Fidelity Digital Assets has used a new research report to make a sharper institutional case for bitcoin: not that every allocator must own it, but that a zero position now needs to be actively defended. In a study published March 25, Chris Kuiper argues bitcoin’s role in portfolios can no longer be dismissed as a fringe question, especially as the assumptions behind the classic 60/40 mix come under pressure.

The report opens with an unusually direct framing. “The central question is no longer” whether bitcoin merits consideration, Fidelity says. Instead, it asks: “What is your current bitcoin allocation, and why?” For the firm’s research team, zero exposure may still be valid, but it now requires a “well-informed rationale.”

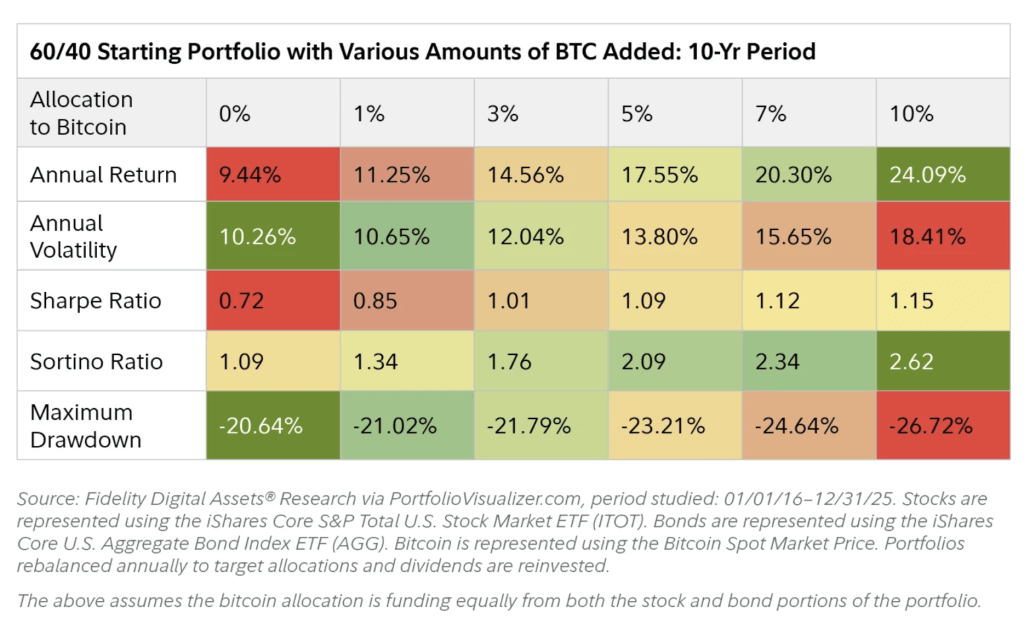

Tiny Bitcoin Exposure, Big Portfolio Impact

That argument rests first on bitcoin’s historical numbers. Fidelity says bitcoin has been the top-performing asset in 11 of the past 15 years and, over multiple time horizons, has posted the highest returns as well as the highest risk-adjusted returns among the assets it examined. The report acknowledges the familiar objection, bitcoin’s volatility remains the highest in the group, but argues that Sharpe and Sortino ratios still compare favorably, while bonds have looked particularly weak on both nominal and inflation-adjusted terms.

From there, the paper tries to move the discussion away from philosophy and into portfolio construction. Fidelity leans on bitcoin’s hard cap, its low long-term correlation to major asset classes, and its sensitivity to monetary expansion.

One of the report’s stronger macro claims is that changes in global M2 have explained 87% of BTC’s price changes over the past 15 years on an r-squared basis, though Fidelity explicitly notes that correlation does not by itself prove causation. It also argues that bitcoin and gold are similar enough to share an inflation-hedge narrative, but distinct enough to remain complementary rather than interchangeable in diversified portfolios.

The most consequential section for allocators is the portfolio work. Using a traditional 60/40 portfolio of US stocks and aggregate US bonds as the base case, Fidelity says adding BTC would have historically lifted both annual and total returns. Volatility rose, as expected, but the report says the increase was compensated by stronger risk-adjusted returns, with the biggest improvement in Sharpe and Sortino ratios showing up when allocations moved from 1% to 3%.

Perhaps more notable for conservative managers, Fidelity says maximum drawdowns did not increase as dramatically as many would assume, partly because of low correlation and partly because annual rebalancing kept the bitcoin sleeve from dominating the portfolio.

Fidelity’s modeling gets more aggressive deeper in the paper. In a mean-variance optimization exercise using what it calls conservative bitcoin assumptions, 25% expected annual return and 50% volatility, against 14.5% expected equity returns and 2% for bonds, the maximum-Sharpe portfolio included 9.4% bitcoin and no bonds at all.

A separate Kelly Criterion exercise produced a 65% position size using historical annual returns, though Fidelity immediately warns that this is not an investment recommendation and notes that more conservative assumptions bring that figure down to 10%. The point is less that institutions should adopt those weights than that BTC’s asymmetric payoff profile can justify larger allocations than intuition might suggest.

That is where the report’s challenge to 60/40 becomes explicit. Fidelity argues the last decade’s strength in traditional portfolios was helped by four decades of falling rates, richening equity valuations, and repeated policy support for credit markets.

It questions whether those tailwinds are durable. On bonds, the paper points to episodes of sharp losses, rising stock-bond correlations, and the risk of negative real returns in a world of persistent debt expansion; on equities, it argues that elevated valuations may leave markets “priced for perfection” even if AI and capital-light business models support margins.

The report stops short of prescribing a universal BTC weight, but its message is clear enough. Fidelity is not presenting bitcoin as a replacement for every traditional asset or as a one-way macro hedge. It is arguing that in a world where fixed income may no longer offer the same ballast and equity valuations already reflect high expectations, even a small bitcoin allocation can produce what it calls a “material outcome” from a non-material starting weight.

At press time; BTC traded at $69,935.