Author:CoinFound

Stablecoins are evolving from trading tools into global financial infrastructure.

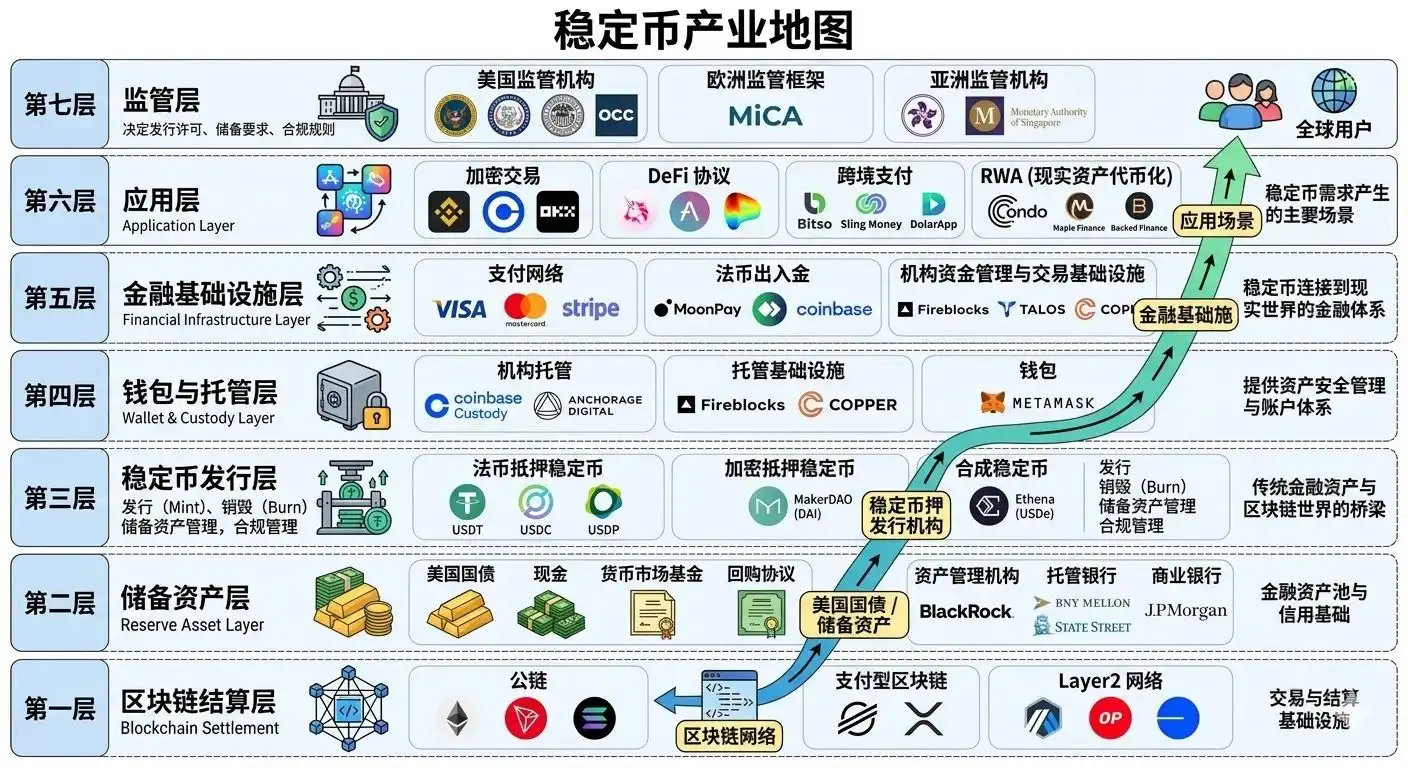

For a long time, the market's understanding of stablecoins was largely confined to their role as a "cryptocurrency trading medium": they were used for exchange quotations, served as on-chain hedging tools, or acted as basic liquidity assets within the DeFi system. However, entering 2026, this narrative is being rapidly rewritten. The functional boundaries of stablecoins have expanded from "auxiliary trading assets" to payments, settlements, collateral, yield generation, cross-border clearing, and even RWA settlement layers, gradually evolving into a key piece of infrastructure within the global digital financial system.

CoinFound's latest research, "Stablecoin Ecosystem Map — From Trading Tool to Global Financial Infrastructure," points out that the stablecoin market is entering a new phase characterized by "high mainstream adoption and high institutionalization." Its significance is no longer limited to price stability or on-chain circulation efficiency, but lies in its ability, through programmability, global settlement capabilities, and multi-chain liquidity networks, to become a crucial bridge connecting traditional finance with the decentralized ecosystem.

Stablecoin Market Has Entered a Trillion-Dollar Normalization Cycle

In 2026, the total market capitalization of the global stablecoin market has exceeded $310 billion, with annual trading volume reaching $33 trillion. This figure alone is sufficient to demonstrate that the practical application scenarios of stablecoins have long surpassed internal circulation within cryptocurrency exchanges and are extending into the broader real economy and global fund clearing networks.

From a market evolution logic perspective, stablecoins are no longer just "dollar substitutes" on-chain but are taking on a deeper infrastructure function:

They are both a carrier for cross-border value transfer and an underlying liquidity engine for the DeFi and RWA systems, while also being gradually embedded into payment gateways, corporate treasury management systems, and the backend clearing structures of social networks.

Particularly noteworthy is the significant growth in the Asian market. The market capitalization of stablecoins on BNB Chain achieved a 133% year-on-year expansion in the past year. This trend indicates that the stablecoin ecosystem is not only deepening its integration within the European and American financial systems but is also forming new regional payment and clearing networks in the Asian market.

Three Macro Drivers Jointly Propel Stablecoin Acceleration

The underlying logic driving the rapid upgrade of the stablecoin ecosystem comes mainly from three aspects:

First, Regulatory Clarity.

Major jurisdictions worldwide are gradually establishing compliant frameworks for stablecoins. Clear regulations not only reduce policy uncertainty but also provide the prerequisite for large-scale institutional capital entry. In the past, many traditional financial institutions were cautious about stablecoins not because they disapproved of their efficiency, but due to the lack of a clear legal framework. Now, this obstacle is being gradually removed.

Second, Sustained Inflow of Institutional Capital.

As regulatory boundaries become clearer, investments from VCs, asset management institutions, and traditional financial companies into stablecoins and their related payment infrastructure continue to expand. According to data in the article, this sector has cumulatively absorbed $7.9 billion in institutional funding, with VC investment showing an annualized growth rate of 44%. This means the stablecoin track is no longer just a battlefield for Crypto Native entrepreneurs but is becoming a core direction for active allocation by traditional capital.

Third, Geoeconomics and Global Clearing Demand.

Complex international environments, cross-border payment frictions, and the normalization of traditional financial sanctions have objectively increased the demand for alternative clearing networks. The borderless liquidity and 24/7 settlement capabilities inherent to stablecoins give them a natural advantage in this trend. Phenomena like capital migration in extreme scenarios also validate the real demand for stablecoins as a global liquidity network.

Global Regulatory Frameworks Are Reshaping Industry Boundaries

Entering 2026, the regulatory environment for stablecoins is moving from localized pilots to systematic implementation.

In the United States, a federal-level framework is taking shape, focusing on 1:1 high-liquidity asset reserves, strict auditing, and inclusion under national bank supervision. Simultaneously, the debate over "whether yield-bearing stablecoins should pay interest" has become a key watershed for industry development.

This debate essentially questions whether stablecoins should be treated as "payment tools" or could evolve into "shadow deposits" or deposit-like financial products.

The EU's MiCA has been fully implemented, imposing strict constraints on stablecoin reserve segregation, whitepaper disclosure, and interest payments, reflecting a highly cautious regulatory logic.

Hong Kong is accelerating the layout of its local stablecoin licensing system, emphasizing local registration, 100% cash or US Treasury backing, and attempting to seize the institutional high ground as an Asian hub for RWA and digital finance.

The UK is also promoting regulatory integration for "systemically important stablecoins," bringing them into the traditional financial services act system.

This means the global stablecoin ecosystem is no longer in a "regulatory vacuum" but is forming a clear policy map.

This map, on one hand, boosts institutional confidence, and on the other, imposes higher requirements on yield-bearing stablecoins, DeFi protocols, and RWA product structures. Future competition will not only be about technology and scale but also about compliance capability, product segregation capability, and policy adaptation capability.

Market Structure Diverges: USDT and USDC Maintain Dominance, Yield and RWA Rise Rapidly

In terms of competitive landscape, the stablecoin market shows clear signs of top-heavy concentration and structural divergence.

Tether (USDT) still maintains a dominant position with a market share of approximately 58%, having built a deep liquidity moat in offshore trade and emerging markets.

Circle (USDC), leveraging its compliant image, institutional channels, and Ethereum ecosystem advantages, continues to increase its share in regulated markets, with its market share rising by about 7%.

Meanwhile, competition among issuers is no longer limited to "whose stablecoin is bigger" but has extended to capital efficiency, yield generation capability, and underlying collateral structure:

-

Tether is challenging the institutional market through more compliant product structures;

-

Besides USDC, Circle is also enhancing its appeal to institutions through yield-bearing and tokenized fund products;

-

Tokenized treasury products like BlackRock's BUIDL are becoming an important component of the underlying interest-bearing collateral for various DeFi protocols and stablecoins.

This change signifies that stablecoin competition has escalated from "payment tool competition" to "financial infrastructure competition." Those who can provide higher capital efficiency, stronger compliance, and deeper institutional synergy will be more likely to lead the next phase of ecosystem evolution.

Sub-sectors: Payments, DeFi, Institutional Settlement, RWA All Accelerating

From an application perspective, the current stablecoin ecosystem exhibits several distinct growth directions.

1. Cross-border Payments and Remittances

Payments and remittances remain one of the core real-world use cases.

Especially in B2B scenarios, stablecoins have become an important tool for restructuring cross-border payment efficiency. Compared to the multi-layer correspondent bank clearing in traditional financial systems, stablecoins offer obvious advantages in cross-timezone, low-cost, 24/7 settlement.

2. DeFi Lending and Yield Generation

Stablecoins have evolved into benchmark interest rate assets in DeFi.

The rise of yield-bearing stablecoins means they are no longer just safe-haven assets but also capital management tools兼具 (jùbèi - possessing both) payment and yield attributes. This change is highly attractive to both users and institutions and has been a major reason for the market's rapid growth in recent years.

3. Institutional Settlement and Backend Clearing

Traditional payment networks are gradually introducing blockchain backends.

The penetration of stablecoins in institutional settlement means they are not just on-chain assets but are progressively becoming the "invisible clearing layer" behind traditional payment systems.

4. RWA Tokenization and Underlying Liquidity Integration

RWA is one of the most noteworthy long-term trends currently.

As traditional financial assets are gradually tokenized, stablecoins or similar yield-bearing products will increasingly assume the role of the cash leg and collateral asset in transactions.

The combination of stablecoins and RWA is expanding the on-chain world from speculative finance to the more real and vast traditional capital markets.

Risks Persist, But the Market Shows Anti-Fragility

Although the stablecoin market is entering a mature phase, underlying risks have not disappeared.

The article broadly categorizes the risks into three types:

-

Operational and Technical Risks: Smart contract vulnerabilities and cross-chain bridge attacks remain major concerns

-

Market and Liquidity Risks: DeFi leverage models and volatility of underlying collateral assets could trigger de-pegging pressure

-

Geopolitical and Scrutiny Risks: The use of offshore stablecoin networks in global capital flows may further trigger AML and compliance regulatory upgrades

Additionally, yield bans are creating new compliance friction for DeFi protocols; and the scaled expansion of RWA highly depends on legal配套设施 (pèitào shèshī - supporting facilities) like offline title confirmation and bankruptcy remoteness.

However, it is noteworthy that the market has not lost resilience because of these risks. On the contrary, after experiencing periodic volatility, the stablecoin ecosystem has demonstrated极强的 (jí qiáng - extremely strong) self-healing capabilities. After short-term deleveraging and sentiment shocks, capital flows back, indicating that the market's long-term judgment of the value of stablecoin infrastructure has not wavered.

Stablecoins Are Forming a Full-Chain Closed-Loop Ecosystem

From an industry chain perspective, stablecoins are no longer an isolated asset but have formed a complete closed loop from upstream to downstream:

-

Upstream: Reserve assets, government bonds, regulated RWA

-

Midstream: Issuance, custody, cross-chain routing, multi-chain liquidity networks

-

Downstream: Payments, settlement, DeFi, RWA, social payments, AI-driven scenarios

This full-chain closed loop意味着 (yìwèizhe - means that) stablecoins are upgrading from a single financial product to an extensible, composable, embeddable global value transfer network.

Future innovation directions worth focusing on include:

-

Stablecoin payment integration within social platforms

-

Compliant stablecoins pegged to regional fiat currencies

-

AI Agents-driven machine-to-machine payments

-

Lower-barrier fiat on-ramps and account abstraction technology

These trends indicate that the future of stablecoins is not just "more people holding them" but "more systems adopting them as the default payment and clearing layer."

Conclusion: From On-Chain Dollars to Global Financial Rails

The stablecoin industry is undergoing a fundamental identity transformation.

It is no longer just a convenient tool in the Crypto market but is evolving into a global financial infrastructure covering payments, clearing, yield, collateral, and asset settlement.

From regulatory clarity to institutional entry; from solidified top-tier格局 (gèjú - landscape) to the rise of RWA and yield-bearing products; from expanded payment scenarios to integration with social networks and AI protocols, the next phase of the stablecoin ecosystem will clearly not be about point breakthroughs, but systematic evolution.

For investment institutions, fintech companies, policymakers, and Web3 builders, understanding stablecoins is no longer just about understanding one sector, but about understanding the underlying architecture of the future digital financial world.