Author: Gang Ge

After the last article was published, many people messaged me privately, with questions mainly falling into the following categories:

"Such and such platform seems similar, is it reliable?"

"Is digital currency payment less troublesome?"

"Airwallex makes payment so heavy, is it necessary?"

Figure 1 Jack Zhang's original tweet

This article not only explains why Airwallex chose the "heavy asset" path but also exposes a long-hidden problem in the global payments industry.

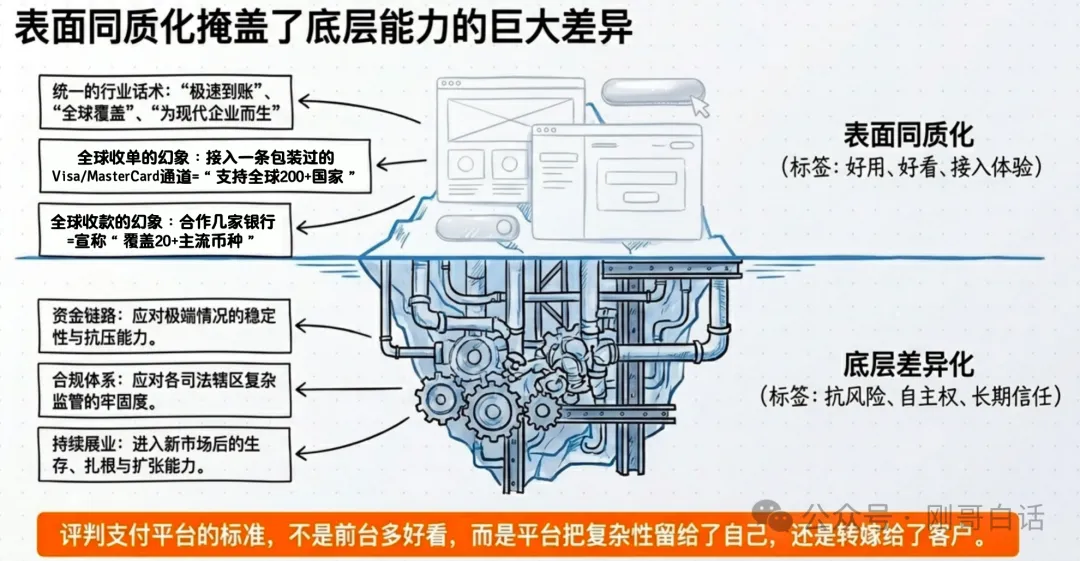

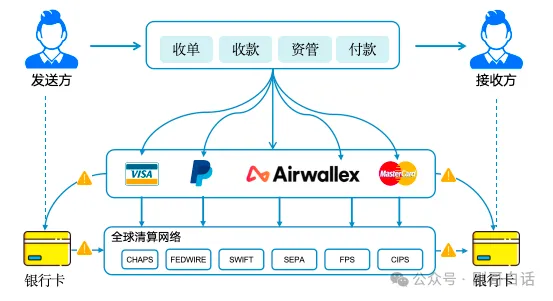

01 Superficial Homogeneity, Core Heterogeneity

When corporate clients choose a payment platform, they are often confused by one problem: the payment companies they talk to all seem to have similar capabilities.

For instance, nearly a hundred global payment companies use a similar script to describe their products: instant settlement, global coverage, serving modern enterprises. Even their features and interfaces are becoming more and more alike.

-

Everyone has global acquiring: By integrating a packaged Visa/MasterCard channel, they can claim to "support 200+ countries and regions";

-

Everyone has global accounts: By partnering with a few banks, they can claim to "collect payments globally with one account, covering 20+ major currencies".

Figure 2 Superficial homogeneity masks vast underlying differences

Users also can't see the real differences between platforms in product descriptions, which is why they scrutinize payment institutions over and over regarding costs, background, licenses, and risks.

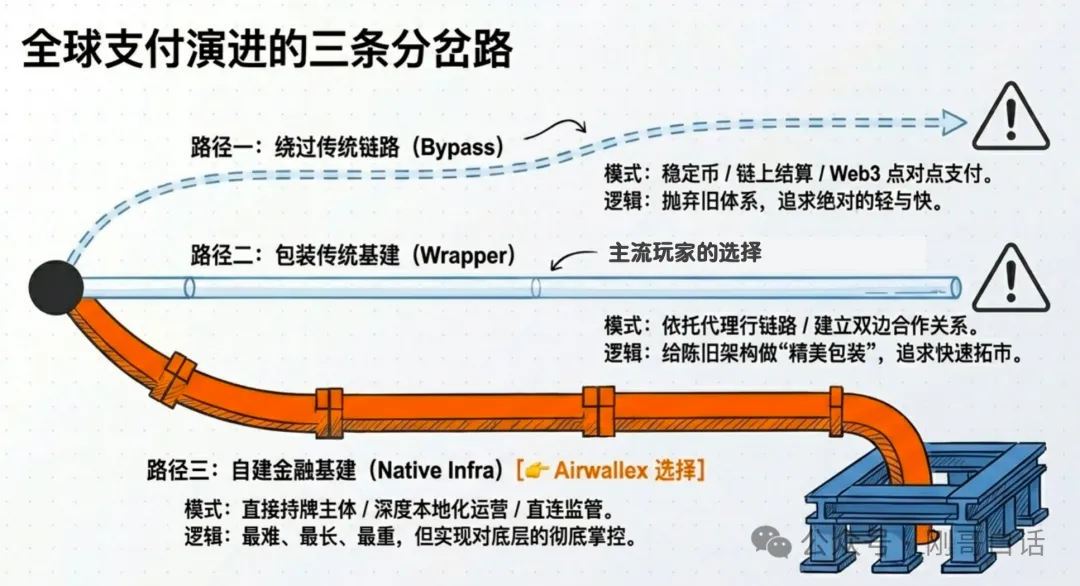

02 Three Paths in Global Payments

Since the front-end can't reveal core capabilities, we must return to the underlying layer and clarify the common paths in this industry.

Breaking down the mainstream players in the industry, there are roughly three paths.

Figure 3 Three divergent paths in the evolution of global payments

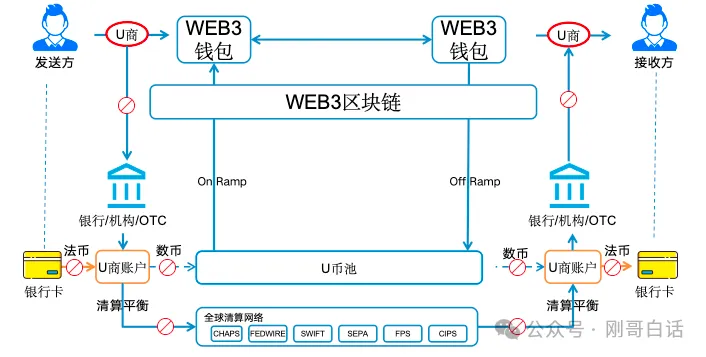

2.1 First Path: Bypassing Traditional Channels

First path: Web3 Digital Currency Payments

This path generally tells the same story: stablecoins, on-chain settlement, programmable payments, peer-to-peer payments. Compared to traditional payments, it promises a shorter path, faster speed, lower cost; and it hopes to penetrate the consumer retail scene with a low-value, high-frequency narrative.

However, you will find that very few digital currency payment players on this path have survived.

Figure 4 First Path: On-chain settlement bypasses traditional channels

-

Technology: Global payments settle in seconds; merchant settlement to card D1/D0 available;

-

Service: Highly competitive payment costs, mature local operations teams serving clients' last mile;

-

Compliance: Regulatory concerns persist across jurisdictions, leading to significant friction;

-

Product: Mainstream platforms also focus on stablecoin payments; once regulations are clear, they can readily integrate and substitute.

This is why many entrepreneurs with Web3 payment dreams ultimately have to bow out.

2.2 Second Path: Wrapping Traditional Infrastructure

This is the most traveled path in the industry: relying on partners, intermediaries, to wrap a layer of packaging around the complex and antiquated underlying architecture, then using better product experience and faster marketing to drive market expansion.

The advantages of this path are also obvious: quick results, fast business development, rapid coverage expansion, making it the natural choice for most players.

But the problem is, it mostly optimizes the front-end rather than rewriting the underlying layer.

Figure 5 Second Path: Aggregated gateways wrap infrastructure

Actually, Stripe, with the fastest-growing global market value, tried to acquire Airwallex in 2019 (rejected), and in 2026, there were rumors of acquiring PayPal (also reportedly rejected).

This at least indicates one thing: even the international payment giants that grew rapidly through "tech + light asset connectivity" eventually have to go back and learn the lesson of building infrastructure.

Often, the seemingly lighter path doesn't avoid infrastructure; it just postpones it.

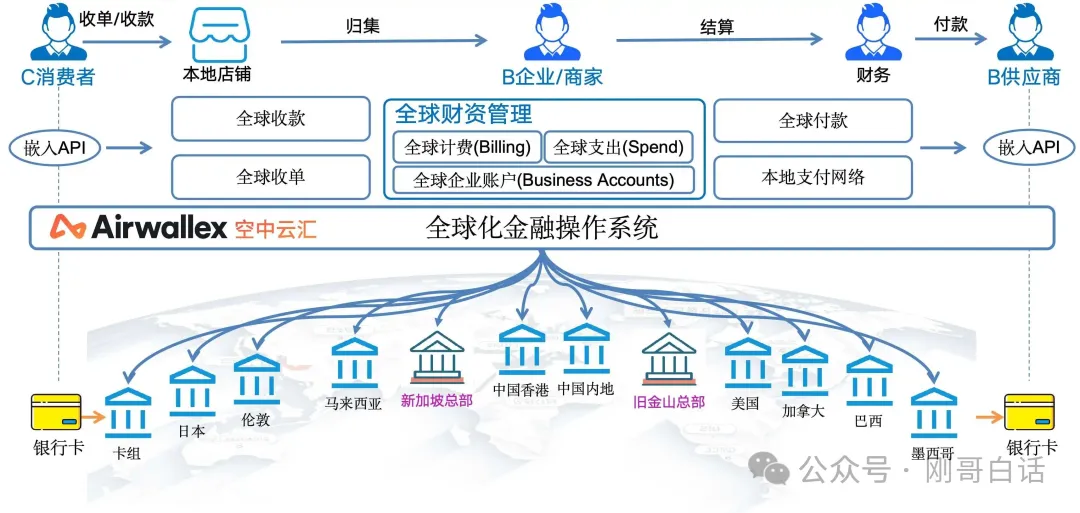

2.3 Third Path: Self-building Global Financial Infrastructure

This path is the most difficult because it offers almost no shortcuts. It requires sustained high investment, longer cycles, and also implies heavier responsibility.

Figure 6 Third Path: Self-building global infrastructure

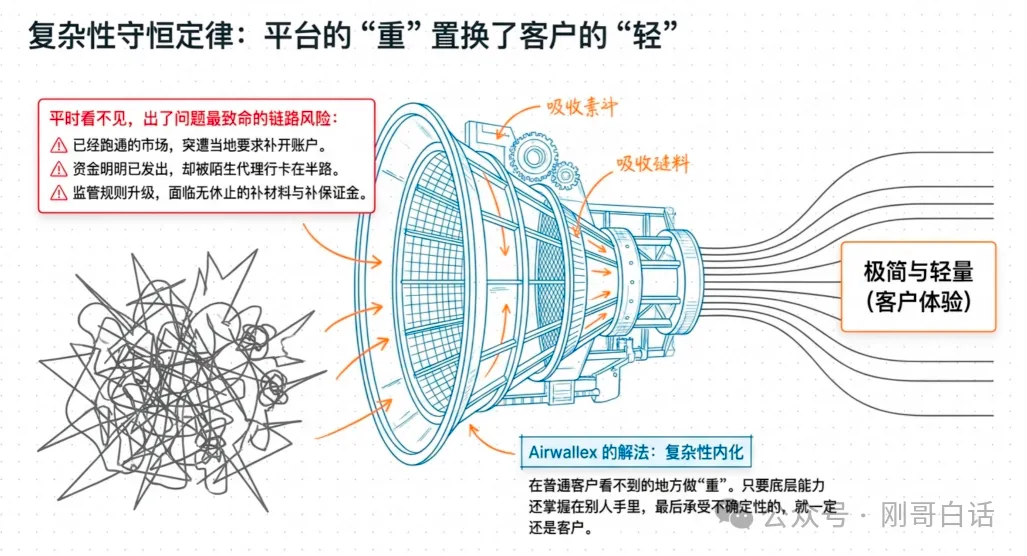

03 Platform's "Heaviness" in Exchange for Client's "Lightness"

For example, a market that was already running smoothly might suddenly have its accounts frozen by banks; a client who already paid for goods might have the funds stuck halfway by a correspondent bank, unable to arrive for a long time; regulatory rule upgrades might require submitting additional documents, collateral, or processes.

These problems may not occur daily, but just one occurrence is enough to disrupt a company's rhythm.

Figure 7 Platform's "heaviness" exchanged for client's "lightness"

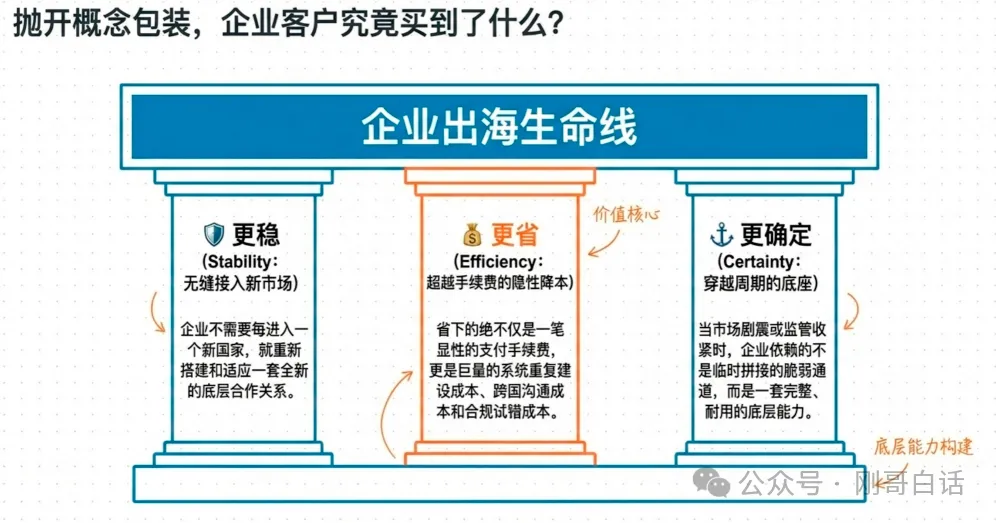

04 What Clients Truly Gain

Figure 8 The value corporate clients truly need

-

More stable, because enterprises don't need to adapt to a new set of partnerships every time they enter a market.

-

More cost-effective, not just saving on processing fees, but also eliminating massive duplicated system costs, communication costs, and compliance costs.

-

More certain, because when market conditions change or regulatory rules tighten, clients rely not on a temporarily patched-together channel, but on a more complete, durable, and cycle-transcending underlying capability.

This is also why Airwallex's growth logic is more like compound interest than explosive growth.

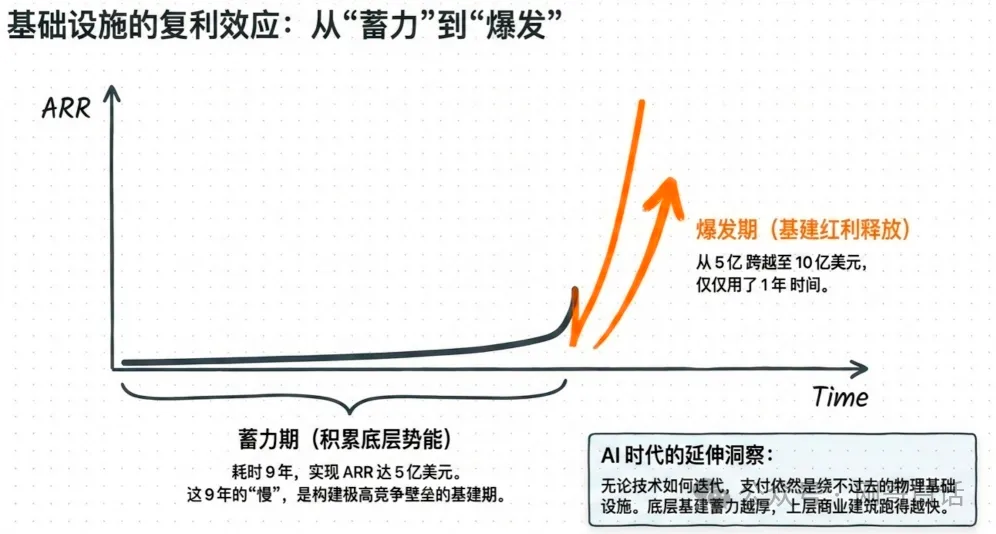

Figure 9 Compound growth brought by infrastructure investment

According to public information, Airwallex took 9 years to achieve $500 million in annualized revenue (ARR), but only one year to grow from $500 million to $1 billion. The initial "slowness" wasn't inefficiency but rather accumulating underlying potential for later acceleration.

05 Final Words

Returning to the initial question, why does Airwallex build its own global financial infrastructure?

Figure 10 Underlying capability is the true watershed

For corporate clients, choosing a global payment platform is essentially choosing a long-term partner, a foundation that can help digest complexity and allow you to operate your business more stably.

[References]

[1] Airwallex Official Article: The Path of Maximal Resistance

https://www.airwallex.com/cn/blog/the-path-of-max-resistance-the-spectrum-of-global-payments-infrastructure

[2] Airwallex Official Article: The Last Mile of Global Payments

https://www.airwallex.com/cn/blog/the-last-mile-of-global-payments

[3] Sina: Reshaping the Future of Finance

https://finance.sina.com.cn/cj/2025-10-11/doc-inftnpwr8889861.shtml