Last week, the Federal Reserve lowered interest rates to a target range of 3.50%–3.75%—a move that was fully priced in by the market and largely expected.

What truly surprised the market was the Fed's announcement that it would purchase $40 billion in short-term Treasury bills (T-bills) per month, which was quickly labeled by some as "QE-lite."

In today's report, we will delve into what this policy changes and what it does not. Additionally, we will explain why this distinction is crucial for risk assets.

Let's begin.

1. The Short-Term Setup

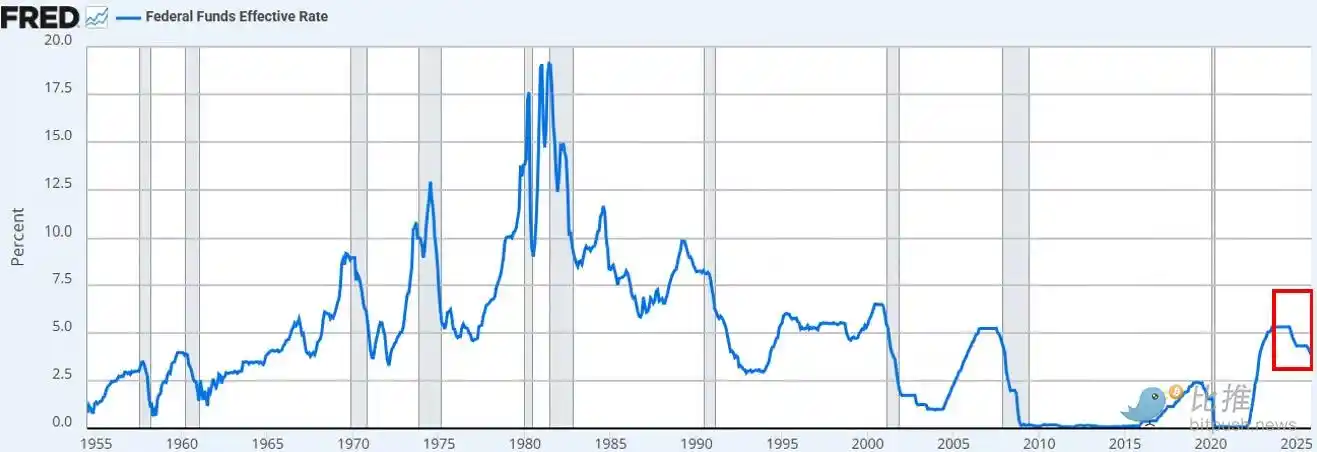

The Fed cut rates as expected. This was the third rate cut this year and the sixth since September 2024. In total, rates have been lowered by 175 basis points, pushing the federal funds rate to its lowest level in about three years.

In addition to the rate cut, Powell announced that the Fed would begin "Reserve Management Purchases" of short-term Treasury bills at a pace of $40 billion per month starting in December. Given the ongoing strains in the repo market and banking sector liquidity, this move was entirely within our expectations.

The prevailing consensus view (both on platform X and CNBC) is that this is a "dovish" policy shift.

Discussions about whether the Fed's announcement equates to "money printing," "QE," or "QE-lite" immediately dominated social media timelines.

Our observation:

As "market observers," we find that market sentiment remains skewed toward "risk-on." In such a state, we expect investors to "overfit" policy headlines, attempting to piece together a narrative while overlooking the specific mechanisms through which policy translates into actual financial conditions.

Our view is: The Fed's new policy is positive for the "plumbing of financial markets," but not for risk assets.

Where do we differ from the prevailing market view?

Our perspective is as follows:

· Short-term Treasury purchases ≠ absorbing market duration

The Fed is buying short-term Treasury bills (T-bills), not long-term coupon-bearing bonds. This does not remove interest rate sensitivity (duration) from the market.

· Does not suppress long-term yields

Although short-term purchases may slightly reduce future long-term bond issuance, this does not help compress term premiums. Currently, about 84% of Treasury issuance is already in short-term bills, so this policy does not materially alter the duration structure facing investors.

· Financial conditions are not broadly easing

These reserve management purchases, aimed at stabilizing the repo market and bank liquidity, will not systemically lower real interest rates, corporate borrowing costs, mortgage rates, or equity discount rates. Their impact is localized and functional, not broad monetary easing.

Therefore, no, this is not QE. This is not financial repression. To be clear, the acronym doesn't matter; you can call it money printing if you like, but it is not deliberately suppressing long-term yields by removing duration—and it is that suppression that forces investors out the risk curve.

That is not happening now. The price action in BTC and the Nasdaq since last Wednesday confirms this.

What would change our view?

We believe BTC (and risk assets more generally) will have their moment. But that will come after QE (or whatever the Fed calls the next phase of financial repression).

That moment arrives when:

· The Fed artificially suppresses the long end of the yield curve (or signals to the market that it will).

· Real interest rates fall (due to rising inflation expectations).

· Corporate borrowing costs decline (fueling tech stocks/Nasdaq).

· Term premiums compress (long-term rates fall).

· Equity discount rates fall (forcing investors into longer-duration risk assets).

· Mortgage rates fall (driven by suppression of long-end rates).

Then, investors will smell "financial repression" and adjust their portfolios. We are not in that environment yet, but we believe it is coming. While timing is always difficult, our base case is that volatility will increase significantly in Q1 of next year.

This is the short-term setup we see.

2. The Bigger Picture

The deeper issue lies not with the Fed's short-term policy, but with the global trade war (currency war) and the tensions it is creating at the core of the dollar system.

Why?

The U.S. is moving into the next phase of its strategy: onshoring manufacturing, rebalancing global trade, and competing in strategically necessary industries like AI. This goal is in direct conflict with the dollar's role as the world's reserve currency.

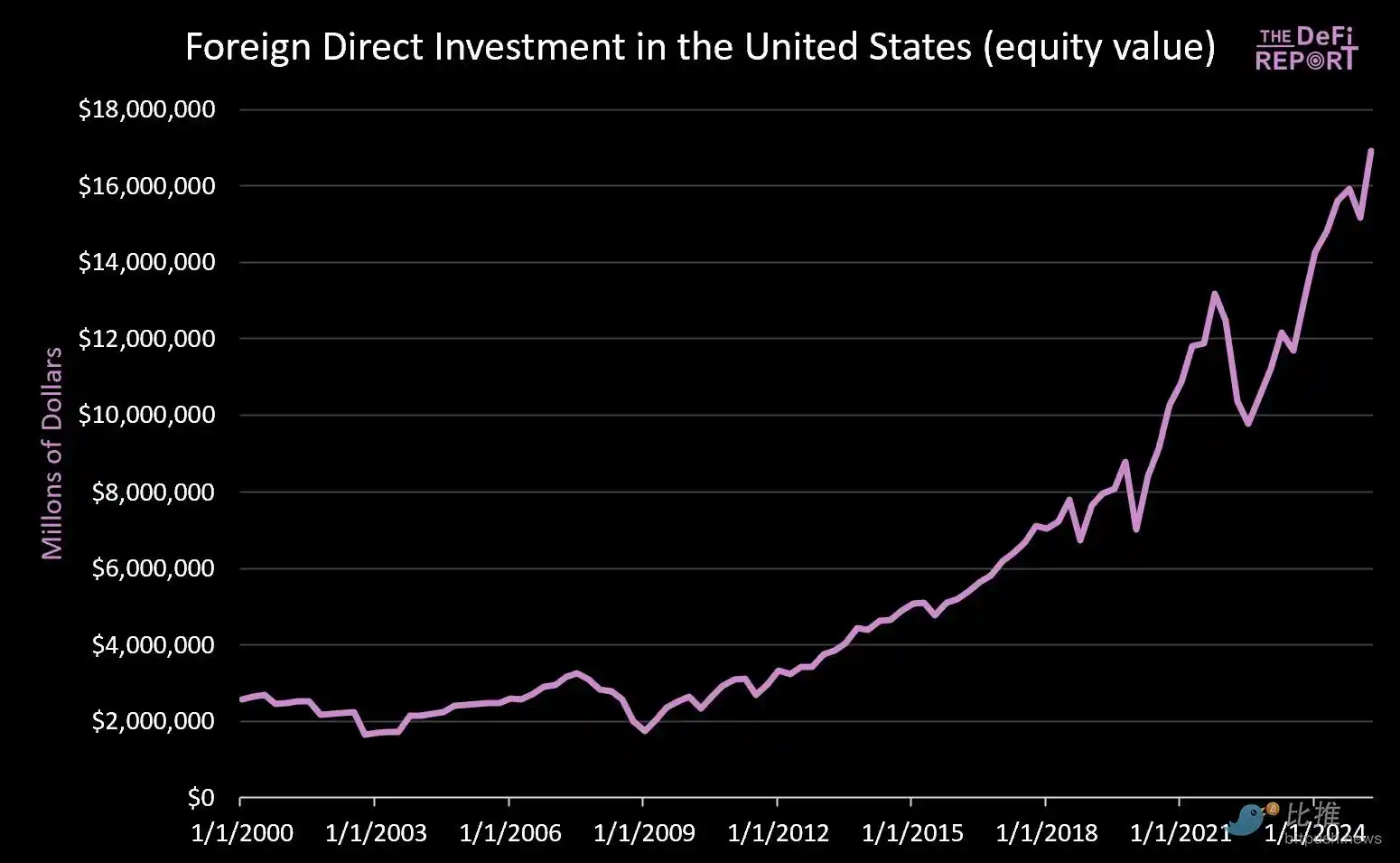

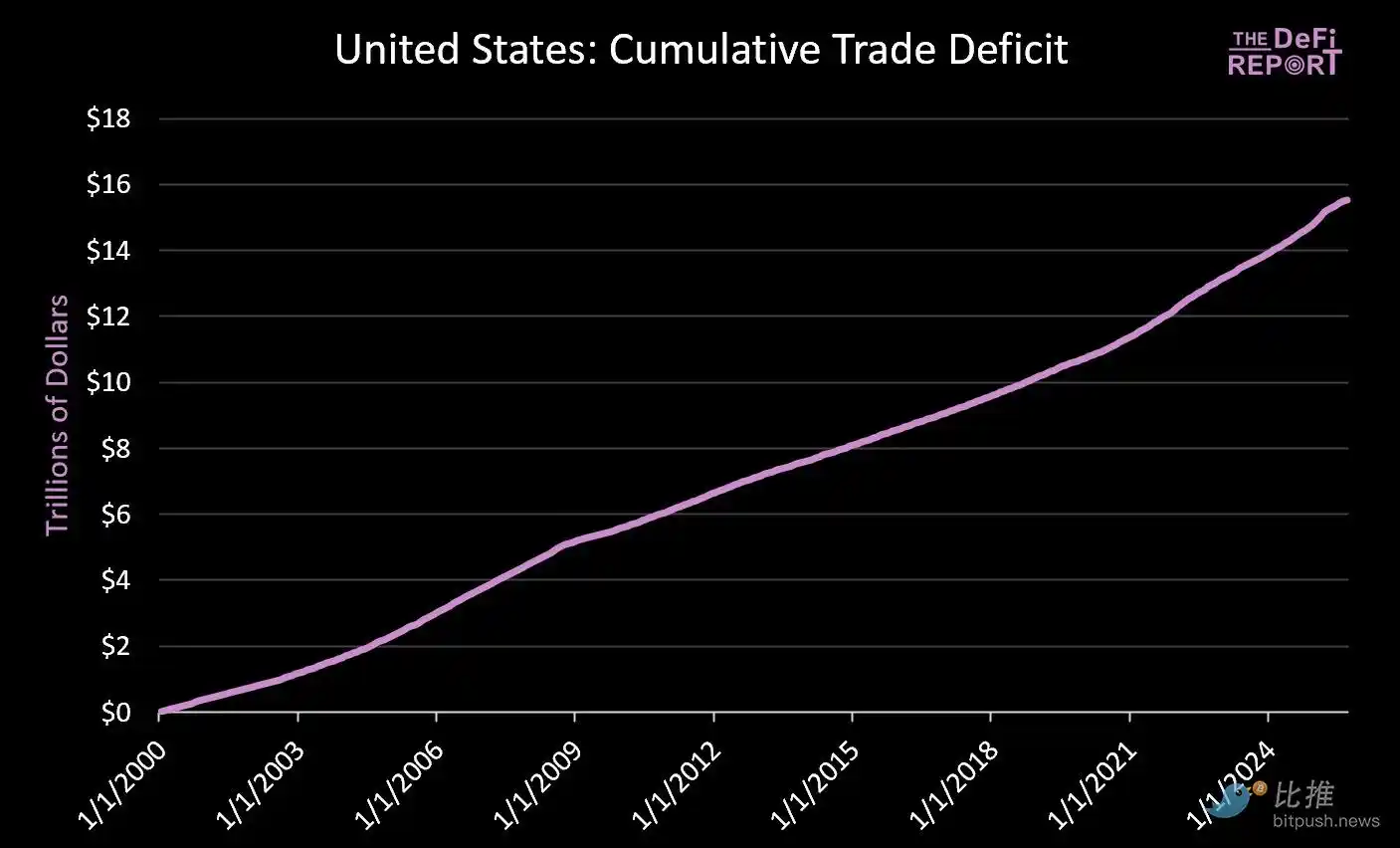

Reserve currency status can only be maintained if the U.S. runs persistent trade deficits. Under the current system, dollars are sent overseas to buy goods and are then recycled back into U.S. capital markets via Treasury bonds and risk assets. This is the essence of Triffin's Dilemma.

· Since January 1, 2000: Over $14 trillion has flowed into U.S. capital markets (this doesn't even include the $9 trillion in bonds currently held by foreigners).

· Meanwhile, roughly $16 trillion has flowed overseas to pay for goods.

Efforts to reduce the trade deficit will necessarily reduce the recycling of flows back into U.S. markets. While Trump touts promises from Japan and others to "invest $550 billion in U.S. industry," what he doesn't say is that Japanese (and other) capital cannot be in both manufacturing and capital markets simultaneously.

We do not believe this tension will be resolved smoothly. Instead, we anticipate higher volatility, asset repricing, and ultimately, a currency adjustment (i.e., a devaluation of the dollar and a write-down of the real value of U.S. Treasury debt).

The core idea is: China is artificially suppressing the yuan (giving its exports an artificial price advantage), while the dollar is artificially strong due to foreign capital investment (making imports relatively cheap).

We believe a forced devaluation of the dollar may be imminent to resolve this structural imbalance. In our view, this is the only viable path to address the global trade imbalance.

In a new environment of financial repression, the market will ultimately decide which assets or markets qualify as "stores of value."

The key question is whether U.S. Treasury debt will continue to function as the global reserve asset once the dust settles.

We believe Bitcoin, along with other global, non-sovereign stores of value (such as gold), will play a far more significant role than they do today. The reason: they are scarce and do not rely on policy credibility.

This is the "bigger picture" setup we see.