Charles Hoskinson used his latest livestream to argue that Cardano’s next phase should focus less on abstract decentralization rhetoric and more on fixing a structural weakness he says still defines crypto: the reliance on centralized off-chain infrastructure. In the process, he tied that critique directly to Cardano’s treasury debates around BlockFrost, Midnight, partner chains and the broader direction of the network.

Speaking from Wyoming in a late-night broadcast recorded on April 23, Hoskinson framed the discussion around “My First Impressions of Web3,” a January 2022 essay by Signal co-founder Moxie Marlinspike. He described the piece as one of the texts that convinced him to acquire BlockFrost, saying Moxie had identified “the uncomfortable hidden truths” behind the industry’s decentralization claims.

Cardano Can Succeed Where Web3 Fell Back

Hoskinson spent much of the stream reading and unpacking Marlinspike’s central argument: that users do not want to run their own servers, protocols move slowly, and most supposedly decentralized applications still depend on centralized companies for the actual user experience. One of the essay’s most important passages, in Hoskinson’s telling, was this: “Once a distributed ecosystem centralizes around a platform for convenience, it becomes the worst of both worlds. Centralized control but still distributed enough to become mired in time.”

That line became the throughline of Hoskinson’s own case for Cardano. He acknowledged that the problem is not unique to Ethereum, even though Marlinspike’s original examples focused on Infura, Alchemy, MetaMask and OpenSea. “So, we’ll stop for a moment and we’ll ask is Cardano any different?” Hoskinson said. “The answer is no. That’s the uncomfortable hidden truth that Moxy’s talking about.”

From there, he shifted from diagnosis to strategy. Hoskinson argued that Midnight had to come first because it brings the cryptographic building blocks needed for a more coherent trust model, citing multi-party computation, zero-knowledge cryptography and trusted execution environments. But, he said, privacy and cryptography alone are not enough if the infrastructure layer remains dependent on centralized service providers.

That is where BlockFrost entered the picture. Hoskinson said the company’s long-term role should be to become “a decentralized infrastructure network,” effectively a decentralized alternative to the developer platforms that now sit between users and blockchains. “BlockFrost destiny, should we fund it, is to become the decentralized infra Alchemy that we all wish we would have had,” he said, “and something that Moxy could write about as the proper good alternative, the thing that actually is philosophically consistent.”

He bolstered that point with the economics of crypto infrastructure. Citing a February 2022 funding round, Hoskinson noted that Alchemy reached a $10 billion valuation after raising $200 million, up sharply from a prior $3.5 billion valuation. For Hoskinson, those numbers were not just venture-market trivia. They were evidence that the real control points in crypto often live outside the chain itself, in the companies that host, index and shape the interfaces through which users interact with the network.

Hoskinson also used the stream to connect this thesis to Cardano’s treasury voting process. He said the proposals now in front of the ecosystem are not random funding asks, but part of an end-to-end push to decentralize the application layer, improve scalability, connect Cardano to other systems and build off-chain infrastructure that does not simply recreate Web2 chokepoints.

“There’s always going to be a part that’s offchain,” he said. “It bothered me deeply to say that we are these web three people, but we’ve created an incentive system for companies to accelerate and grow and basically take the off-chain component and define and sculpt the user experience.”

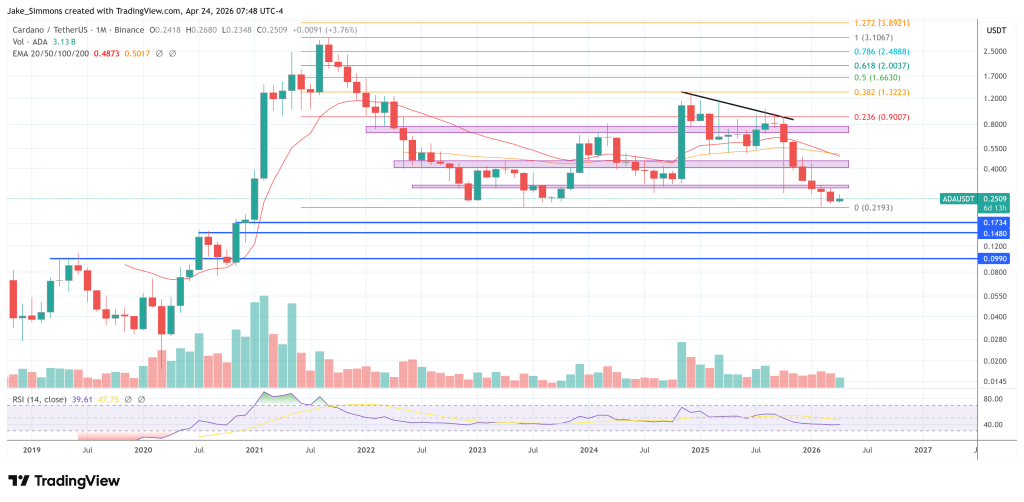

At press time, ADA traded at $0.25.