$200 million is the figure just announced today.

BitMine Immersion Technologies (BMNR), chaired by renowned Wall Street analyst Tom Lee, announced that it will invest in Beast Industries, the holding company behind global top streamer MrBeast. Meanwhile, Beast Industries mentioned in its official statement that the company will explore how to "integrate DeFi into the upcoming financial services platform" in the future.

If you only look at the news, it seems like another familiar crossover: traditional, crypto, internet celebrity, entrepreneurship. On one side is the YouTube霸主 with cumulative global subscriptions exceeding 400 million, whose single video can make the algorithm spontaneously weight you; on the other side is Wall Street's top analyst best at telling crypto narratives, skilled at writing grand blockchain concepts into balance sheets. Everything seems logical.

MrBeast's Journey

Looking back at MrBeast's early videos, it's hard to connect them with today's Beast Industries valued at $5 billion.

In 2017, Jimmy Donaldson, who had just graduated from high school, uploaded a video of himself counting continuously for 44 hours—"Challenge to count from 1 to 100,000!" The content was simple to the point of childishness, with no plot, no editing, just a person repeating numbers in front of the camera, yet it became a turning point in his content career.

At that time, he was not yet 19 years old, with only about 13,000 channel subscribers. After the video was released, it quickly exceeded a million views, becoming the first globally viral case.

Later, he recalled that time in an interview with one sentence:

"I didn't actually want to become famous at that time; I just wanted to know if the result would be different if I was willing to put all my time into something no one else was willing to do."

Jimmy Donaldson successfully built his account, becoming the later well-known MrBeast. But more importantly, from that moment on, he formed an almost obsessive belief: attention is not a gift of talent but something earned through investment and endurance.

Treating YouTube as a Company, Not a Creative Platform

Many creators choose to "conservatize" after becoming famous: reduce risks, improve efficiency, turn content into stable cash flow.

MrBeast chose the opposite path.

He repeatedly emphasized one thing in multiple interviews:

"The money I earn is basically spent on the next video."

This is the core of his business model.

By 2024, his main channel had over 460 million subscribers, with cumulative video views exceeding 100 billion. But behind this is extremely high costs:

· The production cost of a single top video is consistently between $3 million and $5 million;

· Some large challenges or public welfare projects can cost over $10 million;

· "Beast Games" on Amazon Prime Video, described by himself as "completely out of control," and he admitted in an interview: losses reached tens of millions of dollars.

When he said this, he did not show regret:

"At this level, you can't win while trying to save money."

This sentence can almost be used as the key to understanding Beast Industries.

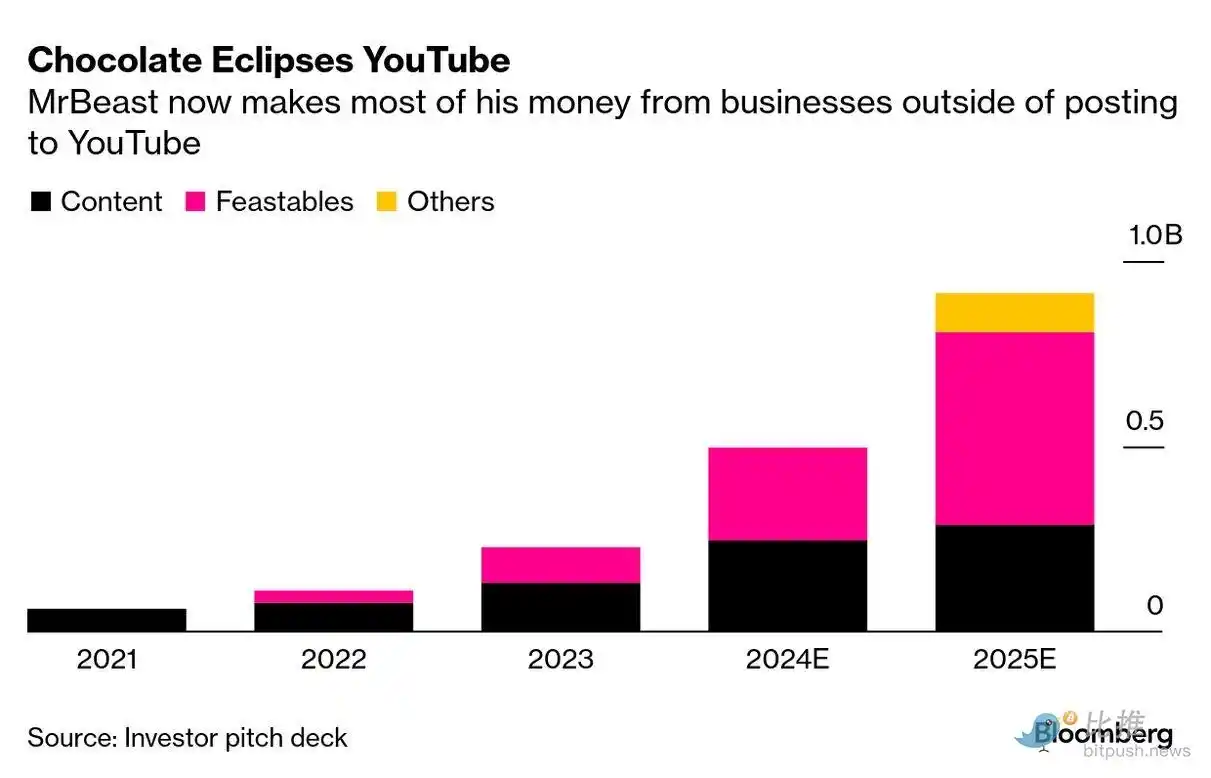

Beast Industries: Annual Revenue of $400 Million, but Thin Profits

By 2024, MrBeast consolidated all businesses under the name Beast Industries.

From public information, this company has far exceeded the scope of "creator side business":

· Annual revenue exceeds $400 million;

· Businesses span content production, fast-moving consumer goods retail, licensed merchandise, tool-based products;

· After the latest round of financing, the general expectation for its valuation is around $5 billion.

But it's not easy.

MrBeast's YouTube main channel and Beast Games bring huge exposure but almost consume all profits.

In stark contrast to the content is his chocolate brand Feastables. Public information shows that in 2024, Feastables sales were about $250 million, contributing over $20 million in profit. This is the first time Beast Industries has seen a stable, replicable cash flow business. By the end of 2025, Feastables had entered over 30,000 physical retail stores in North America (including Walmart, Target, 7-Eleven, etc.), covering the United States, Canada, and Mexico, greatly enhancing the brand's offline sales capabilities.

MrBeast has坦言 on multiple occasions that video production costs are getting higher and even "increasingly difficult to break even." But he still insists on investing heavily in content production because, in his view, this is not just paying for videos but buying traffic for the entire business ecosystem.

The core barrier of the chocolate business is not production but the ability to reach consumers. While other brands need to spend huge sums on advertising exposure, he only needs to release one video. Whether the video itself is profitable is no longer important; as long as Feastables can continue to sell, this business闭环 can continue to operate.

"I'm Actually Broke"

In early 2026, MrBeast revealed in a Wall Street Journal interview that he was broke, sparking discussion:

"I'm basically in a 'negative cash' state now. They all say I'm a billionaire, but there's not much money in my bank account."

This statement is not "humblebragging" but a natural result of his business model.

MrBeast's wealth is highly concentrated in unlisted equity; although he holds slightly over 50% of Beast Industries shares, the company continues to expand and almost pays no dividends; he personally甚至 deliberately does not retain cash.

In June 2025, he坦言 on social media that because he spent all his savings on video production, he even had to borrow money from his mother to pay for wedding expenses.

As he later explained more bluntly:

"I don't look at my bank account—it affects my decision-making."

And the tracks he invests in are no longer limited to content and consumer goods.

In fact, as early as the 2021 NFT热潮, on-chain records show that he had purchased and traded multiple CryptoPunks, some of which were sold for 120 ETH each (worth hundreds of thousands of dollars at the time).

However, as the market entered a correction period, his attitude became more cautious.

The real turning point is that the "MrBeast" business model itself has reached a critical edge.

When a person controls the world's top traffic入口 but is长期 in a state of high investment, cash紧张, expansion relying on financing, finance is no longer just an investment option but becomes infrastructure that must be重构.

The命题 repeatedly discussed within Beast Industries in recent years has gradually become clear: how to make users no longer just "watch content, buy goods" but enter a long-term, stable, sustainable economic relationship?

This is precisely the direction traditional internet platforms have been trying for years: payment, accounts, credit systems. And at this node, the appearance of Tom Lee and BitMine Immersion (BMNR) leads this path to a more structural possibility.

Partnering with Tom Lee to Build a DeFi Foundation

On Wall Street, Tom Lee has always played the role of a "narrative architect." From early explanations of Bitcoin's value logic to emphasizing the strategic significance of Ethereum in corporate balance sheets, he is good at translating technological trends into financial language. BMNR's investment in Beast Industries is not chasing internet celebrity热度 but betting on the programmable future of attention入口.

So, what exactly does DeFi mean here?

Currently, public information is extremely restrained: no token issuance, no profit promises, no fan-exclusive financial products. But the expression "integrating DeFi into the financial services platform" points to several possibilities:

- Lower-cost payment and settlement layer;

- Programmable account system for creators and fans;

- Asset recording and equity structure based on decentralized mechanisms.

The imagination space is large, but the real challenges are also clear. In the current market, whether native DeFi projects or traditional institutions exploring转型, most have not yet truly run a sustainable model. If they cannot find a differentiated path in this fierce competition, the complexity of financial business may反而 erode the core capital he has accumulated over the years: fan loyalty and trust. After all, he has repeatedly stated publicly:

"If one day what I do harms the audience, I would rather do nothing."

This sentence may be repeatedly tested in every future financialization attempt.

So, when the world's strongest attention machine starts seriously building financial infrastructure, will it become a new generation platform or a "too brave" crossover?

The answer will not be revealed soon.

But one thing he knows better than anyone: the greatest capital is not past glory but the right to "start over."

After all, he is only 27 years old.