Author: Andjela Radmilac

Compiled by: Deep Tide TechFlow

Deep Tide TechFlow Introduction: ETFs only solve "how to buy Bitcoin," but few have noticed that Wall Street is already using it to do what U.S. Treasuries and gold have done for years: collateralizing loans, insurance reserves, and rating bonds. The liquidation wave in February proved this system can withstand pressure but also exposed the fatal flaw of a collective stampede in the leverage chain.

Everyone knows about ETFs, but almost no one knows that while ETFs are capturing all the attention, dozens of institutional products built around Bitcoin are quietly emerging—from a $40 million insurance reserve in Barbados to S&P-rated bonds being sold to Wall Street investors by Jefferies.

ETFs answered only one question: how ordinary investors and institutions can hold Bitcoin within a regulated wrapper. The products in this article answer a different, arguably more important question: once you own Bitcoin, what can you do with it?

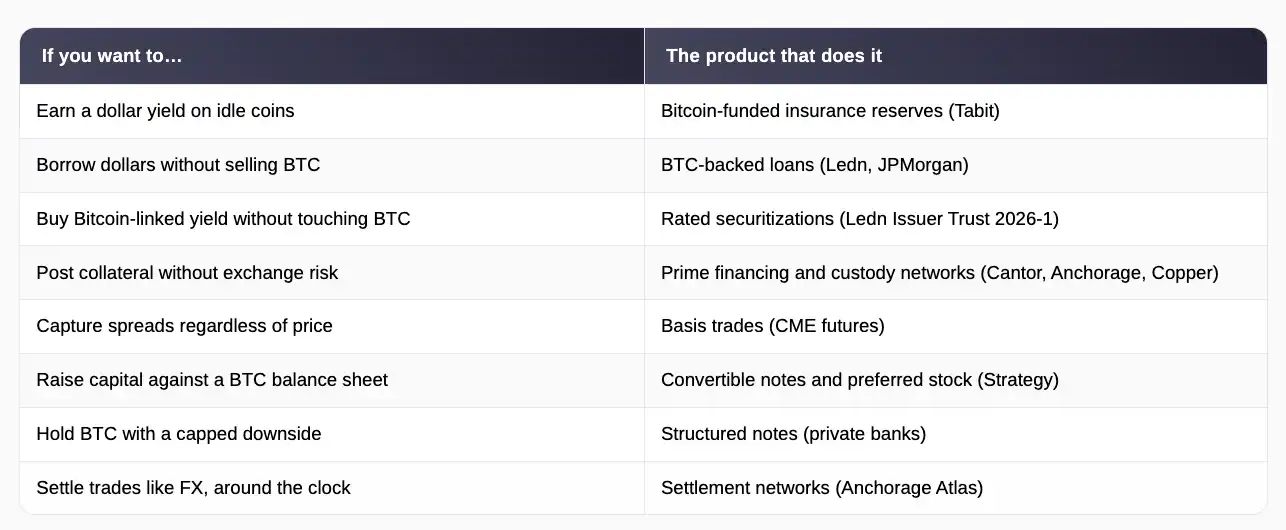

The answer: exactly what the financial industry has always done with U.S. Treasuries and gold. You can use it as collateral to borrow money, post it as margin for trades, backstop insurance policies as reserves, or build a corporate balance sheet on top of it.

Assets capable of doing all these things simultaneously are sometimes called financial primitives, a fancy term for "building blocks": things that are widely accepted and easily valued, upon which the rest of the financial system can stack loans, bonds, and derivatives. Treasuries earned this status because everyone agrees on their value and how to seize them if a trade goes wrong.

Bitcoin is now undergoing the same test. Early results explain why some of the biggest players in this market genuinely don't care whether the price goes up or down.

Insurance Reserves, Consumer Credit, and the First Rated Bitcoin Bond

In March 2025, Tabit Insurance, a Barbados-licensed insurer founded by former Bittrex executives, capitalized a property and casualty insurance entity with $40 million funded entirely by Bitcoin.

Essentially, Bitcoin holders surrendered their holdings to back real insurance policies covering storm damage and lawsuits against company directors. In return, they earned a near 10% dollar-denominated yield. Policies and premiums remained in dollars, so clients never touched cryptocurrency, while Bitcoin served as the reserve to pay claims if problems arose.

Tabit holds a Class 2 license from the Barbados Financial Services Commission and is structured as a segregated accounts company. This means each investor fund pool is legally isolated from others, so losses in one account don't drain capital from another.

Regulators and auditors can also check the reserves on the blockchain in real-time, providing more transparency than traditional insurers offer in their quarterly reports. CEO Stephen Stonberg noted that the entire global reinsurance industry runs on roughly $800 billion in capital, while Bitcoin is a multi-trillion-dollar asset class. Thus, even a small portion of this wealth flowing into underwriting would be felt across the entire industry.

While insurance reserves are indeed an unexpected use case for Bitcoin, lending is where things get serious. Bitcoin-collateralized loans work in a straightforward way: you pledge your coins to a lender, receive dollars, and when you repay, you get your coins back.

Holders do this because selling triggers taxable gains and ends their exposure to future price appreciation, while borrowing against coins gives them cash without relinquishing any holdings.

Transaction volume across platforms reached about $2 billion in 2025. Toronto-based Ledn alone reported issuing over $9.5 billion since 2018. Major banks like JPMorgan Chase have also launched similar products for their own clients.

In February 2026, this lending business entered the mainstream bond market. Ledn completed a $188 million securitization, meaning it bundled 5,441 loans into a pool and sold bonds whose interest payments come from borrower repayments.

The bonds were split into two tranches: $160 million in senior notes that get paid first, rated BBB- by S&P Global Ratings (an investment-grade rating, the first ever assigned to a digital asset-backed security), and $28 million in riskier subordinate notes rated B-, which absorb first losses in exchange for higher yields.

By crypto standards, the underlying numbers are conservative. The 2,914 U.S. borrowers in the pool owe $199.1 million but have pledged around 4,079 BTC, worth $356.9 million. This translates to a loan-to-value ratio of 55.8%, meaning they pledged nearly $2 worth of Bitcoin for every $1 borrowed.

Ledn CEO Adam Reeds stated that this structure creates a "direct pipeline" between Bitcoin holders seeking liquidity and the world's deepest pools of institutional capital. Bitwise's European Head of Research, Andre Dragosch, added that the deal proves traditional finance now views Bitcoin as legitimate, even pristine, collateral.

The structure was almost immediately stress-tested, revealing both the model's strength and its fragility. Bitcoin fell about 27% from mid-January to February 2026, pushing up the loan-to-value ratio across the pool and triggering margin calls—automatic demands for borrowers to either add more collateral or watch the lender sell it.

Ledn eventually liquidated roughly a quarter of the loans originally intended for the deal. The sale still went through, partly because these automatic liquidations worked exactly as designed, and Ledn never suffered a loss when selling collateral due to default.

The perverse consequence to remember: when many lenders run the same triggers on the same volatile asset, a sharp price drop forces them to sell simultaneously, and this selling further depresses the price, triggering more sales. The system passed its first real test, but it also revealed where it would break under sufficient stress.

Collateral Networks, Carry Trades, and Corporate Balance Sheets

Beneath these products, the market's fundamental mechanics are being rebuilt to resemble currency and bond markets more closely, where the entity holding your assets, the platform you trade on, and the system settling the trades are three separate things.

Anchorage Digital, which operates the only federally chartered crypto bank in the U.S., launched its Atlas settlement network in April 2024. This allows institutions to settle trades directly with each other without parking funds in custody accounts or pre-funding exchanges.

By March 2026, Atlas had connected nearly 600 participants, four times the number from a year earlier, processed hundreds of billions in settlements, and expanded to managing collateral. This means the bank now monitors loan positions, issues margin calls, and handles liquidations on behalf of lenders.

Cantor Fitzgerald chose Anchorage and Copper.co to play this role for its global Bitcoin financing business in March 2025. Copper's ClearLoop system lets trading firms lock their coins in custody while still trading across multiple exchanges, so a repeat of the FTX collapse wouldn't take client assets.

All of this makes posting Bitcoin as margin as routine and safe as posting Treasuries—a prerequisite for the expansion of everything else mentioned in this article.

A significant portion of the institutional capital flowing through these mechanisms has absolutely no view on Bitcoin's price. The basis trade has been one of the most popular institutional strategies since the ETF launch, exploiting the fact that Bitcoin futures typically trade slightly above the spot price: funds buy spot Bitcoin or ETF shares while simultaneously selling futures contracts at a higher price, profiting from the spread regardless of where the price goes next, as gains on one leg offset losses on the other.

After ETFs gave funds an easy way to hold the spot side, hedge funds built record short positions in CME futures, where open interest climbed from around 30,000 contracts in early 2024 to a peak near 45,000 in November of that year.

This trade became large enough that its unwinding can now move the market on its own. CME open interest fell below $10 billion in April 2026 as these paired positions closed, mechanically selling pressure and depressing prices regardless of anyone's sentiment.

CME continues to build for this crowd, adding 24/7 trading in May 2026 and launching Bitcoin volatility index futures in June, allowing institutions to bet on or hedge the severity of price swings rather than its direction.

Corporate treasuries take this idea the furthest. As of late May 2026, MicroStrategy holds 843,738 BTC. The company has issued $6.7 billion in convertible notes (bonds convertible to stock if the share price rises), plus $15.5 billion in preferred stock across five different instruments—securities paying fixed dividends that sit between debt and common stock—to fund its aggressive BTC purchases.

In 2025 alone, it raised $25.3 billion, making it the largest U.S. equity issuer that year, accounting for about 8% of all issuance. It markets its preferred securities as "digital credit," a full-fledged fixed-income product line whose dividends are ultimately serviced by the Bitcoin balance sheet.

Shareholders effectively get leveraged Bitcoin exposure through the stock; dividend investors get double-digit yields backed by the coins. From Tokyo-listed Metaplanet to Semler Scientific, imitators are copying Michael Saylor's risk playbook.

Private banks run parallel assembly lines for wealthy clients, packaging structured notes that cap the downside of Bitcoin exposure in exchange for giving up some upside, allowing conservative portfolios to hold an asset that would otherwise be too volatile for them.

This brings us full circle to the opening paradox.

ETFs answered how institutions can own Bitcoin. The products described in this article answer what they own it for. An asset that simultaneously capitalizes Caribbean reinsurers, backs investment-grade bonds, posts margin for CME derivatives, and services preferred stock dividends has moved far beyond speculative adoption and into the working machinery of finance.

Historians of this market may ultimately see ETFs as the visible first layer of institutionalization, while the lasting change happened in the plumbing of funding and settlement systems, where Bitcoin is doing the work Treasuries and gold have done for generations: serving as collateral upon which everything else is built.

The risks are real, as proven by the February liquidation wave, and they grow with leverage. But the direction seems set. Bitcoin's most important institutional role may never appear on a fund flows chart because it is becoming part of the machinery itself.