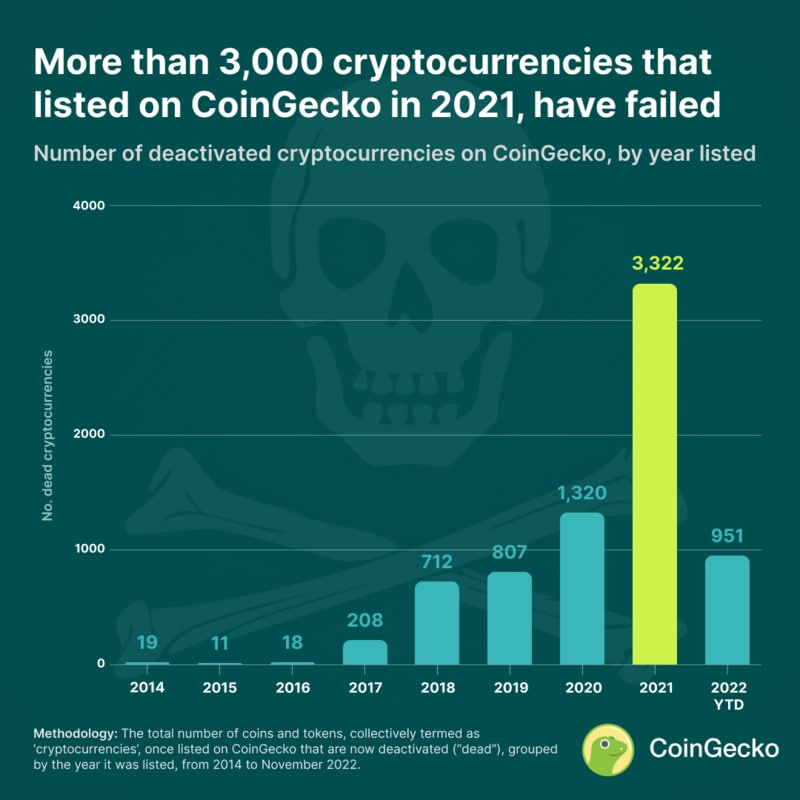

Новое исследование показало количество криптовалют, которые не оправдали ожиданий после выхода на рынок в 2022 году на фоне преобладающего медвежьего рынка. В частности, по данным CoinGecko, 951 монета была признана «мёртвой» или «потерпевшей неудачу» в 2022 году.

⠀

Определяя «мертвые» монеты, авторы исследования отметили, что рассматривались криптовалюты, которые могли быть удалены с сайта CoinGecko из-за недостатка торговой активности в течение последних двух месяцев. Проекты также признавались мертвыми после того, как их посчитали мошенничеством или создатели запросили деактивацию.

⠀

«Последняя волна бычьего рынка, начавшаяся в ноябре 2020 года, привела к резкому росту числа криптовалют, зарегистрированных на бирже, и в 2021 году на бирже было зарегистрировано более 8000 криптовалют. На сегодняшний день почти 40% были деактивированы и исключены из списка CoinGecko», — говорится в исследовании.

⠀

Диаграмма количества «мертвых» монет. Источник: CoinGecko

⠀

Согласно исследованию, количество мертвых монет в 2022 году значительно снизилось по сравнению с показателем 2021 года – 3 322. Примечательно, что за последние девять лет в 2021 году было зарегистрировано наибольшее количество мертвых монет на фоне преобладающего бычьего рынка.

⠀

Наплыв мемных монет

⠀

В исследовании отмечается, что такая разница может объясняться притоком на рынок «мемных» монет в 2021 году. При этом, большинство из них не имели значительной ценности, а анонимные разработчики наряду с этим нуждались в более значительных обязательствах по их развитию.

⠀

После успеха мемных монет, таких как Dogecoin (DOGE) и Shiba Inu (SHIB), многие попытались повторить этот успех. Интересно, что исследователи отметили, что без учета аномального роста в 2021 году, в период с 2018 по 2022 год количество мертвых монет в среднем составляло 947.

⠀

В целом, сторонники криптовалют утверждают, что по мере созревания сектора количество мертвых монет должно увеличиваться. По общему мнению, когда отрасль достигнет зрелости, активы с минимальной полезностью, скорее всего, исчезнут.

Paul L. для Finbold