Ноябрь стал поворотным моментом для крипторынка, и мемкоины оказались одним из самых успешных его секторов.

Редакция BeInCrypto составила список мемкоинов, от которых можно ждать приятных сюрпризов в декабре 2024 года.

Department of Government Efficiency (DOGE(GOV))

В ноябре DOGE(GOV) достиг исторического максимума в $0,545 благодаря повышенному интересу к президентским выборам в США. Ажиотаж вокруг политической ситуации создал сильный импульс для мемкоина. Однако учитывая возвращение Дональда Трампа на президентский пост и объявление о создании Департамента эффективности правительства под руководством Илона Маска, ралли DOGE(GOV) может продолжиться и в декабре.

Учитывая быстрый рост DOGE(GOV), достижение отметки $1 в следующем месяце выглядит вполне вероятным.

Bonk (BONK)

В начале ноября цена BONK достигла исторического максимума $0,00006230, но затем снизилась до $0,00004607. Однако несмотря на падение, у мемкоина есть значительный потенциал для дальнейшего роста, поскольку ажиотаж вокруг экосистемы Solana продолжает расти.

На момент написания BONK торгуется под важным сопротивлением на уровне $0,00004736. Удачный прорыв и закрепление выше него поможет мем-монете установить новый исторический максимум.

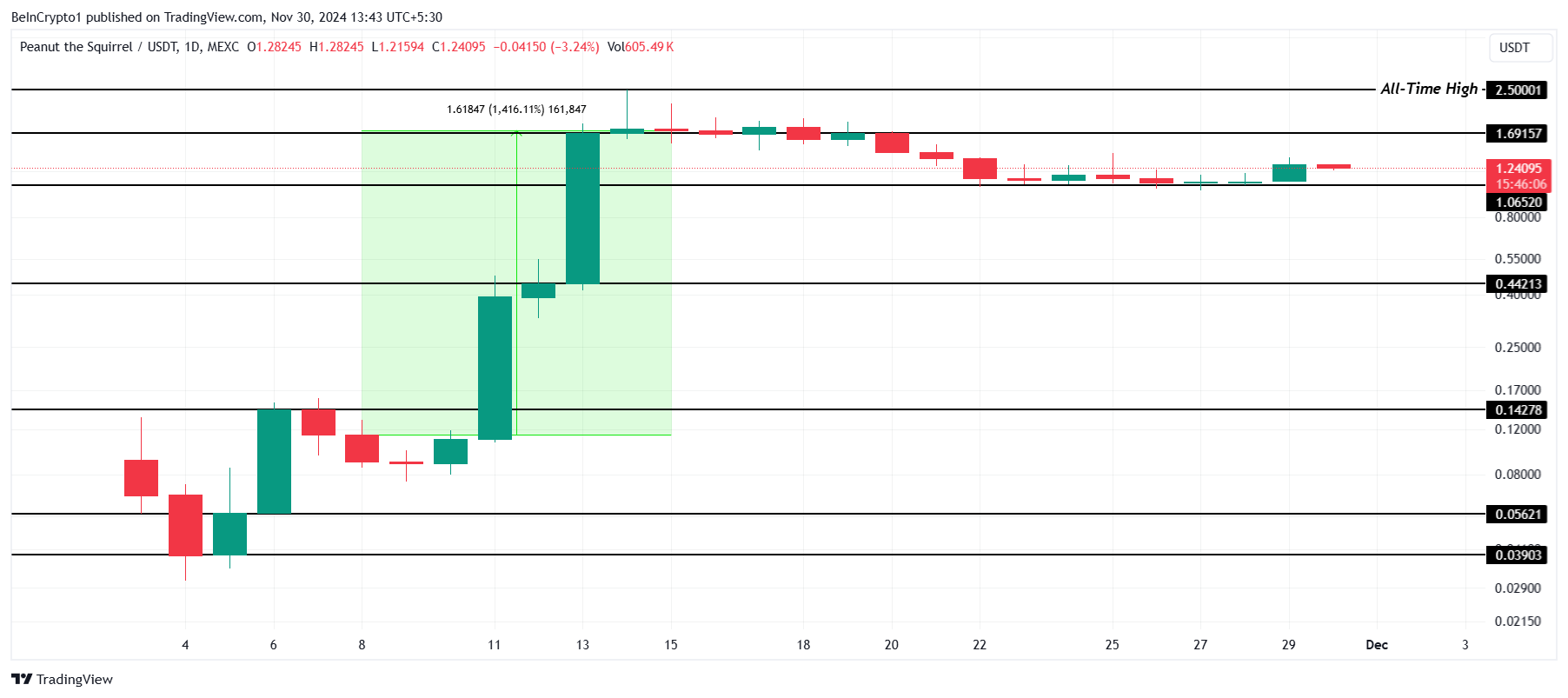

Peanut the Squirrel (PNUT)

PNUT стал одним из лучших криптоактивов в этом месяце, прибавив в цене 1 416% всего за неделю. На момент написания мемкоин торгуется у отметки $1,24, удерживаясь выше важной поддержки на уровне $1,06. Пока цена находится выше этого порога, PNUT, скорее всего, избежит значительного падения и сохранит восходящий импульс.

Однако если эта поддержка не устоит, мемкоин может ждать коррекция до $0,44.

Act 1: The AI Prophecy (ACT)

ACT находится на пересечении двух быстро развивающихся секторов криптовалютного рынка — искусственного интеллекта и мемкоинов. Это уникальное сочетание дает токену особое преимущество и привлекает новых инвесторов.

В начале ноября альткоин вырос на 3 044% всего за неделю. Если ACT успешно преодолеет исторический максимум в $0,95 и закрепился выше его, токен ждет продолжение ралли.

Однако фиксация прибыли может спровоцировать падение ниже критической поддержки в $0,44, что аннулирует текущий бычий прогноз.

Pepe (PEPE)

PEPE неожиданно вырос в ноябре, прибавив в цене почти на 84% всего за 48 часов и достигнув исторического максимума в $0,00002597. На момент написания мемкоин торгуется в районе $0,00002091, удерживаясь выше критического для сохранения бычьего импульса уровня $0,00001677. Его потеря опровергнет позитивный прогноз и спровоцирует очередную коррекцию.