Author: Climber, CryptoPulse Labs

According to the latest SEC filing, SpaceX plans to issue approximately 556 million shares at $135 per share, raising $75 billion, corresponding to a valuation of approximately $1.77 trillion. At the same time, SpaceX is integrating rockets, Starlink, AI, orbital data centers, and the future space economy into a super-narrative.

For the crypto market, what is truly worth paying attention to is not the "space concept," but rather the shift in capital valuation logic. When capital begins to reallocate assets around AI, infrastructure, and future ecosystems, which directions in the crypto market will receive a spillover effect from this capital?

So, which crypto sectors could become the core of the next cycle? This article explores the possible industry cycle development logic based on this historic largest IPO event.

I. The AI Narrative Enters Its Second Half: The Market Begins to Compete for "The Shovel Sellers"

Over the past year, the main narrative around AI in the crypto market has undergone two changes.

In the first stage, the market traded AI applications. After the explosion of ChatGPT, a large number of AI Agent, AI assistant, AI social, and AI content projects began to attract market attention.

The logic of this stage was very simple: whoever was closer to the end user was easier to value. But problems soon emerged. The barrier to entry for AI applications themselves was rapidly decreasing.

After a new AI application emerged, it could easily be replicated. After model upgrades, many applications could even be directly replaced. The market then began to realize that what is truly scarce in AI is not the application layer, but the underlying means of production.

SpaceX's IPO actually reinforces this logic.

On the surface, SpaceX sells rockets, but the prospectus materials and roadshows repeatedly emphasize AI, computing power networks, and future data centers.

Goldman Sachs expects SpaceX's AI revenue to grow 100-fold by 2030, essentially betting on future AI infrastructure. Mapping this logic to the crypto market means capital may further migrate towards underlying AI protocols.

The first is computing power. Currently, one of the biggest limiting factors in the AI industry is not the models, but GPU resources.

From OpenAI to xAI, from Anthropic to Google, everyone is competing for high-performance computing resources. Even the continuous rise in Nvidia's market cap essentially reflects the market's revaluation of computing resources.

A similar type of asset exists in the crypto world, such as TAO. Many have simplistically understood TAO as an AI-themed coin, but it is actually closer to an AI network-layer protocol. It attempts to use token incentives to create an open network of model, computing power, and data contributors.

If the market continues to strengthen the AI infrastructure logic in the future, TAO's valuation framework may further shift towards "AI network infrastructure" rather than an ordinary application project.

Next are GPU computing power networks. For example, projects like RENDER, AKT, and IO have long been understood as computing power rental platforms, but they may need to be reinterpreted in the future. They are not selling GPUs, but the liquidity of future computing capacity.

The most profitable entity in the internet era was not necessarily websites, but AWS. In the AI era, the most profitable might not be Agents, but computing networks.

A change may occur in the next cycle. In the past, the search was for which AI product would explode. In the future, the search may be for who is selling computing power.

The valuation systems for these two logics are completely different. The former relies on user growth, while the latter relies on the value of infrastructure, which typically has a longer cycle.

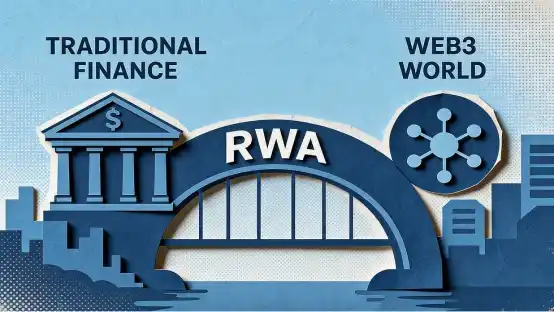

II. When Trillion-Dollar Assets Begin to Go On-Chain: RWA May See Its Real Breakout Point

Behind the $75 billion fundraising size, there is another question worth noting: why can SpaceX obtain a $1.77 trillion valuation?

Because the market believes in the future.

But the practical issue is that a large number of ordinary investors actually cannot participate in the early stages of these future assets. This is true for OpenAI, SpaceX, and many AI unicorns.

This means there may be a huge future demand: how can global capital participate in future assets earlier and more efficiently? The crypto industry is attempting to solve this problem.

In the past, RWA (Real World Assets) mainly revolved around government bonds for a simple reason: bonds have low risk, simple structures, and are easy to bring on-chain. But the future development direction of RWA may not just be bonds, but equity assets, stock assets, and even unlisted assets.

If more SpaceX-type assets partially enter the on-chain market in the future, it means the logic of asset trading may change.

In the past, there was a huge disconnect between the primary and secondary markets. Ordinary investors struggled to participate in early-stage quality assets. But if assets begin to be tokenized, this boundary may be broken.

New models of asset circulation may emerge, such as on-chain asset issuance, on-chain asset trading, on-chain asset settlement, forming a global 24/7 liquidity network.

This change could be bigger than DeFi because DeFi redefines financial instruments, while RWA may redefine the assets themselves.

Therefore, from a project perspective, the first to benefit may not be asset projects, but infrastructure projects. ONDO may benefit from the expansion of asset issuance, LINK may benefit from the growing demand for asset data, and RWA networks like Plume may benefit from the increasing demand for asset liquidity.

In the past, the market traded tokens. In the future, it may begin to trade assets. And whoever masters the asset circulation network masters the value gateway.

III. Stablecoins, Payments, and DePIN: A New Underlying Logic Is Forming

If AI and RWA still belong to the growth logic, another possible main beneficiary line is the infrastructure logic.

The most easily overlooked point about SpaceX is that rockets are not its true core; what is truly valuable is Starlink.

Because Starlink is essentially not a hardware business, but a network business.

Networks typically have greater long-term value than products because products can be replaced, but once a network reaches scale, it creates barriers.

A similar situation exists in the crypto market.

In the future, whether it's AI, RWA, or the development of on-chain securities, they will all ultimately require underlying settlement capabilities. Therefore, stablecoins may become one of the real big winners of the next cycle.

In the past, stablecoins were more understood as a medium of exchange. But in recent years, stablecoins have gradually evolved into financial infrastructure.

Cross-border payments need stablecoins.

On-chain securities need stablecoins. AI economic systems need stablecoins. Global asset circulation also needs stablecoins. This means the demand for stablecoins may no longer come from within the crypto market, but from the real world.

Simultaneously, payment protocols may also enter a stage of value revaluation. Many payment projects have long been undervalued by the market because payments seem to grow slowly.

But if the scale of the on-chain economy continues to expand in the future, the payment network itself could become a super gateway.

In addition, DePIN is also worth paying attention to.

In the past, the market mostly understood DePIN as a concept. But SpaceX actually proves one thing: real-world infrastructure can obtain extremely high valuations.

DePIN similarly attempts to use token incentives to build real-world networks—wireless networks, mapping systems, storage networks, computing networks—all essentially follow this logic.

If the market begins to reprice real-world infrastructure in the future, then DePIN may undergo a new value revaluation.

Because in the future, the most valuable thing may not be the application, but the network itself. This was true in the internet era, true in the mobile internet era, and may still be true in the AI era.

Conclusion

SpaceX appears to be an IPO event, but what it truly reflects is the new capital allocation path in the financial markets. The first stage is capital chasing stories, the second stage is capital chasing infrastructure, and the third stage is capital chasing cash flow.

Over the past few years, the crypto market has mostly remained in the first stage. In the coming years, capital may gradually enter the latter two stages. AI infrastructure, RWA, on-chain securities, stablecoins, payment networks, and DePIN may not rise the fastest in the short term, but they may be closer to the true underlying logic of the next cycle.

Because in every technological revolution, the ultimate biggest winners are often not the hottest applications, but those who build the underlying systems.