On May 15, OpenAI launched a new feature that left many feeling "both excited and uneasy" — a ChatGPT personal finance tool. Simply put, you can now directly connect your bank accounts and investment accounts to ChatGPT.

This feature is currently available for preview only to ChatGPT Pro users (monthly fee $200) in the United States. OpenAI uses the financial data service Plaid to facilitate account connections, supporting over 12,000 financial institutions, including JPMorgan Chase, Fidelity, Charles Schwab, Robinhood, American Express, and Capital One.

It sounds great. But the comments section almost exploded — would you really dare to give your bank account to an AI?!

01

What Does Your "AI Personal CFO" Look Like?

First, let's see what this tool can actually do.

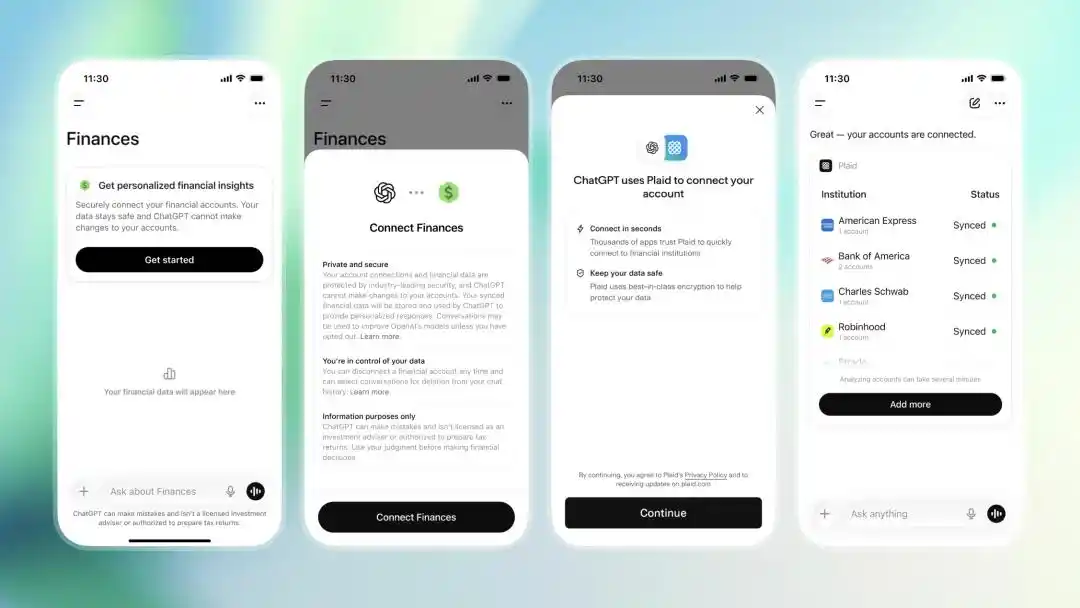

Users go to the "Finances" option in the ChatGPT sidebar, click start, or directly type "@Finances, connect my accounts" in the dialog box. ChatGPT will then guide you through connecting your bank accounts via Plaid. The entire authorization process is essentially the same as linking your bank card in apps like Venmo or Robinhood — Plaid's tokenized authentication mechanism means ChatGPT itself does not have access to your bank passwords.

You need to connect your bank account via Plaid first | Image source: OpenAI

Once connected, ChatGPT will take a few minutes to sync and categorize your financial data, then generate a visual financial dashboard. This dashboard covers comprehensive information: checking and savings account balances, transaction history, spending breakdown by category, monthly recurring subscription services, upcoming bills, payroll deposit records, investment portfolio performance, as well as liabilities like credit card debt and mortgages.

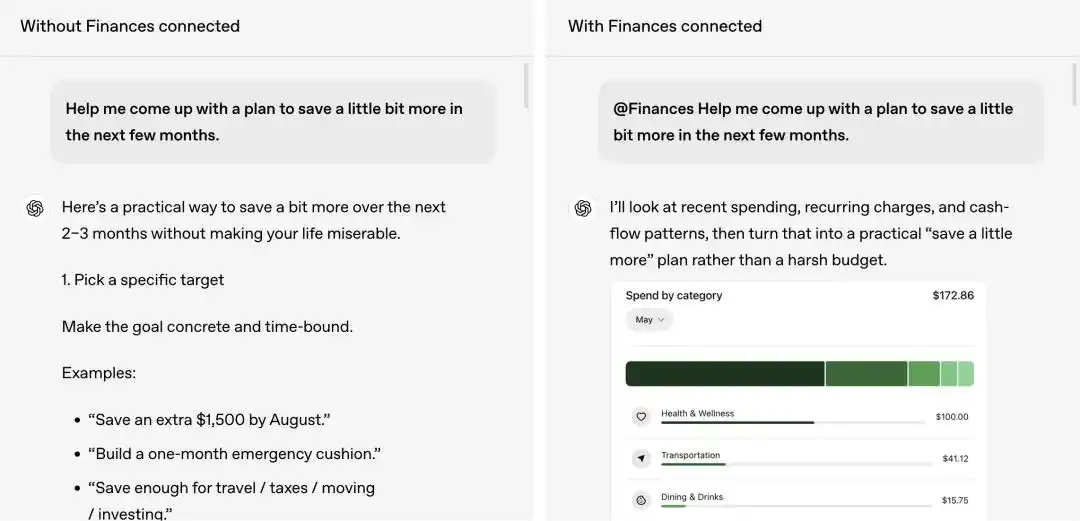

But the dashboard is just the starting point. The really interesting part is "conversational finance management." Unlike traditional budgeting tools like Mint or YNAB, ChatGPT doesn't require you to look at charts, browse categories, or manually set budgets. You simply ask questions in natural language, and it provides answers based on your actual data.

Comparison of financial questions before (left) and after (right) using personal financial data. Clearly, the latter is more planned and targeted | Image source: OpenAI

OpenAI provided several example scenarios: you can ask, "Am I spending more lately than before? What's changed?" ChatGPT will analyze your transaction history for spending trends.

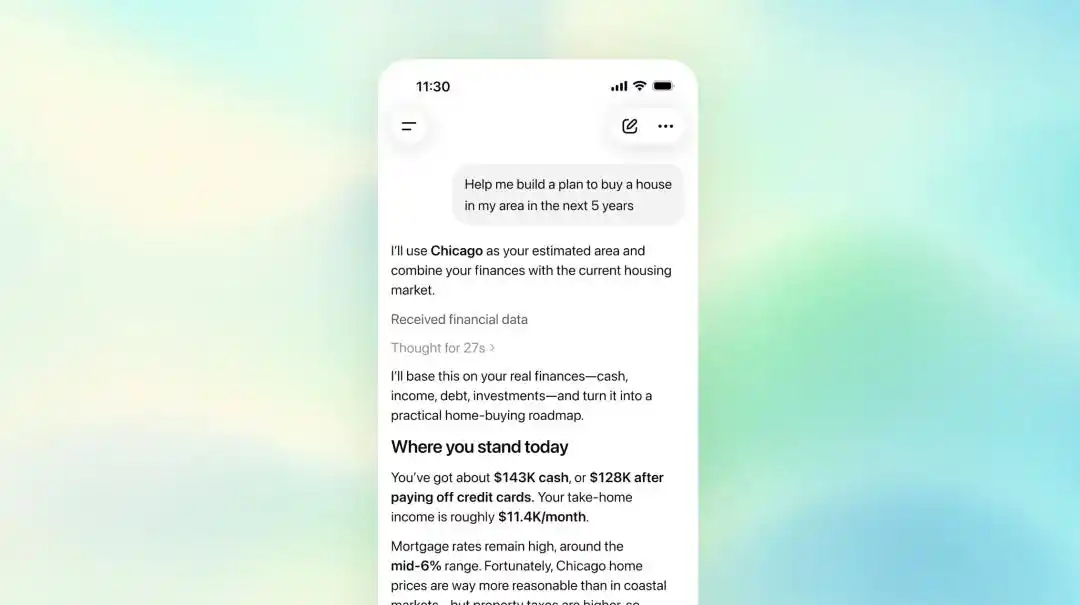

You can say, "Help me make a plan to buy a house locally within five years," and it will calculate based on your income, savings rate, and current liabilities; you can even tell it, "I still owe my parents some money" or "I plan to buy a car early next year." ChatGPT will store this information in its "financial memory," and subsequent conversations will consider this context.

This is completely different from ChatGPT's previous experience in answering financial questions. Before, if you asked it "How should I save money to buy a house?" you'd get a bunch of generic textbook financial advice. Now that it can see your bank account balance, monthly spending structure, investment returns, and debt ratio, the suggestions are no longer generic nonsense like "we recommend saving 20% of your salary each month."

OpenAI also hinted at the next step: soon supporting Intuit data integration, allowing users to have ChatGPT analyze the specific tax impact of selling a particular stock or assess their approval probability for a certain credit card application.

OpenAI wants to evolve ChatGPT from "helping you look up a concept" to "helping you make decisions."

02

Two Acquisitions, Three Strategic Moves

OpenAI didn't undertake this on a whim.

Its groundwork has actually been underway for over half a year. In October 2025, OpenAI acquired the personal finance app Roi, and its founder Sujith Vishwajith subsequently joined OpenAI.

In April 2026, OpenAI acquired another personal finance startup, Hiro Finance, with founder Ethan Bloch and the entire team joining. Hiro's positioning was "AI personal CFO" and had helped users manage over $1 billion in assets. Bloch previously founded the automated savings app Digit, which was acquired for over $200 million in 2021.

Two acquisitions, two fintech veterans, half a year — OpenAI is clearly building a "financial task force" in a planned manner.

The driving data behind this is also staggering. OpenAI revealed that over 200 million people ask financial-related questions on ChatGPT every month — from budget management to how to cut expenses. These users were already using a "general-purpose chatbot" for financial tasks, except previously ChatGPT's responses lacked personalized data support.

Users can directly conduct financial analysis within ChatGPT | Image source: OpenAI

Now, with Plaid's account connections and the stronger reasoning capabilities of the GPT-5.5 model, ChatGPT's goal is clear: to evolve from a "chat-about-anything" general assistant into a "super assistant" that truly understands your financial situation.

OpenAI has actually already tested this path before.

In January of this year, it launched ChatGPT Health, allowing users to connect medical records and health apps like Apple Health and MyFitnessPal. Official data shows over 230 million people ask health questions on ChatGPT weekly. From health to finance, OpenAI is shaping ChatGPT into an entry point covering all "high-value decision-making" scenarios in life.

03

Privacy Storm Arrives Faster Than the Product

But the problem is, managing money isn't like writing copy. What you're handing over isn't a prompt, but your entire financial profile.

Following the release of this feature, reactions on social media were overwhelmingly skeptical. Someone commented on Twitter: "What sane person would willingly give that level of access to OpenAI?" Others immediately brought up past issues: "You guys were just hit with a class-action lawsuit for secretly sharing ChatGPT conversation data with Google and Facebook."

This isn't baseless. Just one day before the finance feature launch, a new class-action lawsuit was filed in a California federal court, alleging that OpenAI embedded Meta Pixel and Google Analytics tracking codes in the ChatGPT webpage, transmitting chat topics, user IDs, email addresses, and other information to Meta and Google for ad targeting without user knowledge. The complaint points out that many users discuss extremely private topics like finance, health, and law on ChatGPT.

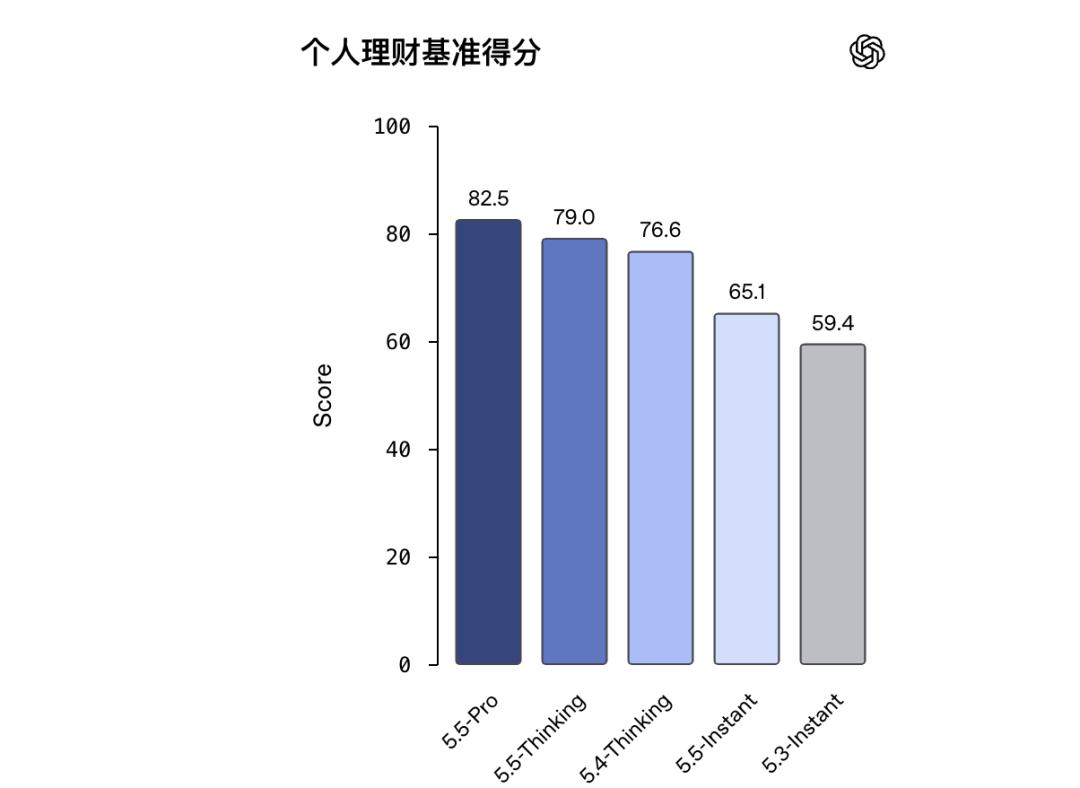

OpenAI officially stated that GPT-5.5 Pro performs better for private financial analysis | Image source: OpenAI

Getting sued for allegedly secretly sharing user chat data, then launching a new product that asks users to connect their bank accounts — this timing coincidence is almost a PR disaster-level coincidence.

OpenAI clearly recognizes the trust issue. It repeatedly emphasized in its announcement that ChatGPT cannot perform any actions on user accounts, nor can it see full account numbers; it can only read balances, transaction history, investment portfolios, and liability information. Upon disconnection, data will be deleted within 30 days. Users can also view and delete the financial "memories" ChatGPT retains.

But one detail is noteworthy — there is an optional switch in the system called "Improve the model for everyone." If users turn it on, their financial conversation data will be used to train the AI model. Although this switch is off by default, its very existence sends a signal:

Your financial data, within OpenAI's system, can theoretically become training material.

04

AI Companies Collectively Rush Towards "High-Value Data"

Viewing ChatGPT's financial tool within a broader context reveals a collective shift in the AI industry.

The era of general-purpose chatbots is ending; the war for "vertical super assistants" has begun.

OpenAI launched health in January and finance in May; Anthropic released ten professional AI Agents for the financial industry in early May, directly targeting banking, insurance, and asset management, with data sources including Moody's, S&P Capital IQ, and Morningstar — news that caused FactSet's stock to drop 8% that day. Perplexity also launched "Computer for Professional Finance" around the same time, targeting professional investment research teams, supporting connections to data sources like PitchBook and Daloopa, and offering 35 preset financial workflows.

Interestingly, Perplexity's financial product recently also started supporting user connections to brokerage accounts via Plaid — using the same infrastructure as ChatGPT. This means Plaid is becoming the underlying pipeline for the "AI finance management" era, much like Stripe for online payments.

But the strategic differences between companies are also evident. OpenAI is taking a consumer (C) route, aiming to bring every ordinary person's bank account into ChatGPT. Anthropic and Perplexity are taking a business (B) route, aiming to let financial professionals use AI to replace some functions of Bloomberg Terminal.

However, whether B or C, the core logic is the same: whoever gains access to users' most private, highest-value data occupies the entry point in the next phase of AI.

Health data, financial data, legal data — these fields are being collectively targeted by AI companies not because AI suddenly became good at finance, but because these scenarios naturally require personalization, inherently involve high-frequency interaction, and naturally have a willingness to pay.

05

The Ultimate Test for the "Super Assistant"

Returning to ChatGPT's launch. From a product logic perspective, it's actually quite well done: using Plaid connections ensures a baseline of security, read-only permissions rather than operational permissions reduce risk, and the 30-day data deletion provides an exit mechanism. OpenAI also stated it will soon support Intuit connections, allowing users to analyze the tax impact of stock sales or assess credit card approval probabilities.

But there is a chasm between a well-made product and user trust.

Sam Altman wants to turn ChatGPT into a "personal super assistant," covering every aspect of life from writing to search, from health to finance, from programming to shopping. This vision is undeniably grand. But the grander the vision, the higher the demand for trust. And OpenAI's track record on privacy issues doesn't inspire complete confidence.

A comment on Slashdot was quite direct: "Hand over your bank account to a hallucinating chatbot? Since when can AI's financial advice be written into the disclaimer?"

This is harsh but touches the core issue. There's a fundamental difference between AI financial tools and traditional financial advisors — human financial advisors are subject to financial regulation, have licenses, and bear legal responsibility; ChatGPT's terms of service clearly state it does not provide investment advice and bears no financial consequences.

When a tool looks like a financial advisor, talks like a financial advisor, and even understands your spending data better than most advisors — yet legally, it is nothing of the sort — this itself is a gray area that needs serious discussion.

OpenAI says it will first gather feedback from Pro users before deciding whether to open it up to Plus users. This is a smart strategy — using the most adventurous hardcore users to "beta test." But if the trust issue isn't resolved, the larger user base might never see it.

Technically, ChatGPT is ready to manage your money.

But are you ready? This might be an unavoidable choice for everyone in the AI era.

Geek's Question

Would you be willing to connect your bank account to an AI chatbot? Why or why not?

This article is from the WeChat public account "GeekPark" (ID: geekpark), author: Huà Lín Wǔ Wáng