Author: BiBi News

On May 18, 2026, Situational Awareness LP submitted its 13F filing for the first quarter of 2026.

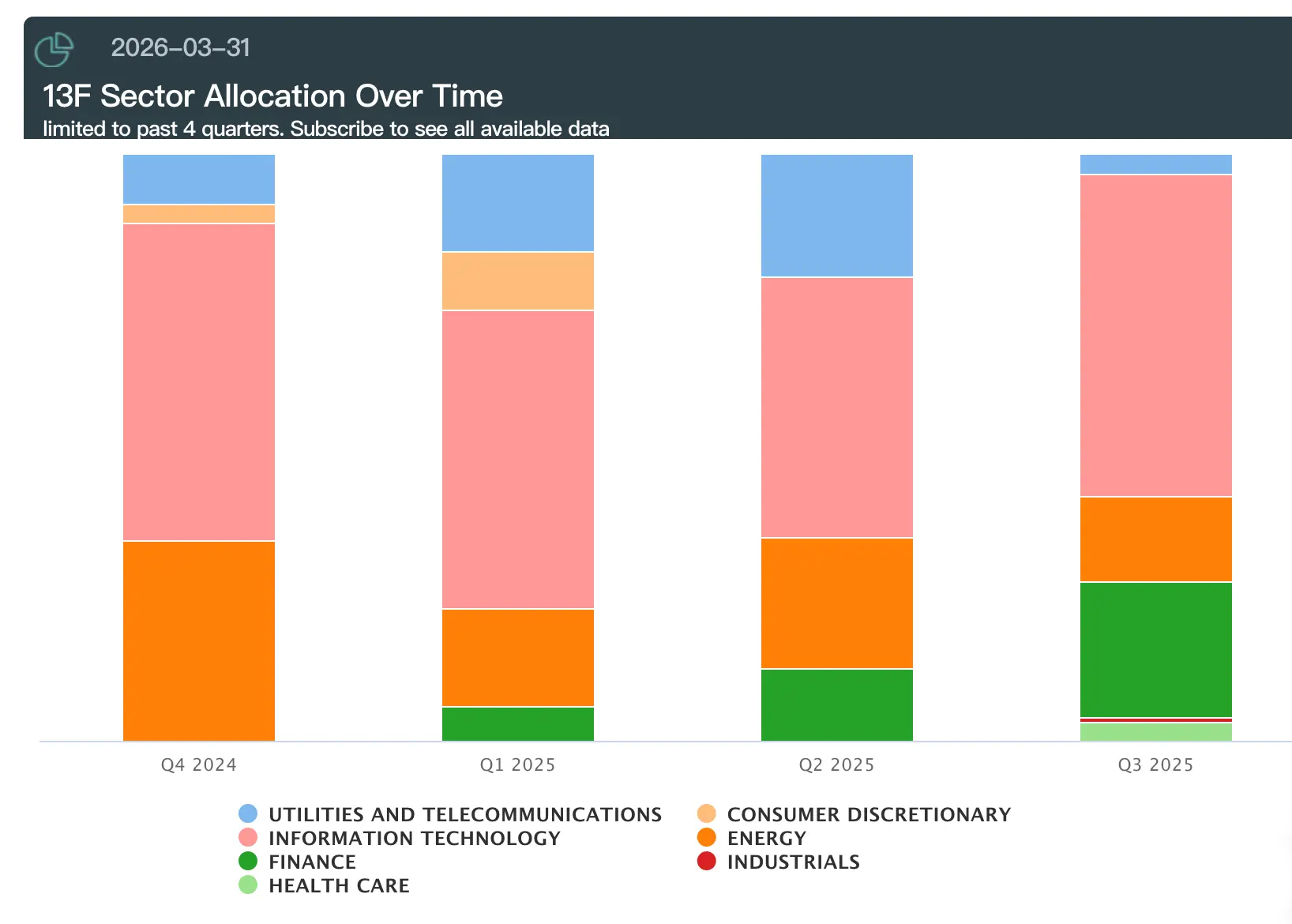

The fund's nominal exposure to U.S. stocks and options expanded from $5.52 billion at the end of 2025 to $13.677 billion, a single-quarter growth of 148%.

However, what caught market attention was not the size, but the structure: over 60% of the new nominal exposure was entirely placed in put options on the semiconductor sector.

What Q1 Did

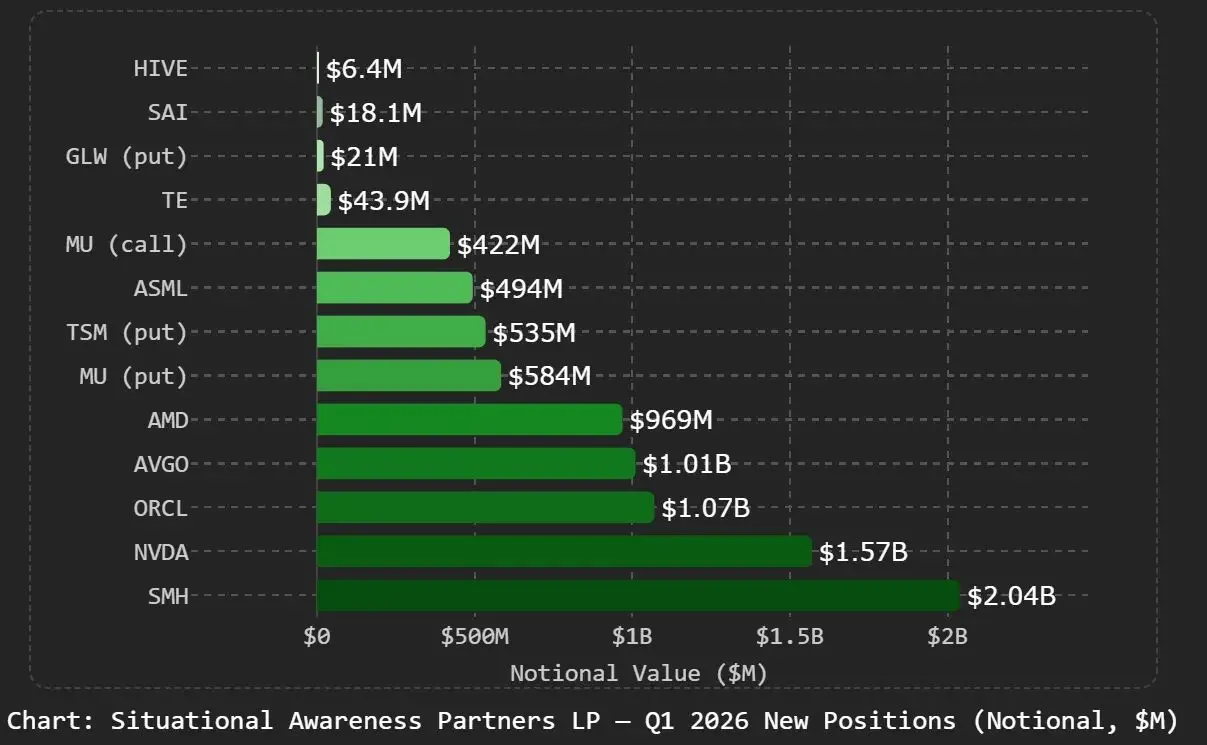

The put options cover nine targets: VanEck Semiconductor ETF (SMH), NVIDIA, Broadcom, Oracle, AMD, Micron, TSMC, ASML, Intel.

Among them, SMH has the largest put nominal size at $2.04 billion, followed by NVIDIA at $1.56 billion. Micron and TSMC hold both call and put options, indicating a bet on volatility rather than a one-sided short.

It should be noted that the 13F filing only discloses the nominal value of options, making it impossible to directly determine the net short size. These put positions could be active shorting or could be hedging protection purchased while holding long positions.

The full intent cannot be reconstructed from the filing alone.

In the stock direction, the fund continued to bet on computing infrastructure.

CoreWeave holdings increased from 6.1 million shares to 7.18 million shares; IREN and Applied Digital were similarly increased;

The expansion was most pronounced in the miner direction: Bitfarms (now renamed Keel Infrastructure) increased from 6.9 million shares to 19.88 million shares, CleanSpark increased from 1.64 million shares to 12.28 million shares, Riot Platforms increased from 6.17 million shares to 11.5 million shares.

Bloom Energy reduced holdings by 3.59 million shares but still holds about $879 million in market value, while retaining 408.5 thousand call options. This is profit-taking, not a change in direction.

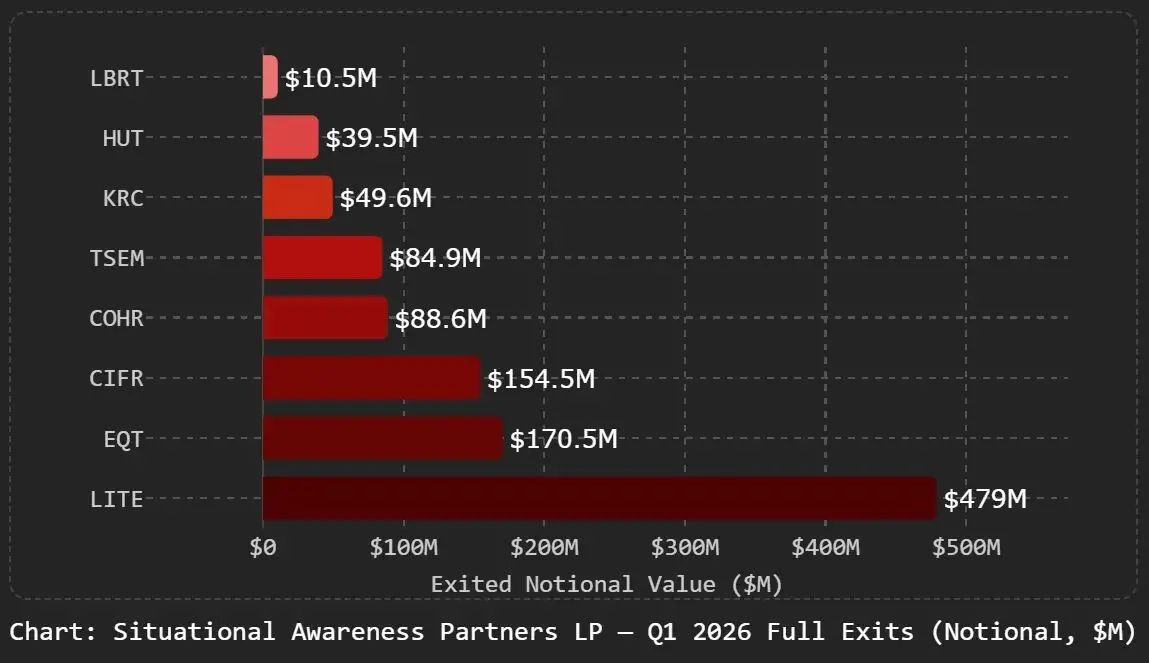

Exits were concentrated in the optical communication direction.

Lumentum and Coherent were completely liquidated; last quarter, Lumentum's position accounted for as much as 8.68%, this quarter it is zero.

Intel's operation deserves separate attention: last quarter held about 20 million call options, all liquidated this quarter, while establishing new put option positions.

Not a flat position, but a complete reversal in direction, from bullish to bearish.

Where the Bottleneck Is, the Money Is

The logic behind this 13F is a specific judgment on supply and demand: the constraints on AI expansion are shifting.

Over the past two years, the core constraint limiting AI scale was GPU shortage, so the market persistently traded NVIDIA, HBM memory, advanced manufacturing, and optical communication. During this phase, the semiconductor sector as a whole received a significant premium.

However, as computing clusters scale towards hundreds of thousands or even millions of GPUs, new constraints are emerging.

Grid connection applications in the US currently have a backlog exceeding 2TW, with an average wait time of over five years; transformer capacity is limited, and new data center construction cycles are measured in years; chips can continue to expand production, but the electricity, land, and construction capabilities needed to support their operation cannot keep pace.

Under this judgment, the logic of shorting the semiconductor sector is not the belief that AI will fail, but that valuations in the chip sector have already priced in expectations, and value is migrating to downstream physical infrastructure.

Buying puts on SMH and NVIDIA hedges against potential valuation corrections in the chip sector; continuing to hold CoreWeave, transformed miner companies, Bloom Energy, is betting on the real bottlenecks: electricity and data center capacity.

CoreWeave's operation also confirms this thinking: call options were slashed from 10.81 million to 1.81 million, while common shares increased from 6.1 million to 7.18 million shares.

The direction hasn't changed, only the high-leverage option positions were swapped for common stock to reduce portfolio volatility impact.

From $225 Million to $13.677 Billion

This fund was founded in September 2024; its first 13F disclosed U.S. stock exposure of about $225 million. By the end of 2025, this number had grown to $5.52 billion; as of March 31, 2026, the nominal exposure reached $13.677 billion.

In the first half of 2025, the fund achieved a return of about 47%, while the S&P 500 rose only about 6%; for the full year, it outperformed the S&P 500 by about 12.5 percentage points.

Before founding the fund, this 24-year-old German published a 165-page paper titled "Situational Awareness: The Decade Ahead," outlining judgments on the AGI timeline and that power and computing infrastructure would become the biggest bottlenecks. The fund's early capital came from Nat Friedman, Daniel Gross, and Stripe co-founders Patrick and John Collison.

The significance of this quarterly report is that it translates a judgment that was previously more narrative into concrete portfolio structure.

Chips are merely the entry point for expansion; what truly determines the speed of AI expansion is whether, in the real world, power can be connected, data centers can be built, and grid connection approvals can be obtained within five years.

If this judgment holds, the keywords for AI investment over the past two years were GPU and models; in the coming years, they may be electricity, land, and construction time.