此次更新是在 Hamster Kombat 玩家数量突破 3 亿并预告将推出“加密货币历史上最大规模空投”一周后发布的。

基于 Telegram 的手机点击游戏 Hamster Kombat 发布了有关其备受期待的加密货币空投的更多细节。

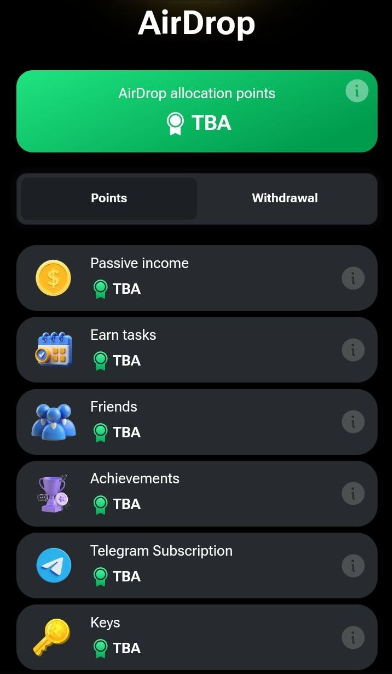

这款热门的点击赚钱游戏公布了更多有关玩家如何获得更大空投的细节。小程序终于在其 Telegram 小程序的空投部分添加了新细节。

HMSTR 空投标签。来源:Hamster Kombat

根据 Hamster Kombat 8 月 8 日更新的新空投部分,所有游戏内活动都将计入积累更多空投点数。更新后的部分包括六个不同的代币累积部分,包括玩家的被动收入和完成赚钱任务、成就、电报订阅和密钥以及朋友推荐。

玩家将根据游戏内不同的积分分配指标获得代币奖励。

不过,Hamster Kombat 发言人告诉 Cointelegraph,空投资格还取决于游戏周期、社区互动、整体社交活动和受邀玩家的质量:

“游戏中的玩家越多,资本化程度就越高,因此每个人的回报就越大。即将到来的 HMSTR 空投将成为加密货币历史上规模最大的一次。而且我们没有任何风险投资人。获得代币的唯一方法就是玩游戏。”

这项备受期待的更新是在 Hamster Kombat玩家数量达到 3 亿后一周发布的 ,并预告即将推出“加密货币历史上最大规模的空投”。

Hamster Kombat 旨在吸引下一个十亿 Web3 用户

Hamster Kombat 的最终目标是吸引下一个十亿主流用户加入 Web3。

当被问及游戏的最终目标时,Hamster Kombat 的发言人告诉 Cointelegraph:

“我们希望建立最大、最紧密的社区,并让下一个十亿人加入 Web3,所以我们必须向所有人展示 Web3 的实际运作方式。最简单的方法就是通过游戏。”

该发言人补充说,Hamster Kombat 的便利性无缝地向用户介绍了底层区块链技术和加密货币,而没有额外的摩擦点,使该游戏成为吸引新 Web3 用户的绝佳工具。

其他人也相信 Telegram 的主流入驻潜力。例如,TON 基金会投资总监 Justin Hyun 表示,Telegram 可能是大规模采用区块链的“特洛伊木马”。

Justin Hyun 谈论小程序的机制。来源:YouTube

Hamster Kombat 能否实现历史上最大规模的加密货币空投?

虽然已知 HMSTR 代币空投量的 60% 将专门用于玩家,但没有关于代币经济学的更多细节。

然而,组织加密货币历史上最大规模的空投可能会很有挑战性,因为它需要超越 Uniswap空投总额超过 64.3 亿美元 — —据CoinGecko称,这是迄今为止最有价值的加密货币空投。

顶级加密货币空投。资料来源:CoinGecko

除了空投之外,Hamster Kombat 已经创下了最快达到 1 亿用户的产品记录,仅用两个月就达到了这一里程碑,并且有望创造吉尼斯世界纪录。