC spread widens abnormally: Need to determine if it's a liquidity shock or a divergence in issuer fundamentals;

- Coupon adjustment diverges from market price: A board decision to increase the coupon may support the price but also increases future cash burden.

7. Conclusion

SATA's innovation is real. It transformed a traditionally monthly/quarterly paying perpetual preferred stock into a listed instrument generating cash flow every business day; it also allows investors in traditional brokerage accounts to access a high-yield security linked to a BTC balance sheet without directly holding the cryptocurrency.

However, price and asset changes in late June corrected several overly optimistic judgments:

- SATA is not a BTC-collateralized bond; it is a corporate-level cumulative perpetual preferred stock;

- Daily distribution did not create low volatility; principal price can erase most of a year's dividends in a few days;

- BTC quantity growth did not prevent coverage from falling from 2.44x to 1.52x;

- ~940bp was the stated spread; the current market spread has widened to ~1,117bp;

- The cash buffer is strong, but the dividend burden and financing cost have risen simultaneously;

- SATA's structural advantages remain, but the market has already repriced it from a "near-par income product" to a "deeply discounted high-risk perpetual credit."

What SATA does is: slice off a layer of tradable, cumulative, perpetual preferred equity from a BTC treasury company's balance sheet and let the market reprice this layer daily.

A mature asset class not only has a spot price but also develops financing rates, seniority tiers, credit spreads, maturities, and default pathways.

However: Cash flow frequency can be engineered, but risk does not disappear; it merely transforms from coin price volatility into coverage ratios, financing costs, perpetual duration, and corporate governance risks.