TL;DR

Micron is scheduled to release its fiscal year 2026 third-quarter earnings on June 24, with the earnings call set for 4:30 PM ET on the same day. Ahead of the report, Citi has raised its price target for Micron from $840 to $1,200, maintaining a Buy rating, citing stronger-than-expected memory prices in 2026 and high gross margins.

The highlight of this target hike is not the $1,200 figure itself. Based on the stock price of approximately $1,020.76 at the time of the report's release, this target implies an upside of about 18%. However, as of June 23, market data shows Micron's stock price hovering around $1,211, slightly above Citi's target. In other words, the stock has already approached the target price, and the market's focus now shifts to whether Citi's earnings assumptions can materialize.

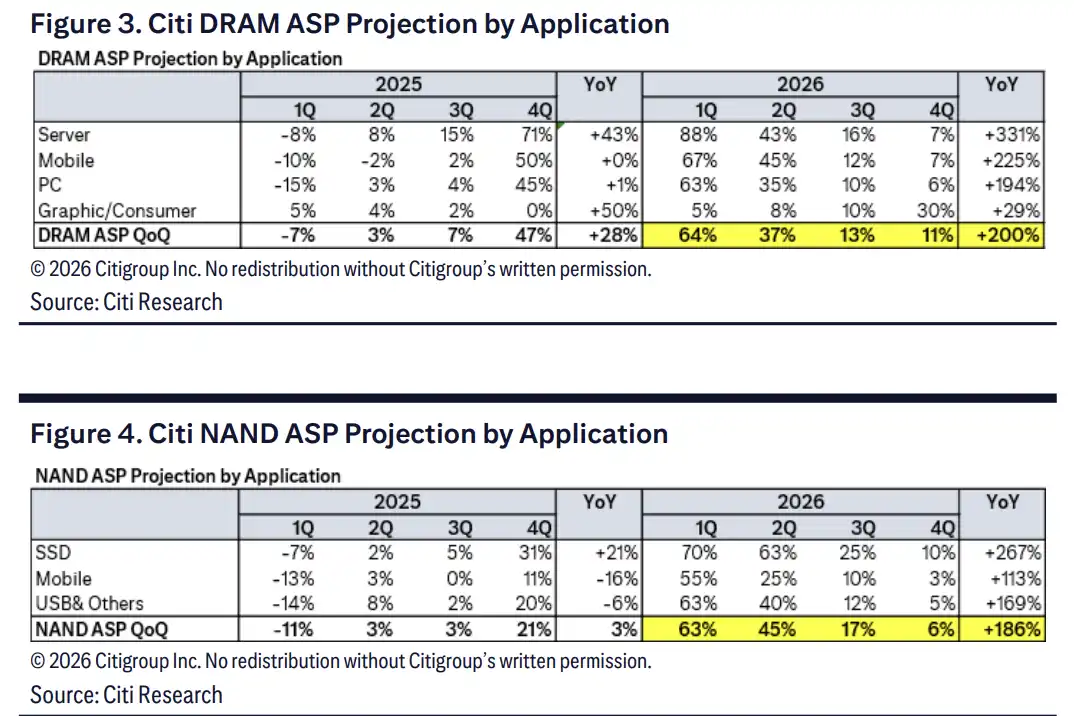

The most aggressive assumptions come from pricing. Public reports citing Citi's view indicate that DRAM average selling prices (ASP) are projected to rise by 200% in 2026, while NAND ASP is expected to increase by 186%. If this wave of price hikes continues to transmit from spot prices to contract prices, there remains room for further upward revisions to Micron's fiscal year 2027 earnings expectations.

Behind the $1,200 Target: Further Upside for FY27 Earnings

According to reports from TipRanks/The Fly, Citi has raised Micron's price target to $1,200 while maintaining a Buy rating. Yahoo Finance and Investing.com, citing related reports, noted that Citi has increased its FY2027 EPS estimate for Micron to $114.73.

Such revisions typically stem from two directions: higher pricing on the revenue side and sustained high gross margins. Memory industry profits are extremely sensitive to price. When DRAM and NAND prices enter an upward cycle, minor quarterly revenue changes can be magnified into larger full-year earnings expectations.

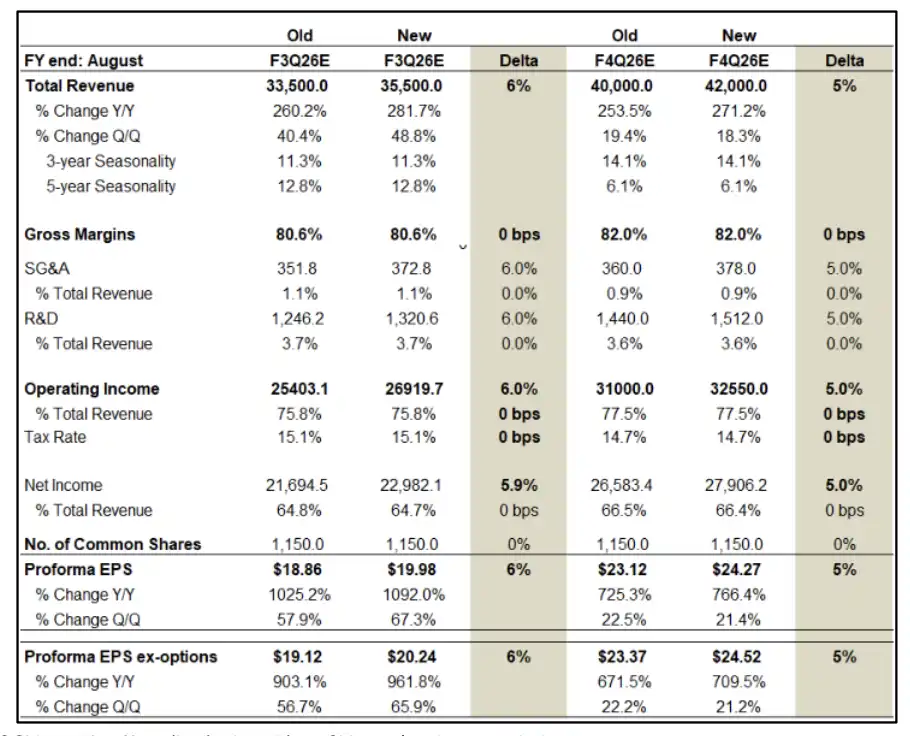

The assumptions in Citi's original report are even more aggressive. The report shows expectations for Micron's F3Q26 revenue at $35.6 billion and EPS at $19.98. F4Q26 revenue is forecast at $42.0 billion with EPS of $24.27. On an annual basis, FY26 revenue is estimated at $115.0 billion, while FY27 revenue is projected to rise further to $197.5 billion, with FY27 EPS revised up to $114.73.

The $1,200 price target reflects high confidence in 2027 earnings rather than being a tactical trade around a single quarter's report. If FY2027 EPS approaches $115, Micron's current valuation may still find support. Conversely, if memory prices peak earlier, and with the stock already near the target price, the margin for error would significantly shrink.

Spot Prices Lead Contract Prices, Hikes Still Propagating to Customers

The direct driver for the upward revisions to Micron's earnings expectations is memory pricing.

Public reports citing Citi data note that DRAM spot prices have risen 52% cumulatively since the beginning of 2026 and are currently about 21% higher than contract prices. In the memory industry, spot prices typically react faster than contract prices. When spot prices are significantly higher than contract prices, contract prices may still be adjusted upward upon customer re-negotiations.

This is also the basis for the substantial upward revision of the 2026 ASP assumptions. Citi expects DRAM ASP to rise 200% for the full year 2026. NAND ASP is projected to increase by 186% for the year, with Q2, Q3, and Q4 expected to see sequential increases of 45%, 17%, and 6%, respectively.

The server segment is the most concentrated direction for price increases. Citi's original report assumes server DRAM ASP will rise 331% for the full year 2026, while NAND SSD will increase by 267%. This indicates that the price hikes are not solely due to PC and smartphone restocking; procurement from data centers, AI servers, and enterprise SSDs represents a stronger source of demand.

HBM Strains Capacity; Supply Discipline Determines Cycle Length

Whether prices can continue to rise depends largely on whether supply remains tight.

Citi's report assumes a global DRAM supply shortage of about 5% in 2026. For the memory industry, such a deficit is sufficient to drive significant price volatility, especially as High Bandwidth Memory (HBM) consumes wafer, equipment, and advanced packaging resources, further squeezing supply for conventional DRAM.

HBM also acts as an amplifier in this cycle. AI training and inference continue to drive demand for high-bandwidth memory, while HBM capacity ramp-up consumes more advanced production capacity. If HBM prices remain strong, Micron's product mix and gross margins may continue to benefit.

The risk lies in the supply side not remaining disciplined indefinitely. TipRanks, citing TrendForce data, notes that global DRAM bit supply is expected to grow by about 30% in 2026, with Micron's growth projected at 42%. If competitors accelerate capacity expansion in 2027, or if new capacity is released faster than AI and data center demand can absorb it, the current assumptions of shortage and high gross margins will be challenged.

Long-Term Agreements Can Smooth Cycles, But Terms Are Key

Beyond price increases, Long-Term Agreements (LTAs) are another part of Citi's optimistic scenario.

Historically, memory companies have been most heavily discounted by the market for their highly cyclical earnings. Profits rapidly expand during price hikes but decline once oversupply emerges, dragging down prices and margins. If customers are willing to lock in longer-term procurement arrangements, the volatility of Micron's revenue and profits over the next few years could be partially smoothed.

Citi's original report mentions that Dell has signed relevant LTAs and suggests such agreements may drive the adoption of complementary NAND solutions like KV cache offload, further opening up SSD and NAND demand. Expectations and reality still need to be separated here: LTAs can improve earnings visibility, but they do not yet constitute a fully validated new business model.

What truly impacts valuation are the detailed terms, including the volume covered, the design of the pricing mechanism, whether there are minimum purchase commitments, and whether customers can adjust orders in response to price changes. If LTAs are merely framework agreements without strong, binding purchase arrangements, their support for Micron's valuation would be significantly weaker.

Stock Price Nears Target; Bear Case Reminds of Cyclical Risks

Citi's base case target price is $1,200. The original report outlines a bull case target of $1,400 and a bear case target of $400. This range itself indicates that market divergence regarding Micron is not about the direction but rather about how long the cycle can last.

Risks are mainly concentrated in three areas.

First, HBM yield and capacity ramp. Slow release of high-end memory supply may intensify price hikes in the short term but could also affect Micron's deliverable volumes and customer qualification progress.

Second, industry capacity expansion. The memory industry has repeatedly seen cycles where high prices stimulate expansion, which in turn depresses prices. It's difficult to completely escape this pattern this time around.

Third, AI and data center capital expenditures. The current price forecasts imply continued expansion in AI server, inference demand, and enterprise SSD procurement. If cloud providers slow spending, or if storage demand growth falls short of expectations, the pace of ASP increases may decelerate.

For Micron's upcoming earnings report, the most crucial aspect is not just whether F3Q26 exceeds expectations, but also how management discusses supply and demand for 2026 and 2027, HBM pricing, LTA progress, and gross margin guidance. The $1,200 target price is built on a combination of continued memory price increases, tight supply, and sustained high margins. If any one of these links weakens, with the stock already near the target price, the market's patience for this uptrend cycle will be even shorter.