Authored by: Tiger Research

Compiled by: AididiaoJP, Foresight News

The weight of DeFi lending is shifting from protocols to risk managers who possess the power of choice. Entering the market boils down to one decision: to borrow this judgment, to provide it, or to own it yourself.

Key Takeaways

- The role of asset manager is emerging in DeFi. The era where protocols and governance decided everything is over.

- The market is still early, but capital and distribution channels are starting to concentrate towards leading managers, whose track records are becoming institutional benchmarks.

- There are three paths to entry: distribution (risk manager as backend), supply (bringing assets on-chain), and operation (becoming a risk manager).

- The chosen path determines the level of control gained, the capabilities required, and the risks assumed.

- The core question is not *whether* to enter DeFi, but *which* judgment calls to delegate and which to retain.

1. Risk Managers: On-Chain Asset Management Specialists

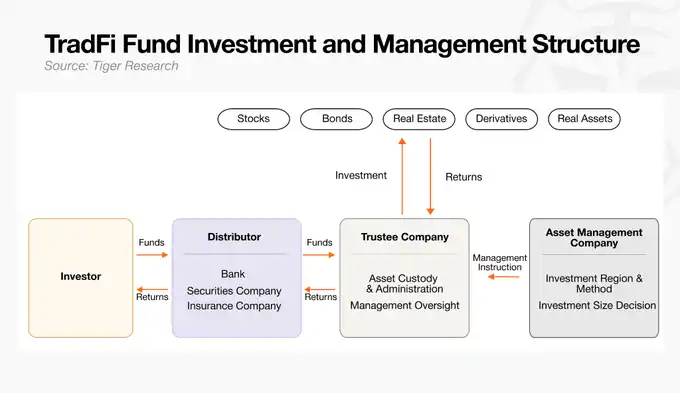

Just as traditional finance long ago separated judgment from execution, the crypto market has matured to a point where each function is handled by specialized players. The division of labor in TradFi is as follows:

- Asset Manager: The "brain" of the fund, formulating strategies and issuing specific instructions to the custodian.

- Custodian: Holds the assets, executes investments per the manager's instructions, and provides oversight.

- Distributor: Distributes fund products to investors and raises capital.

The crypto market has corresponding roles. DeFi was initially designed to rely entirely on smart contract code, but over time it became clear that code alone cannot fully control on-chain risks.

To safely operate on-chain lending, a class of professionals specializing in assessing and coordinating complex risks emerged. They are called risk managers and have de facto taken on the role of asset managers within the on-chain ecosystem.

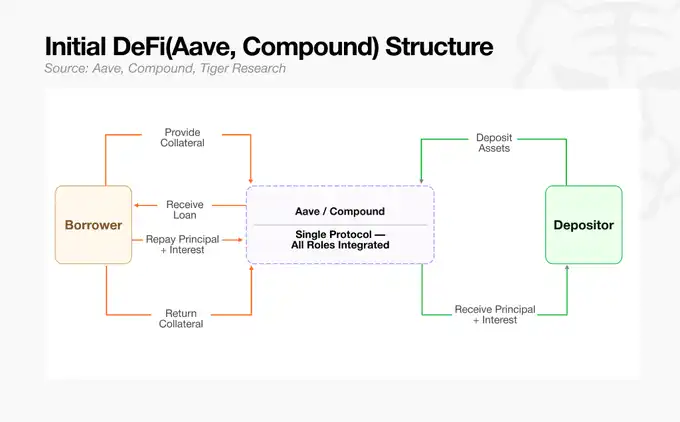

2. Early DeFi Had No Professionals

Early DeFi protocols like Aave and Compound bundled lending infrastructure and risk standards into a single structure. Risk managers existed back then, but because all assets were in one giant pool, their role was limited to being a "risk manager" at the system level, adjusting the protocol's overall risk parameters. As high-volatility assets flowed in, the single-pool design meant one bad asset could spread losses throughout the entire system. Someone had to manage this contagion risk.

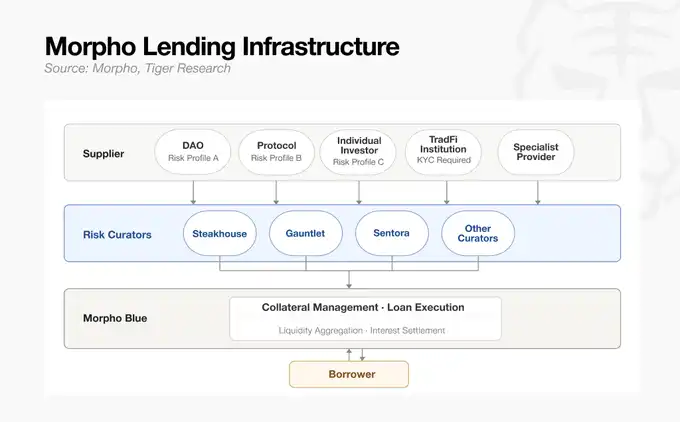

This changed with the advent of Morpho, which separated collateral assets and loan terms into independent markets. By replacing the single giant pool with a multi-vault structure, asset management strategies became modular, and the role of the risk manager transformed completely. They were no longer passive risk managers within a single protocol's fixed framework; they became external professionals able to design and operate independent lending vaults according to their own criteria.

With infrastructure and risk judgment fully separated, risk managers evolved from system-level risk managers into "asset managers" for the crypto market, actively operating multiple vaults.

3. Current Market Leaders

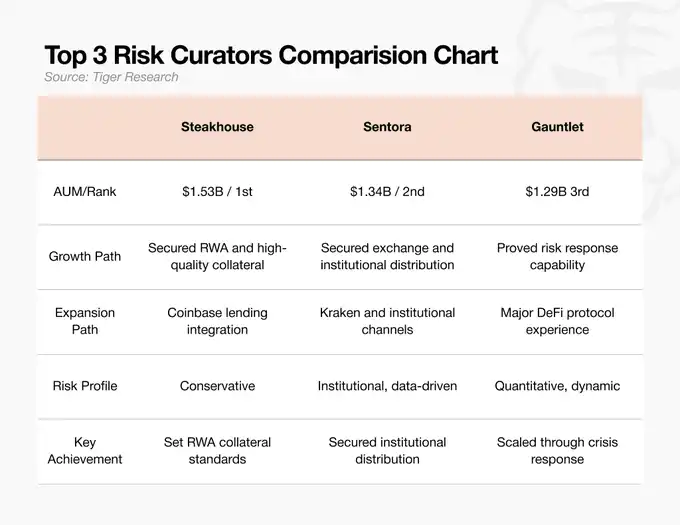

As of May 2026, the risk manager market manages roughly $70 billion in assets, with the top three teams accounting for 70% of that share. This market only truly entered the institutional arena in 2025, yet capital has quickly concentrated, indicating capital is chasing teams with reliable track records. The three leading teams reached the top via different paths:

- SteakhouseFi: A conservative risk manager leading the adoption of high-grade real-world assets (RWAs, like US Treasuries). As the backend for Coinbase's lending service, it unlocked distribution channels and currently ranks first in AUM ($15.3B as of Feb 2026). Beyond AUM, this team sets industry standards for which RWAs qualify as legitimate DeFi collateral.

- SentoraHQ: A team built on AI risk models and institutional-grade data infrastructure. As Kraken's backend, it has secured institutional capital pipelines, ranking second in AUM ($13.4B). It won the channel connecting exchanges to institutional clients.

- Gauntlet: Initially an on-chain quant analytics firm simulating risk parameters. In October 2025, when one of its vaults saw an influx of $775M, the team normalized collapsing APYs within 10 days, proving its capabilities. Ranking third in AUM ($12.9B), it is recognized as the strongest team in risk defense and crisis response to massive inflows.

At this stage, the risk manager market is no longer a simple TVL race but a competition to establish standards first: collateral standards, distribution channels, and risk response capabilities.

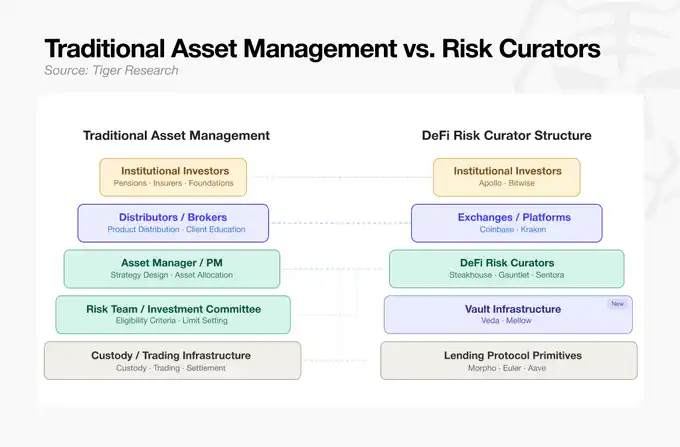

4. Traditional Asset Management vs. DeFi Risk Managers

As Morpho fragmented the market, each collateral type required professional judgment. Specialist risk teams like Steakhouse entered as DeFi risk managers. Through this shift, DeFi began to approximate the traditional asset management process.

Reading the chart from top to bottom shows how today's DeFi infrastructure replicates the labor division of TradFi on-chain:

- Capital Sourcing & Distribution (Top): Institutional investors are at the top as capital sources. Their large capital pools flow into the on-chain ecosystem via major CeFi exchanges and platforms, which assume the role of TradFi distributors (brokers).

- Strategy Design & Risk Control (Middle): Below are the DeFi risk managers who decide how the incoming capital is managed. Analogous to TradFi asset managers' portfolio managers (PMs) and risk committees, they set asset eligibility criteria and limits and design the overall investment strategy.

- Product Assembly & Custody (Bottom): The risk managers' strategies become investable on-chain products via the vault infrastructure below. At the very bottom are lending protocol primitives, which hold assets and execute settlements in code, replacing TradFi's custody and trading infrastructure.

From capital sourcing to management to custody, the entire workflow now mirrors the labor division of traditional finance. For traditional TradFi institutions, on-chain lending is no longer a foreign domain but a structured market with a familiar architecture, creating natural entry points.

5. A TradFi-Like Industry: Where Are the Opportunities?

As on-chain lending infrastructure adopts a labor division akin to TradFi asset management, the door is open for institutional entry. But not every layer has the same entry barriers.

- Distribution Layer: The customer-facing, front-end market. Highly saturated, making it inefficient for TradFi institutions to compete head-on here.

- Management Layer: An area driven entirely by financial expertise and human judgment. Assessing, controlling, and packaging asset risk is the core work of traditional asset managers. They can apply existing risk management capabilities to already-built, modular infrastructure without constructing complex systems, instantly gaining a business model.

- Custody & Infrastructure Layer: Asset custody and transaction processing are technology-intensive, requiring deep blockchain engineering capabilities. It is unrealistic for TradFi institutions to build their own systems and compete here.

Unlike other layers requiring technical or platform-first advantages, the management layer presents the clearest window of opportunity where TradFi institutions can achieve market leadership using the very risk management capabilities they already possess.

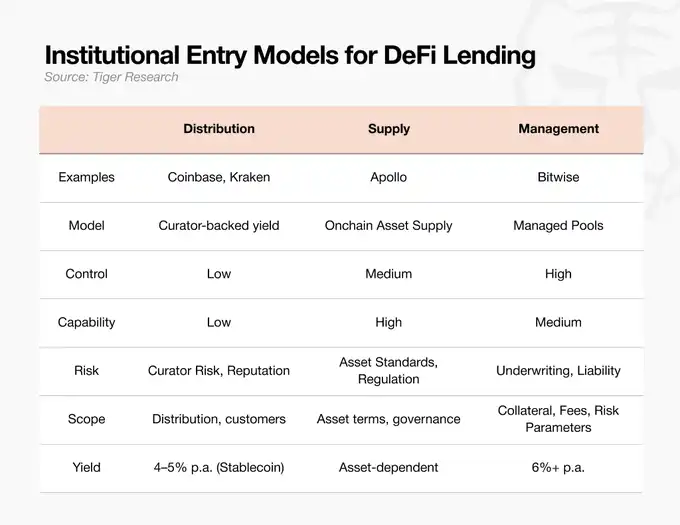

Institutions currently enter the DeFi market through three paths: distribution, supply, and operation. Regardless of the path chosen, the engine driving the market is the asset manager's "risk curation" ability.

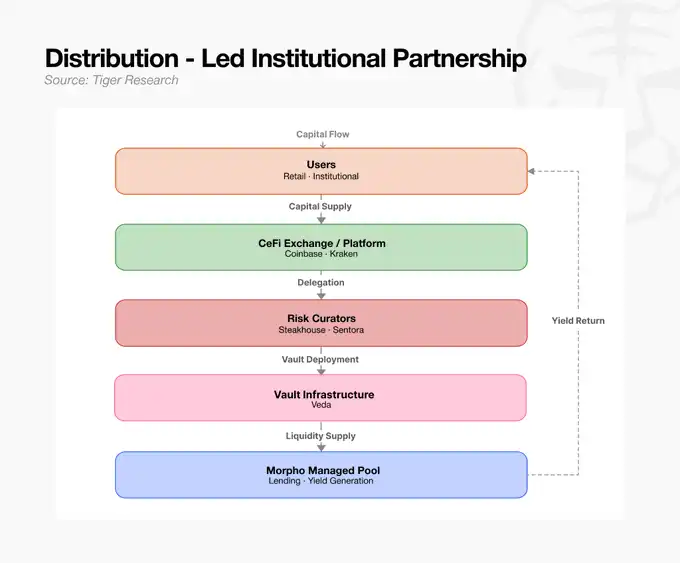

Distribution: Risk Manager as Backend

Connect with proven external risk managers as a backend for quick market entry. This suits exchanges and fintech companies with client channels but lacking internal management capabilities. Strategy is outsourced, but reputational risk and accountability for the chosen risk manager remain with the distributor.

This is the path chosen by centralized exchanges with strong client touchpoints but unwilling to directly manage the complexities of on-chain lending risk. They connect to proven external risk managers as backends and launch lending services. The exchange distributes large capital pools through its own platform, while collateral evaluation and risk management are entirely handed over to the partner risk manager.

Supply: Pushing Assets onto On-Chain Rails

Asset managers holding RWAs or credit assets directly supply these assets to the market. Like Apollo, they can acquire governance tokens of protocols like Morpho while supplying assets, thereby shaping infrastructure standards (e.g., collateral standards). The challenge lies in asset standardization and regulatory infrastructure development.

Large private equity funds or institutions holding real-world assets directly place their own capital on the on-chain rails. Apollo not only simply supplies assets but also acquired governance tokens of a major lending protocol. This move aims to push rules and standards so that its RWAs are recognized as superior, safer "official collateral" in the on-chain market.

But asset suppliers cannot arbitrarily register any asset as collateral. Someone must calmly assess whether the asset is truly safe and whether it can be liquidated immediately in an on-chain liquidation event. This requires the rigorous evaluation and endorsement capabilities of a risk manager. Ultimately, the supply path also must rely on the asset manager's risk validation capability to be viable.

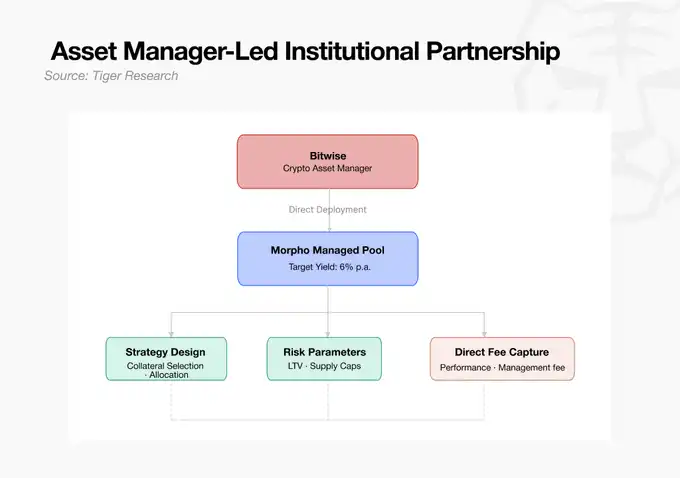

Operation: Becoming a Risk Manager (Bitwise)

The asset manager designs its own strategy and operates its own vault. Bitwise defined on-chain vaults as "ETF 2.0" and entered directly. This path offers the strongest control over fees and collateral standards, but the manager bears full responsibility for operational failure. It suits asset managers with in-house risk teams.

This is the path where a traditional asset manager itself enters as a risk manager, without relying on external platforms. Bitwise defined the on-chain lending vault structure as "ETF 2.0" and entered the market directly. Leveraging its own portfolio construction capabilities and risk control systems, it designs and controls vaults itself, directly establishing a management fee model on-chain.

6. Before the Capital Arrives

Given the current trajectory, traditional asset managers are most likely to gain an advantageous position as on-chain lending matures. With the DeFi ecosystem's modularization and labor division, the capabilities truly needed by the market have shifted. Not the ability to write code, but the traditional financial expertise of underwriting collateral and setting risk limits. The competitive advantage of institutions with decades of experience can directly extend on-chain.

But today's DeFi market is still too small for global mega-managers. The global traditional asset management market is approximately $147 trillion, with BlackRock alone managing $14 trillion. In contrast, the entire DeFi market is around $80 billion, with the portion managed by risk managers at only $70 billion. This is merely 1/2000th of BlackRock's AUM.

Yet, it is precisely this massive scale gap that reveals the runway for growth. Institutional capital will not flow where risks are uncontrolled. Once risk managers lay secure on-chain rails for capital and regulatory frameworks take shape, the story changes. Even a tiny fraction flowing in from the $147 trillion could rapidly expand the $80 billion market.

Some opportunities exist only while the market is still small. Currently, the main players in the risk manager market can be counted on one hand. Institutions going on-chain need rails, and the teams that lay these rails first will set the standards.

Institutions entering later will find a safer, clearer market, but they will also become one of many players within already-established standards.