Author: Yuanchuan Investment Review

When an investment chat group grows quiet, tossing in a chart of Wu Yuefeng's net worth curve can instantly liven up the atmosphere.

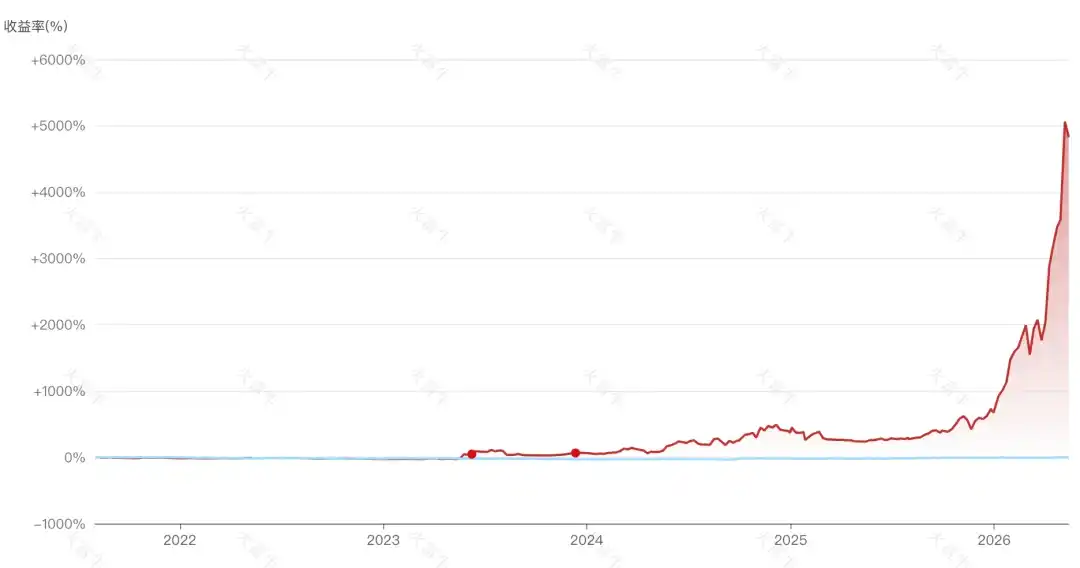

This time, the net asset value (NAV) of Jia Yue Yuefeng Investment's Genesis Fund has not only resurfaced but also hit a new all-time high. Last year, Wu Yuefeng managed to bring the NAV back above water from below 0.3, thinking he had climbed out of the abyss, only for it to soon fall back below 0.5. It wasn't until May 8th this year, with the NAV surging nearly 167.54% in the past month, that Wu Yuefeng made his comeback.

Judging from the fund's portfolio report, the total equity position is maxed out at 100%, with 35% in AI computing infrastructure and 20% in memory chips, constituting the main drivers behind the NAV surge. A/H share optical modules and PCBs make up 5%. Wu Yuefeng has almost entirely bet on the AI computing industry chain [1].

Over the past year, just a slight shift in mindset to chase optical communication and memory stocks, rather than defending in baijiu, could fill any hole, no matter how deep or poorly dug earlier. Standing in the light, staying close to the chips, has been the biggest wealth code this year.

Yuanlesheng, Shiva, Qushi—subjective strategy funds that were infinitely glorious from 2020-2021—have seen their representative products' NAVs skyrocket over the past year, breaking through historical highs. Mr. Fu at Ruijing has quietly doubled his fund's NAV in the past year, setting a new record. A private fund named Zhun Jin Zhi Zhan No.1 is even more exaggerated, multiplying fivefold this year and fiftyfold in under five years since inception.

What is a Thunderous NAV

Then there are rumors of Yao Jinghe's private fund making astronomical profits from memory and CPO (Co-Packaged Optics), the former OpenAI employee Leopold whose hedge fund grew from $225 million to $5.5 billion in a year, and the Hefei state-owned capital, poised to be crowned "the most legendary VC" again with Changxin's impending IPO. It seems everywhere you look, people are counting money standing on "Chips, Light, and Lithium," while those without can only watch the relentless rise, gazing at various thunderous NAVs until their prefrontal cortexes are damaged by anxiety.

At this moment, those standing in Hang Seng Tech and value stocks can't help but wonder: Even Shanghai KTV hostesses have made 18 million, why hasn't the market rotated from high-flyers to laggards?

Silicon Bull, Carbon Bear

This market cycle has a peculiar aspect: no matter how crowded the AI industry chain gets, it just won't fall.

In Q1 this year, active equity funds allocated 31.5% to AI hardware, with an overweight position of 17.7%. Compared to historical core sectors, while not surpassing the peak of the "Mao Index" era, it has already exceeded the peak of the "Ning Portfolio" [2].

Guangfa's Liu Chenming also pointed out that fund holdings in TMT exceeded 40% last year, with electronics holdings consistently above 20% for over a year. From a trading crowdedness perspective, the turnover ratio of A-share TMT has long broken through the 40% threshold of the last industry cycle.

Despite such crowding, since April, the Philadelphia Semiconductor Index has risen 54%, and the STAR Semiconductor Index has risen 60%. Not to mention Mr. Fu who heavily bought into Zhongji Innolight in Q1, even 18 fixed-income-plus funds that raised semiconductor holdings above 10% have pulled off thunderous NAV surges.

Another peculiar aspect of this cycle is that no matter how much Hang Seng Tech falls, it just can't get up.

Two months have passed since Xia Junjie said "Hang Seng Tech may have fallen too much," yet it remains lifeless, like a dead fish lying flat-eyed on ice at a seafood stall.

The persistent weakness of Hang Seng Tech has its reasons. As Juming's Liu Xiaolong explained why he cleared Hong Kong tech stocks: 1) Potential impact of AI on internet business models; 2) Hong Kong stocks are more affected by marginal tightening of overseas liquidity; 3) Large IPO fundraising volumes in 2025, consuming capital.

In essence, the current large model landscape remains one of winner-takes-all and long-tail homogenized competition. Hongshang Asset believes that the "free" and "low-cost" cutthroat tactics in the C-end have led to a valuation dilemma for Chinese AI companies:

When monetization capability is heavily questioned, even the AI businesses of Tencent and Alibaba struggle to gain market recognition. Although models like Alibaba's Qianwen have started trying closed-source, paid models, the results aren't great. This is also why the market has gradually lost patience with Tencent and Alibaba's AI stories recently, and the core reason for their lack of valuation expansion momentum.

The most bizarre aspect of this cycle is that consumer fund managers are starting to transform and chase the light.

A while back, thinking of bottom-fishing in consumer funds, "Bosera Women's Consumption Theme" seemed appealing by name. But opening its top ten holdings revealed Crystal Optech and Zhongji Innolight staring back.

Well-known consumer veterans Tong Xun and Xiao Nan are also gradually blending with the light. After shifting their mindset, Mr. Tong's NAV saw a V-shaped reversal since April; after Q3 last year, the "light content" in Xiao Nan's managed Yifangda Ruiheng gradually increased, widening the performance gap with his peer Zhang Kun, who remains mired in baijiu.

These bizarre phenomena remind one of the peak of the last subjective long-only cycle in 2020-2021.

Only back then, the protagonists were 60s-generation fund managers with muscle memory for "monopoly barriers + perpetual operation," overweighting Kweichow Moutai and Alibaba relative to the market. This cycle's protagonists are 85s-generation managers with extreme faith in hard tech, overweighting Zhongji Innolight and Cambricon relative to the market, most experiencing the 4200-point level for the first time since managing money.

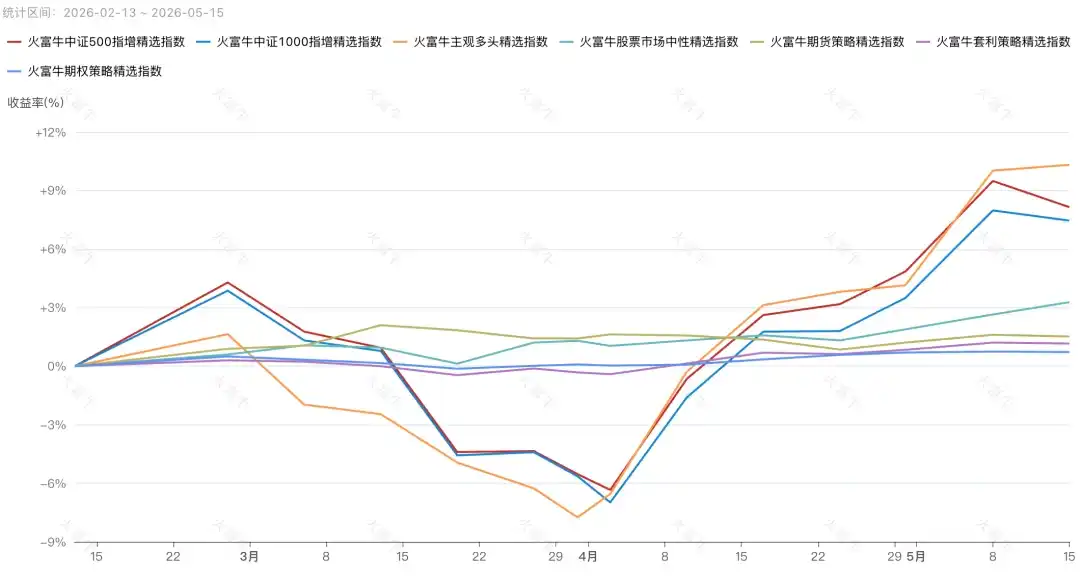

If not for AI, subjective long-only managers, suppressed by quant for years, haven't felt this proud in a long time. Over the past year, 12 public offering subjective long-only products have yielded over 300%; in the past three months, the Huofuniu Private Subjective Long-Only Selected Index has overtaken the CSI 500 Index Enhancement Selected Index to become the strongest strategy index.

Ren Zeping says this is a once-in-a-decade bull market, a confidence bull formed by the叠加 of policy bull + tech bull + liquidity bull. I think a more accurate expression is: it's a bull market for those confident in silicon, and a bear market for those trying to bottom-fish in carbon.

Attack or Defend

For many fund managers, the current situation is like Hansi Flick leading this impoverished Barcelona—there seems to be no other choice.

Flick's tactic is to defend through attack, using high-pressuring to keep the ball in the opponent's half, reducing the chance of them facing his own goal. Once they fall back and bunker, relying on Barcelona's weak defense, they'd only lose worse. Similarly, even defending in Hang Seng Tech and consumer stocks, they'll still fall when the bull market ends, but at least attacking by buying AI can accumulate profit cushions.

Moreover, under extreme FOMO sentiment, managing liability-side emotions is getting harder. After all, clients can easily make money chasing the light themselves in stocks. Seeing friends' subjective funds all pulling thunderous NAVs, why spend time and management fees listening to you preach value investing, only to miss one of life's few era-defining trains?

Since it's a fast-moving train of the times, should those not on board chase? Should those on board get off? These are questions all managers must face directly. Just like how the capital expenditures of the US tech giants have been revised up all the way to $720 billion, no one wants to be left behind by the times.

Wang Zhongyuan, founder of Ziruixing Investment who entered the industry in 1993, lived through the 1995 "327" Treasury Bond incident and witnessed the 1999 internet bubble. He told Yuanchuan a true story:

Stanley Druckenmiller shorted tech stocks in the first half of 1999, went heavily long by year-end, and liquidated at the top in January 2000. But by March 2000, when tech soared again, he couldn't hold back and went all-in, losing 18% in a month and a half.

"What does this story illustrate? Even the world's公认 top trader can make irrational decisions when facing FOMO. So, how many of today's fund managers chasing the light do you think are more厉害 than Druckenmiller?"

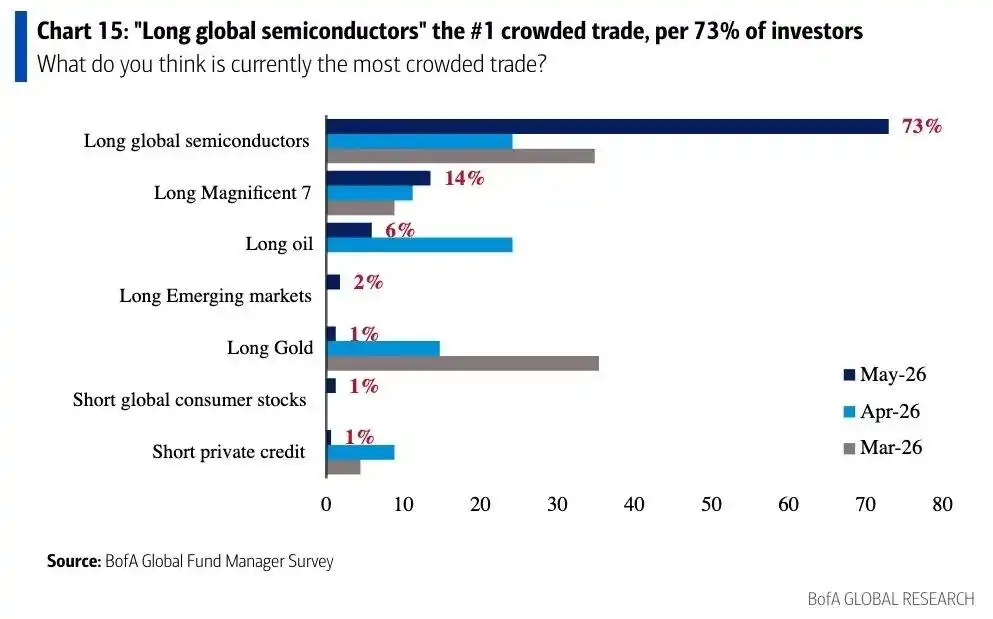

Interestingly, Zeyuan Investment posted a chart on their public account—"Semiconductors Rank First in Global Trading for May."

They advised investors to lower expectations for Zeyuan. The current situation resembles the peak of the dot-com bubble. They would never abandon traditional value investing to chase the dot-com bubble, even if it boils over, "never surrendering." They quoted a line, "The stock market is where dreams and money are exchanged. Those who sell their套取金钱, while those who付出金钱大多套牢守望梦想."

Compared to Ziruixing and Zeyuan, Jingyi Investment expressed it more bluntly—the underlying large models of this AI revolution, and the most core infrastructure and hardware, are overwhelmingly in the hands of those美股头部科技巨头 across the ocean. The fundamental支撑 of the current A-share AI speculation is far weaker than that of new energy back then.

"In 2021, most光伏 and lithium battery companies were伴随着实打实的业绩爆发 and rapid渗透率提升. But many of today's so-called 'AI companies' in A-shares,炒作到市值几千亿, don't even have that momentary profit爆发 of the new energy era."

It's undeniable that some subjective私募 aren't gambling. They withstood the short-selling打击 of Michael Burry's $379付费文章 last year and captured that the core主线 of AI investment is AI hardware. But as the speculation扩散 from optical modules to memory, CPU, electronic fabric,光纤等细分环节, the room for rotation within the板块不断收窄, and the potential代价 of making mistakes is also抬升.

Coupled with the 30-year US Treasury yield breaking 5%, chasing AI now versus when Michael Burry called the bubble last year happens under different macro situations.

It's like Flick's Barcelona, sailing smoothly this season, occasionally刷出雷霆比分. Until the Champions League quarter-finals against counter-attacking specialist Atletico Madrid, they stubbornly persisted with high attacking, leading defenders to frequently追回, receiving two red cards,彻底葬送了比赛.

Epilogue

When people still believed in carbon, thunderous NAVs weren't unheard of either.

In the last baijiu bull market, from 2020 to June 2021, Lin Yuan's performance rose 150%, only to fluctuate and decline for the next five years, now只剩下20%多的收益. Zhengyuan and Chongji, which集中押注光伏新能源 back then, are even more memories wealth managers不愿回首.

Then there's Shifeng Asset, which previously pulled off thunderous NAVs and peaked at 30 billion AUM.尝试转型量化也未能扭转颓势, its规模萎缩到20-50亿, recently learned to have moved from the prime Lujiazui Century Financial Plaza to the cheaper Yuanshen Financial Tower.

These may seem somewhat distant, but at the beginning of the year when gold prices stood at highs, that gold私募 that yelled "sit tight and hold on" three times probably isn't so easily forgotten.

I sometimes ask渠道人士 why they看好某家私募. The answers不外乎三点: Entrepreneurs who left big firms, strategies still effective at small scale, and the most core one—the NAV curve颜值好.

Behind thunderous NAVs often lie收益放大 from集中持仓乃至加杠杆. Buying solely based on业绩锐度 likely gets you a平庸的产品, merely buying into the过去强势的市场风格. The教训 of buying based on charts has repeated一遍又一遍.

Qinyuan's Wu Dingwen once shared: "Allocation requires认同底层逻辑, meaning认同交易,认同价值,认同团队, not just认同赚钱."仅认同赚钱大概率逃离不了什么火买什么,买什么什么跌,什么跌死在哪的循环.