By | TingtongTech (ID:tingtongtech), Author | Ke Chen, Editor | Xiafei Rao

No sooner had the "century lawsuit" between Elon Musk and Sam Altman concluded than their rivalry swiftly shifted to Wall Street.

On May 21, U.S. Pacific Time, SpaceX officially filed its S-1 IPO prospectus with the U.S. Securities and Exchange Commission, planning to list on NASDAQ under the ticker "SPCX" with a target valuation of $1.75 trillion to $2 trillion and a fundraising cap of $75 billion.

On the very same day, OpenAI was reportedly working with Goldman Sachs and Morgan Stanley to draft its IPO prospectus, potentially filing confidentially as early as May 22, aiming for an IPO as soon as September this year.

Former entrepreneurial partners, now courtroom and market adversaries, sent out their invitations to the capital market in the same week. But this is not a heartwarming tale of "former brothers joining forces to reach the shore." This is a head-to-head, cutthroat Wall Street battle.

In this drama, Musk is selling a "space AI" story. Altman narrates a script of transformation from a "non-profit charity" to an entity gripped by a thirst for profit.

For the audience outside the drama, the greater interest lies in who tells the better story in this IPO scramble, whose data looks more impressive, and who is the one most desperate to stay afloat by going public.

More importantly, are these tech giants spinning tales, or are they creating value? What kind of market will be left for investors and the industry after these two giants vie for a position on Wall Street?

-01- SpaceX: When There's No Profit, Stuff 'Dreams' into the Prospectus

This time, Musk is laying out a set of financial cards that are deeply contradictory.

Musk's target is grand. SpaceX plans to raise $75 billion with a valuation of $1.75 trillion to $2 trillion, with a target listing date around June 12. If achieved, SpaceX would be the largest IPO in human history, and Musk would become the world's first trillionaire.

However, key data revealed in the prospectus shows that in 2025, SpaceX had a net loss of $4.94 billion. The loss for Q1 2026 was even more staggering, nearing the annual 2025 figure at $4.28 billion, making a $2 trillion valuation seem far-fetched.

Breaking it down, SpaceX's business segments are "strikingly uneven in prosperity."

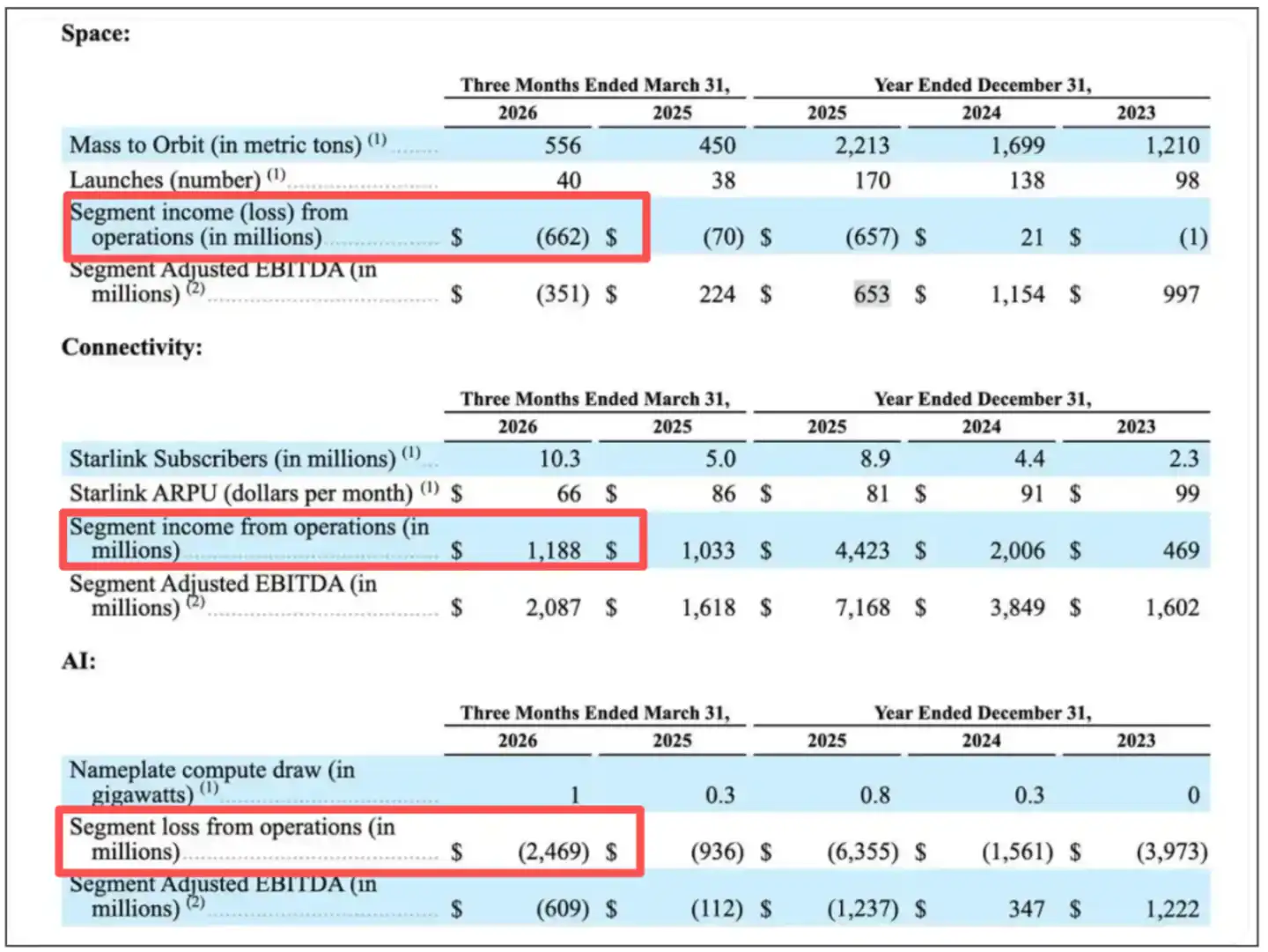

Figure: SpaceX's Three Major Business Segments Revenue and Profit

Source: SpaceX Prospectus

Among the three major segments — Aerospace, Connectivity/Starlink, and AI — the Connectivity business housing Starlink is the only one presentable. In Q1 2026, it generated $3.26 billion in revenue and $1.19 billion in operating profit, accounting for 69% of total revenue. A quarterly profit of $1.19 billion is an exceptionally strong number by any standard.

But the question is, where does Starlink's money go? The answer lies in the other two segments.

SpaceX's Aerospace business (rocket launches and the Starship project) had Q1 revenue of $619 million but lost $662 million. Data suggests SpaceX has already burned over $15 billion developing Starship.

However, what truly obliterates the profits is the AI business. After acquiring Musk's own AI startup, xAI, and integrating it into the "SpaceX AI" segment, it recorded a loss of $6.355 billion for the full year 2025 and another $2.469 billion in Q1 2026.

In other words, the hard-earned net profit from Starlink is not only entirely consumed by the other two segments but also ends up putting the company tens of billions of dollars further in the red.

From Musk's script, this is a beautiful plan: the earth-based "Starlink" makes money to fund the space-based "Space AI" and "Mars." This is likely why, before the IPO, Musk merged xAI into SpaceX.

From the market's perspective, SpaceX's IPO at this time essentially tests a proposition: can one "Starlink" actually support one "Mars" and one "Space AI"?

In other words, the $2 trillion valuation can be understood as Starlink contributing roughly $0.5 trillion, xAI's AI story contributing about $0.5 trillion, and the remaining $1 trillion is essentially a long-dated option on "space AI infrastructure."

Investors tolerated losses from Musk's "Starlink" because they believed that xAI's current black hole would transform into a second money-printing machine. According to SpaceX, the potential market size for AI-related ventures could reach $26.5 trillion around 2030. If this story holds, current losses aren't a problem.

More importantly, the money Musk is pouring into "space" comes with plenty of stories yet to be told.

Take the core orbital AI data center as an example. It is reported that SpaceX has applied to the FCC to deploy up to 1 million satellites, building a "satellite constellation with unprecedented computing power" in low Earth orbit to power advanced AI models.

SpaceX wrote in its prospectus, "We believe we are the only company with a commercially viable path to building orbital AI computing capabilities at scale," with plans to begin deployment as early as 2028.

Another foundational tool is Starship.

SpaceX has cumulatively invested over $15 billion in Starship R&D, with about $3 billion spent in 2025 alone. Starship is the transportation infrastructure for space AI infrastructure, moon landings, Mars colonization — everything. Without it, a space data center is just a castle in the sky.

Further down the line, there are even longer-term blueprints like lunar manufacturing infrastructure and Mars colonization.

Clearly, SpaceX's valuation incorporates a huge premium for investor expectations regarding the space economy, AI, and Musk himself.

Previously, commentators pointed out that what truly elevates SpaceX's valuation might not be any financial model, but investors' fear of missing out on the next Tesla.

Many analysts note that no matter how explosive SpaceX's data is, some analysts and investors will be willing to buy into it, essentially due to the credibility built by Tesla's stock surging over 2,700% in the past decade. The market's fear of "missing the next Tesla" is driving analysts to collectively abandon rationality.

Regardless, SpaceX's filing at this moment indicates Musk is ready to package a bundle of cash-burning dreams, massive losses, and his 85.1% control stake, and sell it to the world for $2 trillion.

-02-OpenAI: From 'Benefiting Humanity' to 'IPO for Cash Infusion'

If Musk's IPO is a valuation gamble, then Altman's IPO is a "life-saving cash infusion that cannot be avoided."

In comparison, although OpenAI's story is much more down-to-earth, the burn rate for large models and APIs is described as "rocketing."

On May 21, multiple media outlets reported that banks including Goldman Sachs and Morgan Stanley were assisting OpenAI in drafting its IPO prospectus. The company plans to confidentially file with regulators soon, possibly within days.

Some insiders also stated that OpenAI aims to launch its IPO as early as September, though the plans remain fluid and subject to change.

This means the AI behemoth, once valued at over $850 billion, is about to open its doors to the public market. Furthermore, many industry insiders believe Altman likely hopes to beat Musk to the punch.

After all, Altman has just settled Musk's lawsuit over "abandoning the public benefit mission." With this major stumbling block removed, OpenAI is fast-tracking its IPO schedule.

However, from the market's perspective, while OpenAI's move appears superficially as a "beachhead landing," its core resembles a "cash infusion and escape."

Peeling back the surface of an $850 billion valuation, OpenAI's substance isn't glamorous.

First, OpenAI needs money to survive. Public data shows OpenAI has about 960 million monthly active users and annualized revenue of around $25 billion — seemingly impressive. But it burns $57 billion a year, resulting in a net loss of $44 billion.

Additionally, OpenAI's monetization efficiency per user is problematic. For instance, competitor Anthropic generates $211 per monthly active user, while OpenAI only makes $25.

Previously, Altman has hinted on various occasions that annual computing power investment is astronomical. Without an IPO for a transfusion, although there's plenty of money in the private market, it will eventually run out. Leveraging the public market essentially means seeking fundraising from global retail investors.

Especially since OpenAI's so-called legal victory didn't actually secure a turning point for itself.

Many see Musk's loss in court as a key turning point for OpenAI's IPO. However, although the lawsuit was won, Musk's soul-searching questions haven't disappeared. A company born with a "non-profit" slogan yet eager to distribute profits wildly to shareholders (including Microsoft) is inherently contradictory in its governance structure.

Many analysts believe that choosing this timing for the IPO, Altman wants to strike while the iron is hot — while the舆论heat from "defeating Musk" is still present and before the口碑of GPT-5.5 cools completely — to quickly harvest the capital market.

Of course, a market commonplace is that OpenAI was once unique but is now being "besieged." Whether it's Anthropic eroding OpenAI's core user base at an astonishing speed or Google catching up step by step, it all indicates Altman must accelerate to take the market lead.

In particular, while ChatGPT is famous, in the enterprise market, Anthropic's Claude enjoys an excellent reputation. Reports indicate Anthropic's annualized revenue exceeds $30 billion, and its latest valuation is about to surpass $900 billion, a figure that has already overtaken OpenAI.

In this situation, if OpenAI doesn't go public soon, it will miss its chance. Once market attention is drawn away by an Anthropic IPO, or if the next "Strawberry" or "Orion" model fails to ignite the market as expected, OpenAI's valuation myth could shatter at any moment.

-03-Spinning Tales or Creating Value?

To make matters worse, Anthropic, also racing to go public alongside Musk and Altman, was recently reported to be nearing profitability.

According to the latest media reports, Anthropic's revenue in Q2 this year is expected to more than double, reaching $10.9 billion, which would help the company achieve profitability for the first time.

This is not good news for either Musk or Altman, as there's still no answer as to when SpaceX and OpenAI will become profitable.

(Image sourced from the internet)

All this will undoubtedly accelerate industry involution. For both SpaceX and OpenAI, the immediate question is who will secure the IPO lead and obtain the "golden parachute."

For Musk, once SpaceX goes public, there will be two Musk concept stocks in the market. Tesla's story is about electric vehicle penetration and autonomous driving realization — narratives that have been repeatedly validated. SpaceX's story is about Starlink, space computing power, and Mars colonization — stories with longer realization cycles and imaginations less constrained.

For Altman, pushing OpenAI public allows his stock options and equity to be realized, transforming him from an "AI evangelist" into a "Silicon Valley magnate."

However, even as these two star companies may face their capital market coming-of-age, they still need to prove whether their trillion-dollar valuations are justified or bubbles.

The reality is, the market cares more about whether these companies are spinning tales or creating value.

As is well known, SpaceX's valuation is built on "long-term imagination." The problem is that this time, the "pie Musk is drawing" is excessively large.

Whether Musk's optimistic expectations materialize depends on whether Starship can launch on schedule, whether AI can find a commercial path in orbit, and whether space data centers can evolve from PPT slides to actual servers.

Even the prospectus admits these plans are "still in early stages, involve significant technological uncertainties, and may not achieve commercial viability." Market analysis also points out that SpaceX's price-to-sales ratio would be around 80x, far above the average of about 7x for the top 15 U.S. companies by market cap.

OpenAI's trillion-dollar valuation is built on the assumption that "large models will become the next-generation operating system."

Judging from current product forms, ChatGPT remains a conversational AI tool, and its business model hasn't broken free from the "pay-per-Token" framework.

OpenAI has also attempted emergency adjustments to mask its internal and external troubles, shutting down the cash-burning, barely-monetized Sora video project, and even rumored to be considering developing its own smartphone.

But investors aren't buying it. According to The Information, several underwriters have conducted soundings with public market investors, receiving rather lukewarm feedback. Major concerns include excessively high valuation, with a forward price-to-sales ratio of about 28x (based on projected 2026 revenue) far exceeding Nvidia's roughly 12x metric.

The above market reactions indicate these are not traditional IPOs but more like two capital scrambles.

Ultimately, the reason lies in the fact that neither SpaceX nor OpenAI are traditional companies.

SpaceX's dream is to build a Martian city; OpenAI aims to achieve AGI. Within Wall Street's narrative logic, this kind of grand, out-of-the-ordinary vision might be the only way to make investors accept astronomical valuations.

But the fact is, in SpaceX's prospectus, Musk holds 85% of the voting power, employing a dual-class share structure. This means that as long as he insists on the Mars colonization dream, the company must follow, regardless of investor opinion.

And OpenAI's various narratives consistently teach investors one thing: "Please believe we will improve; we're just facing some difficulties now."

In other words, both IPOs share a commonality: they aren't using beautiful profit curves to convince investors but are asking investors to pay for faith in a future "promise."

Of course, for the market, the only certainty in this capital game is that, whether for SpaceX or OpenAI, a successful listing will become one of the largest IPOs in history, bringing massive underwriting fees to Wall Street and astronomical personal wealth to the founders.

Simultaneously, retail investors may have to pay a considerable price to fill the enormous financial loss black hole.

And this is precisely the awkwardness of the capital market. If post-IPO stock performance disappoints, investors may conclude these companies were overvalued.

This inevitably recalls the 2021 tech stock frenzy. Back then, any company associated with cloud or SaaS enjoyed sky-high valuations, only to experience brutal corrections during the interest rate hike cycle. Many analysts believe, "To invest in these stocks, you need a strong heart."

Conversely, for these two super IPOs, investors need to think clearly: Are they willing to pay a higher premium for Mars colonization and orbital data centers? And are they willing to wait for years for the AGI vision?

After all, what lies between a bubble and a vision is not just repeated quarterly earnings misses, but a genuine capital valuation scramble for survival.

And Wall Street needs to prepare, because following these two will be even more stories.

(Header image and some supporting images are from AI.)

(Disclaimer: This article is for informational exchange only and does not constitute any investment advice.)