Editor's Note: Against the backdrop of rising multiple asset classes, the periodic stagnation of BTC and ETH is often simplistically attributed to their 'risk asset attributes'. This article argues that the core of the issue lies not in macro factors, but in the crypto market's own deleveraging phase and market structure.

As deleveraging nears its end and trading activity falls to low levels, existing capital struggles to counter short-term volatility amplified by highly leveraged retail investors, passive funds, and speculative trading. Before new capital inflows and FOMO sentiment return, the market is more sensitive to negative narratives, which is a structural outcome.

Historical analogies suggest this performance is more likely a phase of adjustment within a long-term cycle rather than a failure of fundamentals. This article attempts to move beyond short-term price movements, starting from cycles and structure, to re-understand the current position of BTC and ETH.

The following is the original text:

Bitcoin (BTC) and Ethereum (ETH) have recently significantly underperformed other risk assets.

We believe the main reasons for this phenomenon include: the stage of the trading cycle, market microstructure, and market manipulation by certain exchanges, market makers, or speculative funds.

Market Background

Firstly, the deleveraging-driven decline that began last October has dealt a heavy blow to highly leveraged participants, especially retail traders. A large amount of speculative capital has been washed out, leaving the overall market fragile and risk-averse.

At the same time, AI-related stocks in China, Japan, South Korea, and the US experienced extremely aggressive rallies; the precious metals market also saw a meme-like surge driven by FOMO (Fear Of Missing Out) sentiment. The rise of these assets absorbed a significant amount of retail capital—a point that is particularly crucial, as retail investors in Asia and the US remain the primary trading force in the crypto market.

Another structural issue is that crypto assets have not yet been truly integrated into the traditional financial system. In TradFi, commodities, stocks, and forex can be traded within a single account, with almost no friction for asset allocation shifts; however, in reality, moving funds from TradFi to crypto still faces multiple hurdles—regulatory, operational, and psychological.

Furthermore, the proportion of professional institutional investors in the crypto market remains limited. Most participants are not professional investors, lack independent analytical frameworks, and are easily influenced by speculative capital or exchanges that also act as market makers, thus being led by emotion and narrative. Narratives such as the 'four-year cycle' or 'Santa Claus rally' are repeatedly emphasized, despite lacking rigorous logic or solid data support.

Overly linear thinking is prevalent in the market, for instance, directly attributing BTC's price fluctuations to a single event like the JPY appreciation in July 2024, without deeper analysis. Such narratives are often quickly disseminated and have a direct impact on prices.

Next, we will move away from short-term narratives and analyze this issue from an independent thinking perspective.

Time Dimension is Crucial

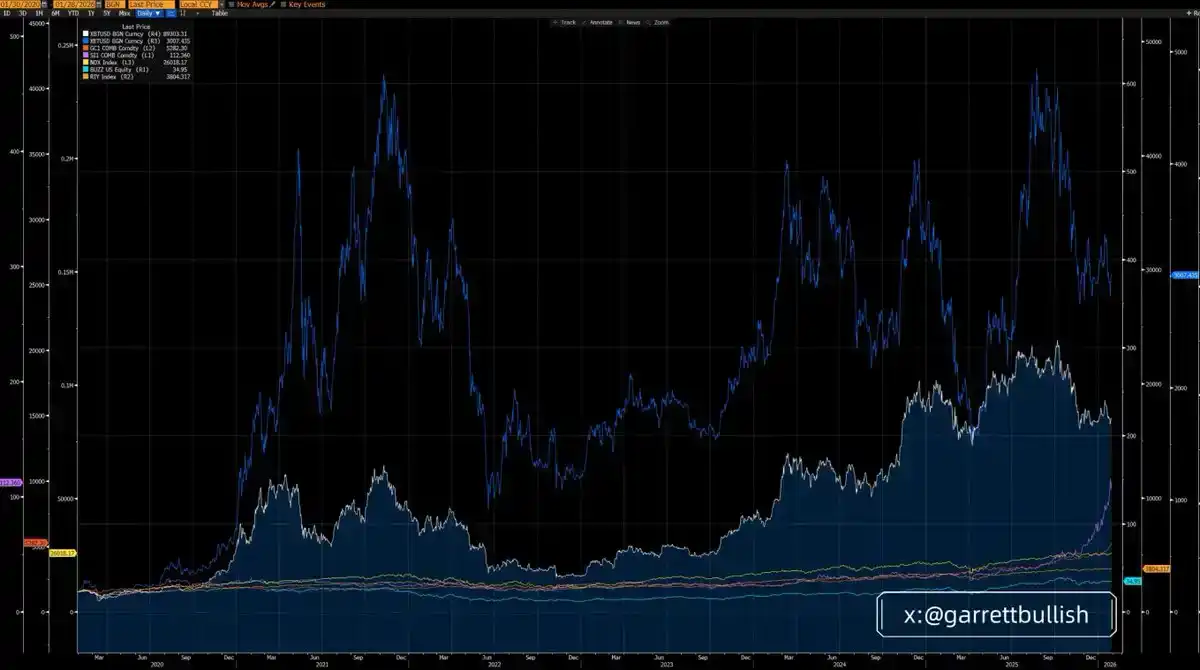

If viewed from a three-year cycle, BTC and ETH have indeed underperformed most major assets, with ETH being the weakest.

However, if extended to a six-year cycle (since March 12, 2020), the performance of BTC and ETH is significantly better than most assets, and ETH actually becomes the top performer.

From a longer time dimension and placed within a macro context, the current so-called 'short-term underperformance' is essentially a process of mean reversion within a longer historical cycle.

Ignoring the underlying logic and focusing only on short-term price fluctuations is one of the most common, and fatal, errors in investment analysis.

Rotation is a Normal Phenomenon

Before the short squeeze in silver prices last October, silver was also one of the worst-performing risk assets; yet now, on a three-year cycle dimension, silver has become the top-performing asset.

This change is highly similar to the current situation of BTC and ETH. Although they are underperforming in the short term, they remain among the most advantageous asset classes on a six-year cycle dimension.

As long as BTC's narrative as 'digital gold' and a store of value is not fundamentally disproven, as long as ETH continues to integrate with the AI wave and exists as core infrastructure in the RWA (Real World Assets) trend, there is no rational basis to believe they will consistently underperform other assets in the long run.

Emphasizing again: ignoring fundamentals and cherry-picking short-term price movements to draw conclusions is a serious analytical error.

Market Structure and Deleveraging

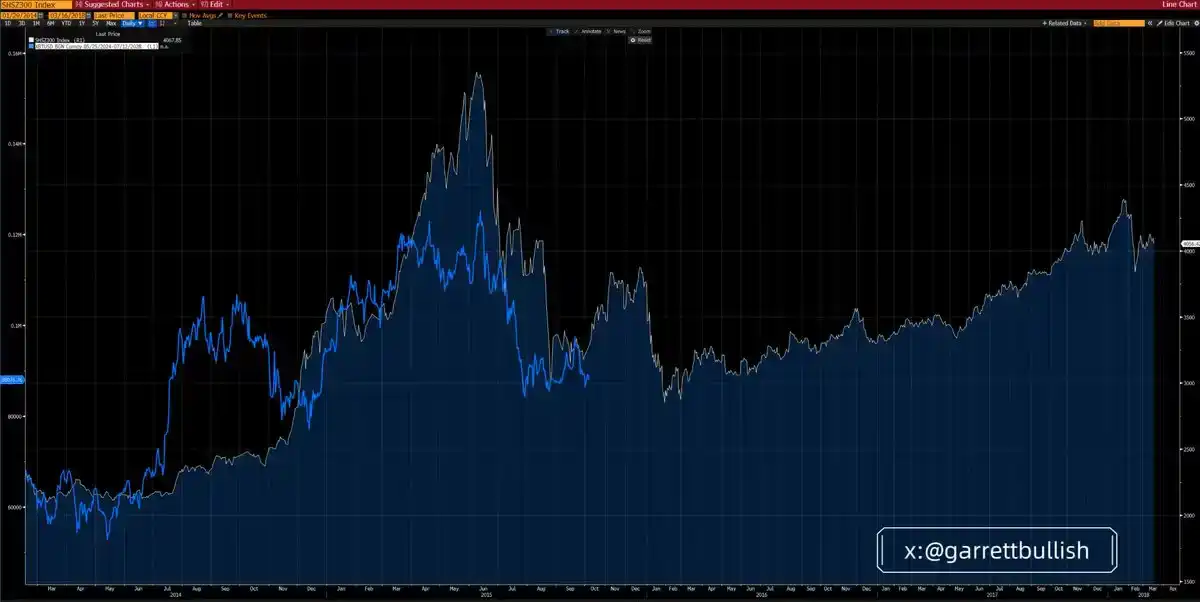

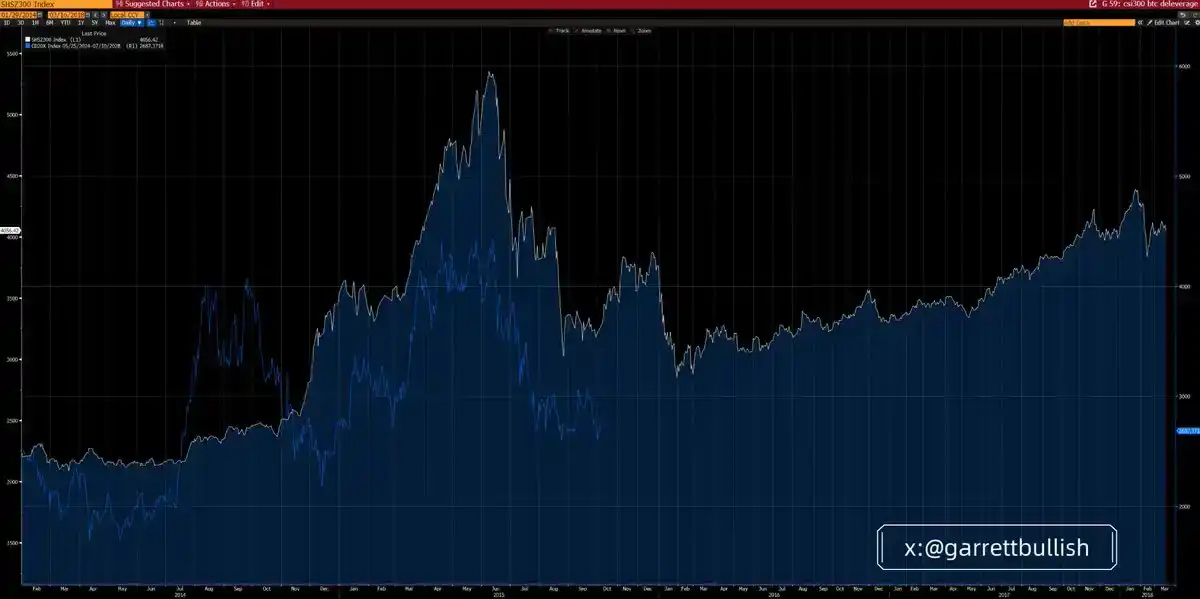

The current crypto market shows a striking similarity to the environment of China's A-share market in 2015 after a leverage-driven rally entered a deleveraging phase.

In June 2015, after a leverage-driven bull market stalled and the valuation bubble burst, the A-share market entered an A–B–C three-wave decline structure conforming to Elliott Wave Theory. After the C-wave bottomed, the market experienced months of sideways consolidation before gradually transitioning into a multi-year bull market.

The core drivers of that long-term bull market came from low valuations of blue-chip assets, improved macro policy environment, and significant monetary easing.

Bitcoin (BTC) and the CD20 index have almost completely replicated this 'leverage up - deleverage' evolution path in the current cycle, showing high consistency in both timing and structural form.

The underlying similarities are very clear: both market environments feature high leverage, extreme volatility, tops driven by valuation bubbles and herd behavior, repeated deleveraging shocks, a long and slow decline process, continuously falling volatility, and futures markets in a long-term contango structure.

In the current market, this contango structure is reflected in the discount of share prices of DAT (Digital Asset Treasury) related listed companies (like MSTR, BMNR) relative to their mNAV (adjusted Net Asset Value).

Meanwhile, the macro environment is gradually improving. Regulatory certainty is increasing, for example, through the ongoing promotion of legislation like the 'Clarity Act'; the US SEC and CFTC are also actively promoting the development of on-chain US equities trading.

Monetary conditions are also easing: rate cut expectations are heating up, quantitative tightening (QT) is nearing its end, repo market liquidity continues to be injected, and expectations of a more dovish stance from the next Fed chair are collectively improving the overall liquidity environment.

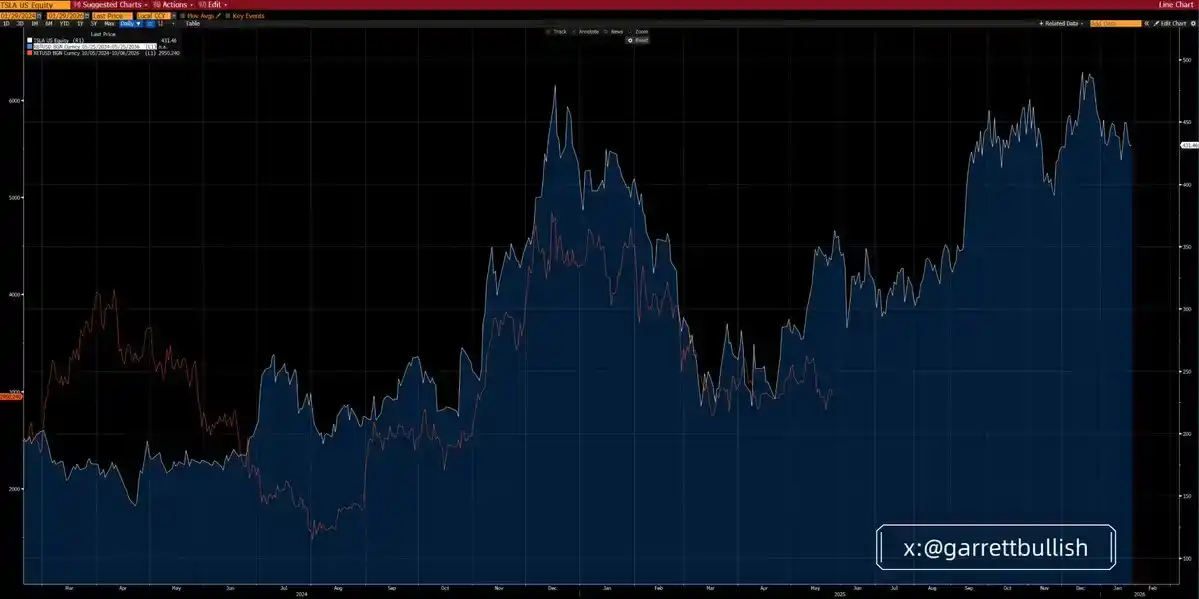

ETH and Tesla: An Informative Analogy

ETH's recent price action is highly similar to Tesla's (TSLA) performance in 2024.

At that time, Tesla's stock price first formed a head and shoulders bottom structure, then rebounded, consolidated sideways, surged again, entered a longer topping phase, fell rapidly, and then experienced a prolonged sideways consolidation at low levels.

It wasn't until May 2025 that Tesla finally broke out upwards, officially starting a new bull market. Its upward momentum came mainly from sales growth in the Chinese market, increased probability of Trump's election, and the commercialization of political networks.

From the current stage, ETH shows high similarity to Tesla at that time, both in technical patterns and fundamental background.

The underlying logic is also comparable: both carry technological narratives and meme attributes, attracted large amounts of highly leveraged capital, experienced violent fluctuations, peaked in valuation bubbles driven by herd behavior, and then entered an adjustment cycle of repeated deleveraging.

Over time, market volatility has gradually decreased, while fundamentals and the macro environment continue to improve.

Looking at futures trading volume, market activity for BTC and ETH has neared historical lows, indicating the deleveraging process is approaching its end.

Are BTC and ETH 'Risk Assets'?

Recently, a rather strange narrative has emerged in the market: simply defining BTC and ETH as 'risk assets' and using this to explain why they haven't followed the rise of US stocks, A-shares, precious metals, or base metals.

By definition, risk assets typically feature high volatility and high beta. From both behavioral finance and quantitative statistical perspectives, US equities, A-shares, base metals, BTC, and ETH all meet this standard and often benefit in 'risk-on' environments.

But BTC and ETH possess additional attributes. Due to the DeFi ecosystem and on-chain settlement mechanisms, they also exhibit safe-haven characteristics similar to precious metals in specific situations, especially when geopolitical pressures rise.

Labeling BTC and ETH simply as 'pure risk assets' and asserting they cannot benefit from macro expansion based on this is essentially a narrative that selectively emphasizes negative factors.

Frequently cited examples include:

Potential EU-US tariff conflicts triggered by the Greenland issue

Canada-US tariff disputes

And potential military conflict between the US and Iran

This line of argument is essentially 'cherry-picking' and applying a double standard.

Theoretically, if these risks were truly systemic, then all risk assets should fall in sync, except perhaps base metals which might benefit from war demand. But the reality is that these risks lack the foundation to escalate into major systemic shocks.

AI and high-tech related demand remains extremely strong and is largely unaffected by geopolitical noise, especially in core economies like China and the US. Therefore, the stock market has not priced these risks substantively.

More importantly, most of these concerns have been downgraded or factually disproven. This leads to a key question: Why are BTC and ETH exceptionally sensitive to negative narratives, yet slow to react to positive developments or the subsidence of negative factors?

The Real Reasons

We believe the reasons lie primarily in the structural problems of the crypto market itself. The current market is at the tail end of a deleveraging cycle, with overall participant sentiment tight and highly sensitive to downside risks.

The crypto market is still dominated by retail investors, with limited participation from professional institutions. ETF flows reflect more passive sentiment following rather than active allocation based on fundamentals and judgment.

Similarly, the accumulation methods of most DATs (Digital Asset Treasuries) are also passive—whether through direct operation or third-party passive fund managers, often using non-aggressive algorithmic trading strategies like VWAP, TWAP, with the core goal of reducing intraday volatility.

This stands in stark contrast to speculative funds, whose main goal is precisely to create intraday volatility—and at this stage, this volatility manifests more on the downside, to manipulate price action.

At the same time, retail traders commonly use 10–20x leverage. This makes exchanges, market makers, or speculative funds more inclined to profit from market microstructure rather than endure medium-to-long-term price fluctuations.

We often observe concentrated selling during periods of thin liquidity, especially when Asian or US investors are asleep, for example, between 00:00–08:00 Asia time. Such fluctuations often trigger chain reactions, including liquidations, margin calls, and passive selling, further amplifying the decline.

In the absence of substantial new capital inflows, or before FOMO sentiment returns, relying solely on existing capital is insufficient to counter the aforementioned types of market behavior.

Definition of Risk Assets

Risk Assets refer to financial instruments with certain risk characteristics, including stocks, commodities, high-yield bonds, real estate, and currencies.

Broadly speaking, risk assets refer to any financial security or investment vehicle not considered 'risk-free'. The common feature of such assets is that their prices are volatile and their value can change significantly over time.

Common types of risk assets include:

Equities / Stocks:

Shares of publicly traded companies, whose prices are affected by market conditions, company performance, and other factors, and can be highly volatile.

Commodities:

Physical assets like crude oil, gold, agricultural products, etc., whose prices are mainly influenced by changes in supply and demand.

High-Yield Bonds:

Bonds that offer higher interest rates due to lower credit ratings, but also come with higher default risk.

Real Estate:

Real property investments, whose value fluctuates with market cycles, economic conditions, and policy changes.

Currencies:

Various currencies in the foreign exchange market, whose prices can fluctuate rapidly due to geopolitical events, macroeconomic data, and policy changes.

Main Characteristics of Risk Assets

Volatility

Risk asset prices fluctuate frequently, which can lead to both gains and losses.

Coexistence of Return and Risk

Generally, the higher the risk of an asset, the higher the potential return, but also the greater the probability of loss.

High Sensitivity to Market Environment

The value of risk assets is influenced by various factors, including interest rate changes, macroeconomic conditions, and investor sentiment.