A crypto market expert has shared reasons why believes that despite the ongoing bearishness in the market right now, Ethereum (ETH) is still a better investment than Solana (SOL). Over the past few months, Ethereum has been in a slump, with its price falling below key support levels and underperforming the broader market. Meanwhile, Solana has seen its fair share of declines, plummeting by over 10% this past week. Despite the weakness across both assets, the analyst still picks Ethereum over Solana, citing ETH’s bullish drivers beyond price action and market trends.

Why Ethereum Is A Better Investment Than Solana

Emperor Osmo, a market analyst on X has presented a compelling case for why Ethereum remains a stronger bet than Solana despite ETH crashing more than 9.5% in the past week to trade near $1,870 at the time of writing. The analyst said he understands why many market participants and investors have turned bearish on the ETH price, pointing to weak price structure and declining network fees.

Osmo noted that Ethereum’s fee revenue has fallen sharply, while Solana continues to close the gap. According to him, Solana has generated about $3.859 billion in annual app fees compared to Ethereum’s $3.868 billion. The difference now stands at only $9 million after years of ETH maintaining a dominant lead.

The analyst also highlighted that Solana’s app fees are growing by roughly 9.5% per month, while ETH;s are declining by about 6.4%. Despite these trends, the analyst believes one key metric continues to support Ethereum’s long term bullish outlook. He revealed that the second largest cryptocurrency is currently sitting on about $161.8 billion in stablecoins, representing roughly 50.7% of all stablecoin value onchain.

Osmo also pointed to growing institutional interest in Ethereum’s ecosystem. He noted that BlackRock, the world’s largest asset manager, recently filed permissioned ERC-20 treasury products on Ethereum, picking the ETH blockchain above all others.

In addition, the analyst referenced projections from the U.S. Treasury Secretary, Scott Bessent, that the stablecoin market could eventually grow to $3 trillion by 2030. Based on those figures, Osmo argued that if Ethereum maintains its substantial stablecoin market share, more than $1.5 trillion in value could eventually be anchored to the network.

As a result, he believes that even if ETH’s current price reflects concerns around slowing fees and weak market structure, it does not represent its potential value backed by stablecoin growth and long term network retention.

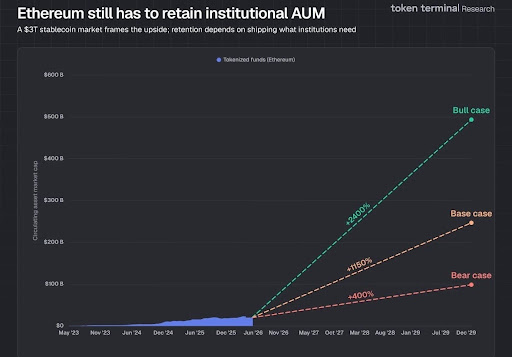

Analyst Outlines Bull, Base, And Bear Case Scenarios For ETH

In an accompanying chart, Osmo mapped out bull, base, and bear case scenarios for Ethereum if it captures a significant slice of institutional stablecoin AUM. The analyst frames ETH’s potential upside against a projected $3 trillion stablecoin market, with retention hinging on whether the blockchain can ship what institutions need.

His bull case projects tokenized funds driving a 2,400% surge in ETH’s circulating asset market cap by December 2029. The base case puts that figure at 1,150%, while even the bear case holds upside at 400%.