Original Title: 8 CEOs on Air Force One just ended the American Power Narrative

Original Author: Mustufa Khan

Compiled by: Peggy

Editor's Note: During Trump's visit to China, beyond the leaders' meeting itself, what is more noteworthy is the list of accompanying US corporate executives: Musk, Cook, Huang Renxun, Larry Fink, and heads from Boeing, Goldman Sachs, Blackstone, Citigroup, and other companies were present in the delegation.

Why did these CEOs come? The reason is not complicated. Tesla needs the Chinese market and its Shanghai factory, Apple needs to maintain its Chinese supply chain, Nvidia needs to reopen the Chinese AI chip market, Boeing awaits major Chinese orders, and Wall Street institutions are concerned about licenses, asset management, and capital market access. They belong to different industries but all point to the same reality: for many leading American enterprises, China remains a market, production base, and regulatory gateway that is not easily replaceable.

Therefore, this article truly discusses not the pomp of a diplomatic visit or potential deals, but the structural dependence of American companies on the Chinese market.

The following is the original text:

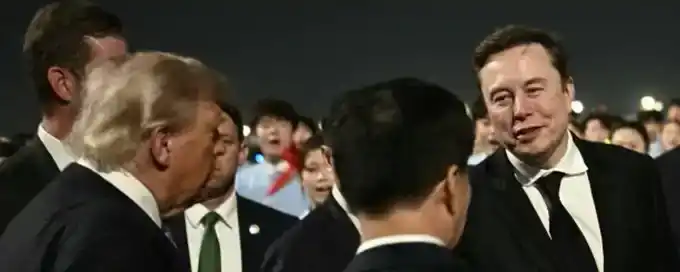

Yesterday, Trump arrived in Beijing, accompanied by Elon Musk, Tim Cook, Huang Renxun, Larry Fink, and several other top US corporate CEOs. The commercial scale behind this delegation is staggering: these entrepreneurs have a combined net worth of approximately $1.07 trillion, exceeding the GDP of the vast majority of economies worldwide, except for a few countries.

The outside world has dubbed this visit a summit.

But judging from the signals released on the ground, it more closely resembles a board meeting of global commercial power: China is the chair presiding over the meeting, Trump is one of the board members, and the accompanying US corporate CEOs are like a business team brought on-site to endorse the final transaction terms.

The core narrative of American power over the past 70 years is being repriced. However, many observers are still focusing on protocol, slogans, and short-term deals, failing to see the underlying structural changes.

The brass band on the tarmac, uniformly dressed Chinese children, and a series of meticulously designed welcome ceremonies can easily be interpreted as standard diplomatic formalities. But what truly matters is not these visuals themselves, but who is setting the pace for this visit.

Nearly every agenda item in the publicly released schedule for this visit was arranged by the Chinese side. This means the agenda's dominance lies with China, while Trump is primarily responding to a predetermined agenda, not actively shaping it. Trump arrives, China hosts. This alone constitutes the most important political and commercial signal of the week.

A country with genuine leverage typically does not publicly disclose what it wants before entering the meeting room; conversely, a country whose leverage is diminishing often compensates for its lack of negotiating chips with a more high-profile public narrative. The American President flies to Beijing, with some of today's most influential US corporate CEOs standing behind him, and before he even lands, press releases have listed every key item on the agenda.

By Friday evening, this visit is likely to yield some concrete results: a few Boeing orders, some quietly progressing chip export licenses, and several agricultural and trade commitments. These will all be packaged as diplomatic victories. But what truly deserves attention this week is not these surface-level achievements, but the very composition of the delegation itself.

Look at who is on this plane and what each needs from Beijing.

Elon Musk: Shanghai Factory Remains Tesla's Lifeline

Tesla's Shanghai Gigafactory began operations in 2019. By 2026, this factory was contributing nearly half of Tesla's global car production, delivering 213,000 vehicles in the first quarter alone from this single site. Musk's investment in the Shanghai production system amounts to tens of billions of dollars, including a multi-billion-dollar Gigafactory and a $200 million Megapack energy storage factory.

The Chinese market contributes roughly a quarter of Tesla's revenue. Over the past two years, Musk has repeatedly warned on X about the risks of authoritarian states and the inevitability of US-China decoupling. But this week, he boarded Air Force One to Beijing, with one core objective being to ensure the continued stable operation of the Shanghai factory.

This is precisely the contradiction Musk must face: one of America's most publicly vocal critics of China is also one of the US CEOs most deeply dependent on Beijing's policy environment. This contradiction is no longer just a matter of posturing in the public arena; it's a reality he must personally handle in Beijing, in front of Xi Jinping and cameras.

Tim Cook: Final China Diplomacy Before the End of His Tenure

Cook will retire on September 1st, succeeded by John Ternus as Apple's CEO. For Cook, this trip to China is likely his last major diplomatic engagement as CEO, and at this moment, he must address one of the hardest parts of the Apple story to fully explain.

For the past five years, Cook has consistently emphasized to Congress, shareholders, and the media that Apple is moving iPhone production out of China. This claim is not without basis. Today, most iPhones sold in the US market are assembled in India. In May 2025 alone, Foxconn invested $1.5 billion into its Indian subsidiary.

Diversification is happening. But the problem lies in the world outside the US market.

The iPhones sold to about 200 other countries and regions still heavily rely on the Chinese assembly system. This means that even as Apple has begun shifting part of its supply chain, its global supply system remains deeply bound to the Chinese manufacturing network.

This week, sitting in a Chinese government building, Cook's real task is not to prove Apple has escaped China, but to ensure this not-yet-relocated supply chain system can continue to operate stably, at least sufficiently to hand this problem over to the next CEO.

Huang Renxun: The Person Trump Personally Called to Get on the Plane

Huang Renxun was originally not on the visiting delegation list. He had planned to skip this trip because his presence might trigger renewed scrutiny within the Republican Party regarding Nvidia's chip sales to China. On Tuesday morning, Trump personally called Huang Renxun, inviting him to join the delegation. Within 24 hours, Huang flew to Alaska and boarded Air Force One.

Trump needed Huang Renxun on-site, primarily due to the H200 chip issue.

Nvidia's H200 AI accelerators were banned for sale to China during the Biden administration, later replaced by the performance-weakened H20. However, the H20 was again restricted in April 2025, leading to a $5.5 billion impairment charge for Nvidia. In late 2025, Trump approved the re-export of H200 to China, with a 25% tariff levied via US Customs. Beijing privately notified customers to suspend purchases.

It has been six months since the White House gave the green light, but not a single H200 has been delivered to Chinese buyers. During this period, Nvidia's market share in China has dropped from 95% to nearly 0%.

Therefore, Huang Renxun's presence in Beijing this week represents one of the most crucial corporate negotiations of the entire visit. He is the only person at the negotiating table who truly understands the chip boundaries: which chips can be sold, which technologies cannot be released, how to maintain revenue from the Chinese market while preventing China from acquiring the computing power foundation to completely overtake Nvidia.

This number cannot be discussed by the Treasury Secretary, nor by Trump. The person who truly understands the technological boundaries and commercial costs is Huang Renxun. In other words, in this negotiation, he is the key party, while the President is more like the person bringing him into the room.

Larry Fink: Managing $11 Trillion in Assets, Yet Still Needing a Chinese License

BlackRock's assets under management (AUM) surpassed $11 trillion in 2024 and have continued to grow since. Larry Fink's business footprint in China has long been at the center of US political controversy.

In 2023, the US House Select Committee on the Chinese Communist Party investigated BlackRock and MSCI, accusing them of directing US investor funds to some Chinese companies blacklisted for alleged military or human rights issues.

Subsequently, BlackRock closed its offshore China equity fund, and its China head, Tang Xiaodong, resigned. Concurrently, several of BlackRock's onshore China funds also suffered losses.

Fink boarded this plane this week because if BlackRock wants to remain the world's largest asset manager by 2035, an onshore China license is almost an unavoidable path. And these licenses are held in Beijing.

The same congressional committee that investigated him three years ago is closely watching this visit. He must secure enough results from Beijing to justify the commercial rationale for staying in the Chinese market, while simultaneously ensuring he is not perceived as having sacrificed US national security interests for market access.

Among all attendees, Fink may have the narrowest needle to thread.

Kelly Otterberg: Boeing CEO Who Has Been Waiting for a Chinese Order for Nearly a Decade

Since Trump's 2017 visit to China, which yielded purchase commitments worth over $37 billion for 300 aircraft, Boeing has not received any truly significant order from China.

The two 737 MAX crashes in 2018 and 2019, the pandemic, the trade war, and Boeing's own prolonged production crisis collectively led to a freeze on Chinese orders for nearly a decade.

Reportedly, the deal on the negotiating table this week may include 500 737 MAX jets and about 100 wide-body aircraft. If finalized, this would become one of the largest single aircraft orders in Boeing's history. Otterberg admitted in a Reuters interview last month that Boeing is relying on the White House to push this order through, and this deal had been somewhat stalled by engine spare parts caught in tariff disputes.

In the first four months of 2026, Boeing secured 284 net orders, its best start to a year since 2014. However, the company's capacity and delivery pace remain under pressure.

A Chinese mega-order might not immediately change Boeing's 2026 performance guidance, but it would be enough to re-energize market valuation of the company's stock and provide Otterberg with the operational validation the board has long awaited. He is on this plane because Boeing has waited for 9 years and cannot return empty-handed again.

David Solomon: Gatekeeper of Goldman Sachs's Wholly-Owned China Business

Goldman Sachs obtained full ownership of its Chinese securities business in 2021, becoming one of the few US financial institutions with a wholly-owned onshore securities business in China.

For Goldman Sachs CEO David Solomon, the core objective of this Beijing trip is to ensure this license continues to hold real commercial value. Over the past three years, China's regulatory environment for foreign financial institutions has continuously tightened, making growth prospects for foreign banks in onshore investment banking, asset management, and wealth management more uncertain.

Onshore investment banking, asset management, and wealth management businesses targeting Chinese clients are important avenues for Goldman Sachs to build long-term revenue sources. If Beijing decides foreign banks are no longer suitable for entering key areas, the strategic path Goldman Sachs has built around the Chinese market over the past 15 years will face reassessment.

What Solomon must do in Beijing this week is ensure that such a reassessment does not happen.

Steve Schwarzman: A Business Statesman Connecting Washington and Beijing for 20 Years

Steve Schwarzman is one of the most senior business-political figures in the delegation. Blackstone's AUM surpassed $1.3 trillion in Q1 2026, becoming the first alternative asset manager to reach this scale.

He founded the Schwarzman Scholars program at Tsinghua University in Beijing, attempting to cultivate bridge-building leaders between the US and China in a manner similar to the Rhodes Scholarship. For many years, Schwarzman has publicly argued that the future of US-China relations is more likely to be one of coexisting "spheres of influence" rather than outright confrontation.

He has spent 20 years cultivating relationships with China's top leadership—a resource most other delegation members do not possess.

Schwarzman's value on this trip lies not in what he can directly obtain from Beijing, but in what he can privately tell Trump: how Xi Jinping will interpret the on-site atmosphere, what concessions are possible, and which conditions will not cause either side to lose face.

In a sense, he is the member of the US delegation closest to a "Kissinger-esque figure." More importantly, he is the only person on this plane who has long treated US-China relations as an investment thesis rather than a quarterly issue.

Jane Fraser: Citigroup CEO Still Waiting for a Chinese License

Citigroup has exited its earlier joint venture arrangements in China and has been waiting for Beijing's approval for its wholly-owned securities brokerage license. However, this application has yet to be granted.

Simultaneously, Citigroup is also involved in a dispute with a Zhejiang-based fuel company. Fraser is accompanying this trip because Citigroup's onshore China strategy is still stuck at the gate, and she needs Chinese regulators to move forward on this long-pending license application.

In the current US-China standoff, Citigroup is among the most squeezed US financial institutions. Mastercard, Visa, and Citigroup are all vying for payments and capital market access, and this access is still controlled by Beijing.

Among the major financial institution CEOs, Fraser likely has the least leverage at the negotiating table, but her needs may be the greatest.

Other Companies on the Plane

The delegation also included executives from Meta, Mastercard, Visa, Micron, Illumina, Cargill, Coherent, and GE Aerospace. They each face different issues, but the underlying logic is highly similar: they all rely, to some extent, on market access, licenses, supply chains, or regulatory resources controlled by Beijing.

Mastercard and Visa want payments access. Micron hopes for lifted restrictions on memory chip exports. Illumina has been placed on the Chinese government's "unreliable entities" list. Cargill needs Chinese soybean orders. GE Aerospace provides engines for Boeing aircraft China may purchase.

These companies are in the delegation because Beijing controls certain key resources they would find difficult to replace within the next five years.

The Common Thread: US Corporate Dependence on China

8 CEOs, corresponding to 8 different forms of dependence on China.

Each of them boarded Air Force One this week because their respective companies have developed, over the past few decades, a structure highly dependent on either the Chinese market or Chinese supply chains. Chinese market access, regulatory licenses, manufacturing systems, order commitments, and policy signals are becoming less of a growth option and more of a strategic necessity for these companies.

And the person holding the keys to these is precisely the one they flew halfway around the world to meet.

Since around 2010, the American corporate class has continually constructed a narrative for itself: that it can seemingly operate above the friction of ordinary political governance. Founders speak directly to users, boards often endorse CEOs' decisions, and regulators are always catching up with already transformed business models.

Many institutions within the US have tried to challenge this narrative, with limited effect.

Over the past 20 years, the Senate has summoned these CEOs time and again but has rarely managed to put them at the same table on the same day. Antitrust investigations often drag on for years, concluding after technology cycles have already shifted. Many Americans watch hearings on YouTube but can hardly name a single piece of legislation from those hearings that truly changed the industry landscape.

But Beijing has accomplished something else: it made these American business leaders fly halfway around the world to sit at the same meeting table, under China's schedule, in China's cities, and within China's protocol system.

This is the part truly worth noting this week. The leverage capable of convening the American power class no longer resides entirely within the American political system. At least for this moment, it exists in Beijing and is being publicly displayed.

By 2026, the most binding force on American corporate behavior may no longer be just Congressional hearings, judicial investigations, or regulatory agencies in Washington, but the market exclusion power held by the Chinese regulatory state.

This leverage is simple and effective: access, or lose access.

After the Summit, the Real Change Won't Be in the Joint Statement

This visit will conclude on Friday. By then, both sides will likely issue a joint statement and announce some concrete results around Boeing orders, agricultural purchases, and some industrial cooperation.

American media may interpret these results as proof of pragmatic engagement; Chinese media will see them as evidence of China's continued central role in the global economy. Neither narrative will be entirely wrong, but both may miss the structural change truly manifesting this week.

What truly matters is that the American corporate class has publicly acknowledged that key decisions affecting their revenue and growth paths for the next decade increasingly occur in a room chaired by Xi Jinping.

The CEOs on Air Force One are the first concentrated display of this model. In the future, any US company still hoping for exposure to the Chinese market will likely have to come to Beijing in a similar manner and accept similar conditions.

The scene on the tarmac is not merely a display of American power. It displays: who has the ability to convene American power and, when needed, make it cross the Pacific to come before them.

While Washington is still explaining why such a power shift cannot happen, the leverage has already quietly moved.

Whether the outside world is willing to admit it or not, the new boardroom is in Beijing.

[Original Link]