Author: Ma He, Foresight News

In May of this year, a 13F holdings report from Jane Street sent the crypto market into an instant frenzy.

This Wall Street's most mysterious quantitative giant suddenly slashed its holdings of the BlackRock Bitcoin Spot ETF IBIT by 71% from 20.31 million shares ($790 million) to approximately 5.9 million shares ($225 million). Its FBTC holdings also fell by 60%, and Strategy holdings were cut by about 78%. At the same time, it was quietly increasing its holdings in Ethereum ETFs by a total of about $82 million.

A month earlier, this company—which has "no CEO and survives on mathematical models and extreme low latency"—had just reported quarterly trading revenue of $16.1 billion and net profit of $10.3 billion, with employee compensation averaging $2.68 million per person, nearly 7 times that of Goldman Sachs. What does this mean in the crypto world? In 2024, Tether, the most profitable company in crypto, had annual net profit of only $13 billion. Hyperliquid, with per capita revenue of $78 million, ranked first globally, yet its revenue for the entire year of 2025 was a mere $908 million.

What exactly is its game in the crypto market? The answer lies in its systematic positioning over the past few years.

Wall Street's Mysterious Player, the Top Behind-the-Scenes Operator in Crypto

Jane Street was founded in 2000. It never manages client assets, trading solely with its own capital across more than 200 exchanges worldwide. It has no CEO and no traditional hierarchy. Each trading desk and business unit is overseen by one of its equity holders, but no single individual has final say. Co-founder Rob Granieri (also one of the defendants in the Luna lawsuit) is seen internally as "first among equals," but major decisions are made collectively by a broader leadership group.

Rob is the only remaining founding partner among the company's four co-founders. Interestingly, it was Rob himself who recruited SBF. SBF later left to found Alameda Research and FTX.

Jane Street Co-founder Robert Granieri

That 13F filing was just the tip of the iceberg. Over the past five years, it has already become the invisible operating system of the crypto market's liquidity infrastructure layer through its Authorized Participant (AP) seat for spot ETFs, its 10-minute front-running before the Luna crash, its suspected anonymous arbitrage addresses in on-chain prediction markets, and its equity investments spread across exchanges and DeFi protocols.

In 2017, Jane Street formally entered the crypto market, led by veteran Thomas Uhm, who has been with the company for 22 years, to spearhead initial business development. In 2018, it launched the institutional OTC trading platform JCX, supporting 24/7 trading of major tokens, and began providing stable liquidity for institutional counterparties.

In May 2022, Terraform Labs quietly withdrew $150 million in UST from the Curve 3pool. Ten minutes later, a wallet associated with Jane Street pulled 85 million UST from the same pool, triggering the death spiral of the $40 billion market.

In January 2024, Bitcoin spot ETFs were approved. Jane Street became the core Authorized Participant (AP) for BlackRock's IBIT, Fidelity's FBIT, and WisdomTree's ETF. This means every retail ETF subscription flows through its hands.

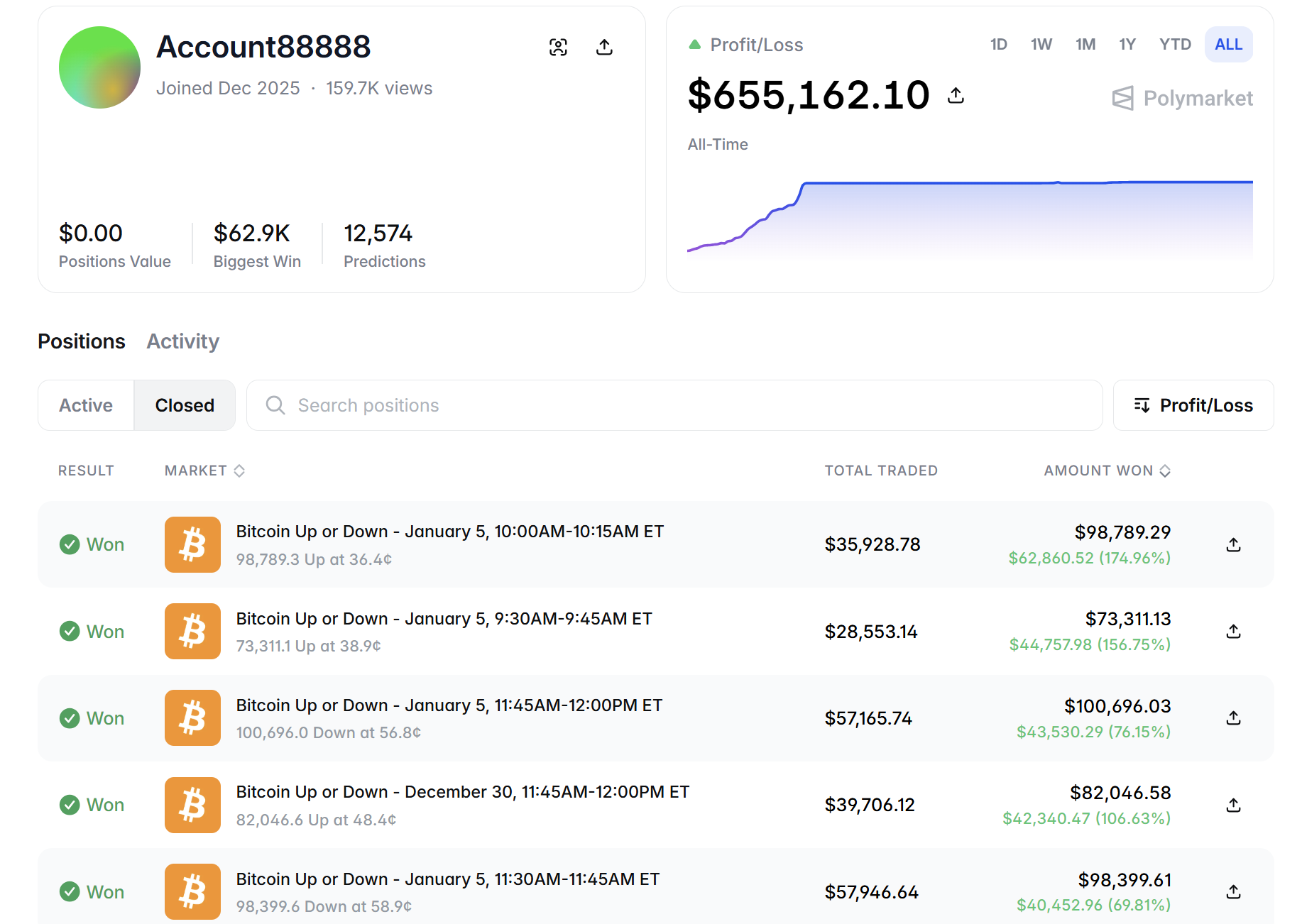

In December 2025, an address signed "JaneStreetIndia" appeared on Polymarket's "15-minute Bitcoin up/down guess" market. The address used a dual-direction betting arbitrage strategy (simultaneously buying up and down, locking in risk-free profit), profiting nearly $360,000 within 25 days.

In crypto infrastructure, Jane Street's imprint is everywhere: Kraken, 1inch (Series B $175 million), Arbitrum, ZetaChain, Euler Finance, Kaito, etc. It also holds equity in mining stocks like Hut 8, Bitfarms, and Cipher Mining on the secondary market.

Its core logic is to deeply embed itself into the liquidity infrastructure layer of the crypto market through methods like front-running, capital arbitrage, and overwhelming advantage, extracting stable "toll fees" and profits from information asymmetry.

The birth of Bitcoin spot ETFs was the moment Jane Street stepped into the spotlight.

The Biggest 'Pipeline Operator' for Bitcoin Spot ETFs

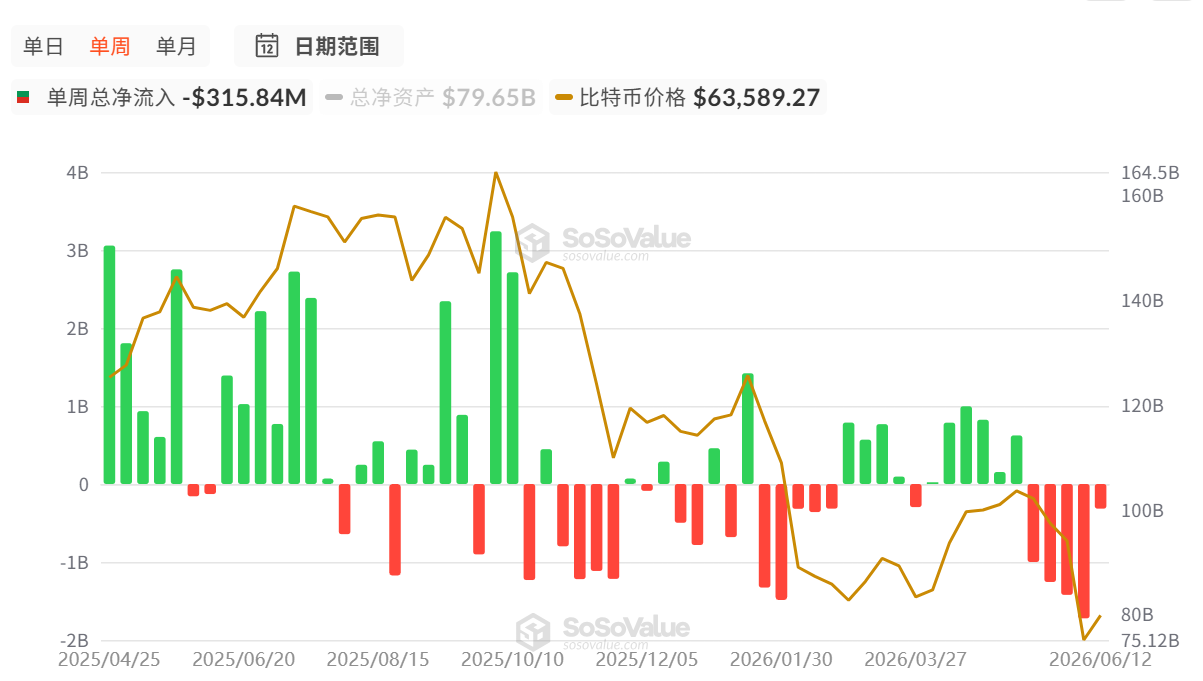

In January 2024, the US SEC approved multiple Bitcoin spot ETFs. After approval, institutional capital flooded in at a pace far exceeding expectations. According to SoSoValue data, as of June 16, total cumulative net inflows reached $53.49 billion, and its inflow/outflow metrics have had a significant impact on BTC prices.

At the pipeline layer of this multi-billion-dollar gateway, Jane Street is the only name appearing in the prospectuses of almost all BTC ETFs—from BlackRock's IBIT and Fidelity's FBTC to WisdomTree. It is either the core AP or even the sole AP.

Retail investors buying IBIT on Robinhood can only buy/sell at market prices, but APs like Jane Street can directly knock on BlackRock's back door, exchanging a basket of physical Bitcoin for ETF shares with the fund company, or returning ETF shares for Bitcoin. This is the so-called "creation" and "redemption."

This "wholesale right" gives APs an arbitrage space inaccessible to retail: when IBIT's market price is higher than its underlying Bitcoin's net asset value (premium), APs buy spot Bitcoin → create ETF shares → sell ETFs on the market, pocketing the difference. When IBIT is at a discount, they reverse the operation. As long as there's a deviation between ETF price and spot price, APs can engage in risk-free arbitrage.

Jane Street's uniqueness lies in the fact that it is not only an AP but also a market maker. It exchanges shares with BlackRock at the "wholesale layer" while providing buy/sell quotes to retail investors at the "retail layer," capturing spreads on both ends. When Bitcoin spot ETFs were approved in January 2024, all 11 applicants listed it as an AP in their prospectuses—Valkyrie even selected only 2 APs, one of which was Jane Street.

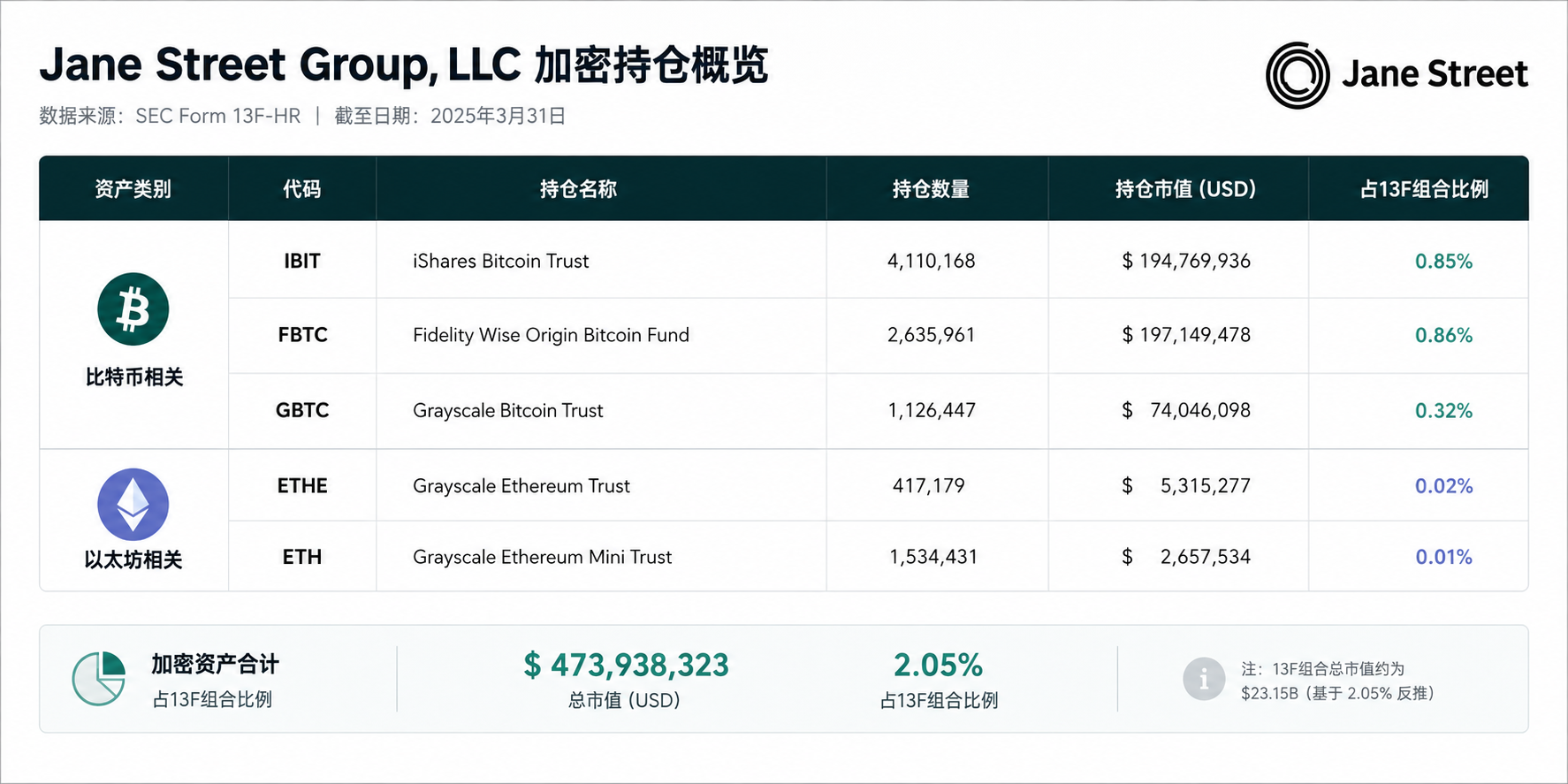

In its Q4 2025 13F filing, Jane Street held approximately 20.31 million shares of IBIT, worth about $790 million. In Q1 2026, it slashed holdings by 71% (IBIT down to ~5.9 million shares, value ~$225 million). In just three quarters, its IBIT position fluctuated wildly like a rollercoaster. Interestingly, in Q1 they increased holdings in ETH ETFs by about $82 million.

It's important to note: This is not a "long-term value investment" holding curve; it's the inventory fluctuation of a high-frequency market maker—positions swing back and forth with arbitrage opportunities, maxing out when opportunities arise and pulling back when premiums converge. This is how they make money.

Former hedge fund manager Michael Green commented: "It's unsettling to see people interpreting Jane Street's 13F as a bullish signal. These holdings are almost certainly hedged with undisclosed options and futures. They are not building a position in Bitcoin; this is standard market making."

Furthermore, beyond Bitcoin and Ethereum, the market maker for SOL ETF was also revealed to be Jane Street.

Compared to other market makers, Jane Street is particularly dominant in complex/non-mainstream ETFs (like fixed income, international equity, commodity, and crypto ETFs). They combine quantitative technology with fundamental/correlation analysis. They transform ETF demand into correlation signals and hedging strategies, willing to hold positions longer to achieve structural arbitrage.

In contrast: Citadel and Jump Trading lean more towards ultra-low latency pure technical high-frequency trading, where speed is the core competitive edge. Jane Street's speed isn't the fastest, but its risk management system and balance sheet allow it to hold positions longer during volatility, thus capturing spreads others cannot hold long enough to realize.

When it simultaneously serves as the Authorized Participant for IBIT, FBTC, and multiple Ethereum ETFs, it collects not returns from directional bets, but the "toll fees" generated by the entire crypto institutionalization process—every subscription, every redemption, every arbitrage rebalancing is completed through Jane Street's pipelines.

However, this model faced a setback in the Indian market, serving as a cautionary tale.

In July 2025, India's market regulator SEBI issued a temporary entry ban against Jane Street-related entities for market manipulation and froze assets worth about 48.4 billion rupees (approximately $566 million). SEBI's 105-page ruling alleged that on 18 derivatives expiry days between January 2023 and March 2025, Jane Street employed a tactic of "pumping up index component stocks in the morning session, simultaneously establishing massive short option positions, then reversing and dumping in the afternoon session to cash in option profits," systematically manipulating India's Bank Nifty index. While recording about $7.5 million in losses in the spot market, it made about $89 million from the derivatives side.

This compliance giant carries a hidden knife, and its inside front-running has landed it in significant controversy.

The Crucial 10 Minutes: The 'Igniter' of the Luna Crash

On February 23, 2026, Terraform Labs bankruptcy administrator Todd Snyder filed an 83-page complaint in the U.S. District Court for the Southern District of New York. The defendants included Jane Street Group LLC, Jane Street Capital LLC, co-founder Robert Granieri, and two employees, Bryce Pratt and Michael Huang.

The core allegation: Before the May 2022 Terra collapse, Jane Street obtained advance knowledge of the liquidity crisis through an internal information pipeline, executed a precise withdrawal of $85 million UST within 10 minutes, thereby avoiding losses exceeding $200 million, and later attempted to buy back Luna at a steep discount after the crash.

Bryce Pratt had interned at Terraform Labs before joining Jane Street. He created a private chat group called "Bryce's Secret," connecting internal Terraform engineers with Jane Street's trading desk. Through this pipeline, Jane Street learned the specific timing and amount of the withdrawal from the Curve 3pool before Terraform made a public announcement. For a quantitative trading firm, this "time advantage" translates directly into arbitrage opportunity.

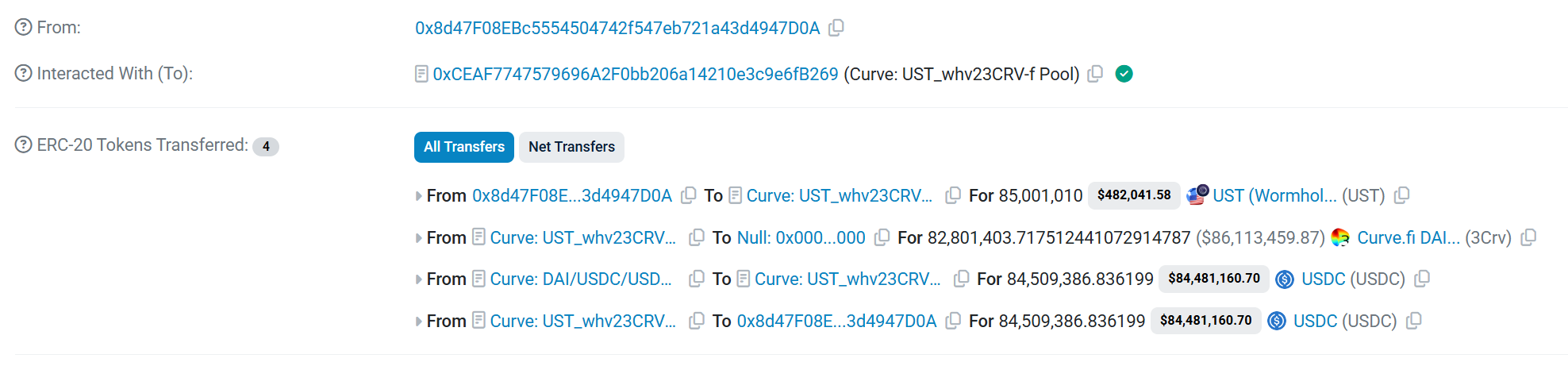

On May 8, 2022, at 17:44, Terraform Labs withdrew $150 million in UST from the Curve 3pool. This operation was not publicly announced at the time (Transaction Hash: 0x18bd477f9beeff22b2ad0c6d48a9c0f02b542049789f0638f5ec50365f1d1de7).

Thirteen minutes later, a wallet identified in the complaint as associated with Jane Street executed an 85 million UST swap from the same pool (Transaction Hash: 0xaa23df48c53f221d0e8ac60ffc9e69340f3e8948fcdc936f3aee9c887d802abb). This was one of the largest single swaps ever on the Curve platform.

The complaint's logic: If Jane Street had not known Terraform's plans in advance, it could not have executed such a precise, massive counter-operation within just 10 minutes of Terraform completing its large withdrawal. Normal quantitative models require reaction time; this wallet reacted in 10 minutes.

More critically, after Terraform's withdrawal, the 3pool's liquidity was already significantly weakened. Pulling out another 85 million at that moment was like kicking a wobbling table, directly shattering market confidence and triggering the UST de-peg.

By withdrawing early, Jane Street avoided massive devaluation of its UST and Luna-related positions during the death spiral. The complaint cites a specific figure: over $200 million. The plaintiff raised 13 legal claims, covering insider trading, securities fraud, violations of the Commodity Exchange Act, unjust enrichment, and breach of confidentiality duties, seeking damages and disgorgement of all illegal gains.

On April 23, 2026, Jane Street filed a 39-page motion to dismiss, with three core defenses:

- Terraform itself engaged in tens of billions of dollars in fraud; a bankrupt party cannot shift the disaster onto others;

- Terraform's on-chain operations were themselves publicly visible; a 10-minute window does not constitute non-public information;

- Its largest single transaction occurred *after* Terraform's withdrawal, not before. A company spokesperson called it a "desperate lawsuit and baseless shakedown."

The 2022 crash, viewed by countless people as a crypto "black swan," is gradually revealing another face under post-facto legal scrutiny: while retail investors scrambled to escape, institutions closest to the core information may have long been standing at the exit.

Prediction Markets: Not Guessing Up/Down, Just Collecting the 'Time Tax'

If the aforementioned dimensions are Jane Street's explicit positioning in the crypto world, then its potential influence in on-chain prediction markets constitutes a more difficult-to-quantify but increasingly noteworthy implicit dimension.

When traditional quantitative giants extend their reach into native on-chain markets, a form of overwhelming advantage occurs. And Polymarket—this prediction market platform that processed over $9 billion in trading volume in 2024 and broke $13 billion in 2025—has become the latest hunting ground.

Ironically, after being heavily fined and kicked out of the Indian market by SEBI in 2025, Jane Street's traders seem to have quickly found a new outlet in the crypto-anarchic prediction markets.

In December 2025, an address signed "JaneStreetIndia" appeared on Polymarket's 15-minute Bitcoin up/down guess market.

According to on-chain statistical analysis, this account is an ultra-high-frequency trading bot. Its operational logic completely deviates from ordinary players' "prediction" scope, focusing purely on mathematical and latency arbitrage.

This account primarily targets event contracts: It almost never touches long-term political elections or cultural events, focusing 100% on extremely high-frequency, high-volatility markets with fast-resolving outcomes like "15-minute cryptocurrency price up/down."

Trading Frequency and Win Rate: Based on recent on-chain statistics, the account executed over 11,000 trades in its first two months of operation. More terrifyingly, its win rate consistently remained above 95%. In the earliest 25-day data exposure, it was profitable for 23 out of 25 days.

According to on-chain data statistics, the address made $360,000 in the first 25 days. After running for another 2 months, total profits quickly soared to approximately $645,000.

This style of play forms a stark contrast with the early individual trader era on Polymarket. In early 2024, anonymous developer @defiance_cr ran a market-making bot on Polymarket with $10,000 capital, earning $700-$800 daily, translating to an annualized return of about 2700%. But by early 2026, he chose to open-source the code and exit, citing inability to profit under current market conditions—because institutional-grade competitors had entered.

A crucial disclaimer is necessary: As of now, no blockchain analytics platform has officially tagged this address, and Jane Street has never publicly acknowledged any connection. All associations are speculative, based on on-chain behavior. However, the following speculation points heavily towards Jane Street.

This address harvests the deviation between contract prices and settlement prices by simultaneously buying up and down. In essence, it's the same convergence arbitrage logic used in spot ETFs transplanted into a different market.

The address executed over 11,000 trades with a win rate approaching 100%. Human traders cannot maintain such discipline over 25 days; only a system with institutional-grade computing power and low-latency infrastructure can continue harvesting in such a squeezed environment.

Furthermore, changing from an identifier with institutional connotations to a completely meaningless numeric string—if a retail investor was impersonating, they would typically boast or abandon the address after attention; but choosing the most covert path for continued operation aligns more with a typical institutional compliance playbook: no explanation, just concealment.

Jane Street's core competency is extreme low latency (FPGA hardware, microwave networks, fiber optic infrastructure). The 15-minute up/down market cycle is extremely short, demanding extremely high latency—while retail investors are still refreshing pages, the bot has already completed order placement, hedging, and settlement. This address choosing 15-minute short cycles over long-term predictions indicates its advantage lies in speed, not judgment, which highly matches Jane Street's DNA.

Why is it unlikely to be other quantitative institutions like Jump Trading?

In February this year, Bloomberg reported that Jump Trading had acquired equity stakes in Polymarket and Kalshi and assembled a ~20-person prediction markets trading team; DRW was recruiting prediction markets traders with a $200k base salary; SIG became Kalshi's first official market maker. These "regular armies" enter in a compliant, equity-based, team-based manner.

Jane Street's entry method is anonymous, bot-based, zero-sum. It doesn't seek platform partnerships but appears directly as an on-chain address, harvesting with the most aggressive arbitrage strategies. This guerrilla approach aligns more closely with Jane Street's modus operandi in the Luna incident (information advantage, low-profile execution, post-fact denial).

For Jane Street, Polymarket isn't an experimental ground to believe in the "ideal of decentralized prediction markets"; it's a new, liquidity-insufficient, pricing-inefficient volatility surface—to be harvested.

This reveals a deeper structural issue: When an institution simultaneously possesses pricing power in the spot market, participation capability in the derivatives market, and potential liquidity influence in the prediction market, the information and capital loop formed between these three layers can theoretically achieve highly synergistic profit extraction.

Even if all operations are within the legal framework, the information asymmetry brought by this multi-layer penetration is enough to place ordinary retail traders' decision-making at a severe disadvantage.

This is not a conspiracy theory; it's the reality of financial market structure.

Conclusion

Jane Street is not an institution that invests in crypto. It does not bet on Bitcoin's rise or fall, doesn't care which public chain wins, and isn't even concerned with whether the ideal of decentralization is realized.

Reviewing its multi-faceted positioning: On the hundred-billion-dollar gateway of Bitcoin spot ETFs, it earns not returns from Bitcoin appreciation but the "toll fees" from the basis spread between ETF shares and spot net asset value. In the 10-minute window of the Luna crash, it obtained the coordinates of the collapse in advance, avoiding major losses. In the infrastructure layer, it broadly invests in Kraken, 1inch, Arbitrum, and Bitcoin mining stocks—not betting on who wins, just ensuring that whoever wins, it holds influence over the infrastructure. On Polymarket's 15-minute up/down guess market, it turns the prediction market into another volatility harvesting machine.

Operators never stand on stage. When the operator becomes the infrastructure itself, the market no longer needs an operator.

It has become the market.

When traditional Wall Street's top-tier regular armies penetrate all aspects of DeFi, OTC, and even native on-chain prediction markets like Polymarket, is the "permissionless, retail-friendly" alpha space that the crypto world prides itself on being permanently erased? When so-called genius individual traders are forced to open-source code and exit the game, is the crypto industry becoming more mature, or has it completely turned into another pool of flesh and blood for Wall Street?

Perhaps there is no agreed-upon answer.