Crypto’s Stablecoin ‘Wildcat Era’

DeFi protocols are making moves.

With take rates shrinking on fee-based business models and on-chain activity drying up, blue-chip DeFi protocols are seeking to establish alternative sources of revenues in order to diversify and strengthen their protocols.

We’ve seen early signs of this expansion, with protocols such as Frax building out liquid staking and lending products, Ribbon developing an options exchange and Maker breaking into lending with Spark Protocol.

Now, we have a new form of diversification in the form of application-specific stablecoins, which refer to stablecoins issued by DeFi protocols as their secondary, rather than primary, product offering.

These stablecoins are typically issued in the form of credit, where users can borrow against their assets directly within a lending market or through a DEX in order to mint a stablecoin. Protocols can earn revenue from this in a variety of ways such as through borrow interest, minting/redemption of new units, peg arbitrage, and/or the liquidation of positions.

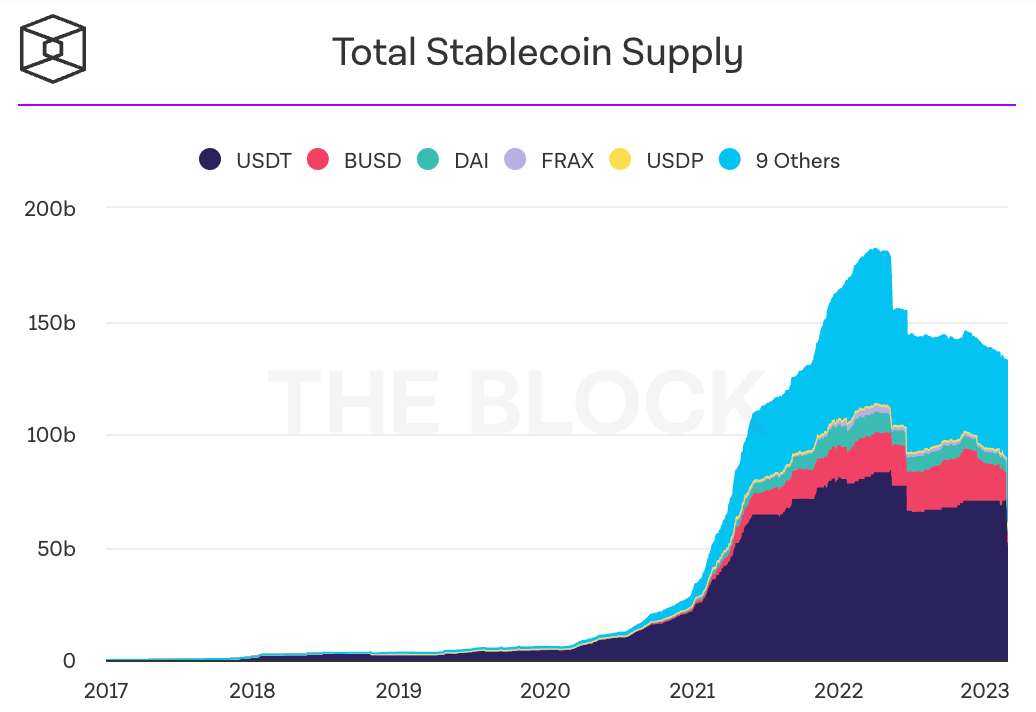

As we know, the stablecoin sector is immense. There is currently $145B in stablecoins within the crypto ecosystem, with a future addressable market in the tens of trillions.

Total Stablecoin Supply - Source: The Block

With regulators targeting centralized, fiat-collateralized stablecoins such as BUSD, a window may open for DeFi protocols to not only diversify their business models, but possibly steal a portion of their market share.

Many will point to DAI and FRAX as the likeliest candidates to take a chunk out of USDC and USDT… but could some application-specific stablecoins play a spoiler role?

What impact will this trend have on the markets and DeFi? Let’s find out!

GHO and crvUSD

The two most prominent protocols launching stablecoins are Aave and Curve, which are issuing GHO and crvUSD respectively. Let’s take a brief look at these stablecoins under the hood.

GHO

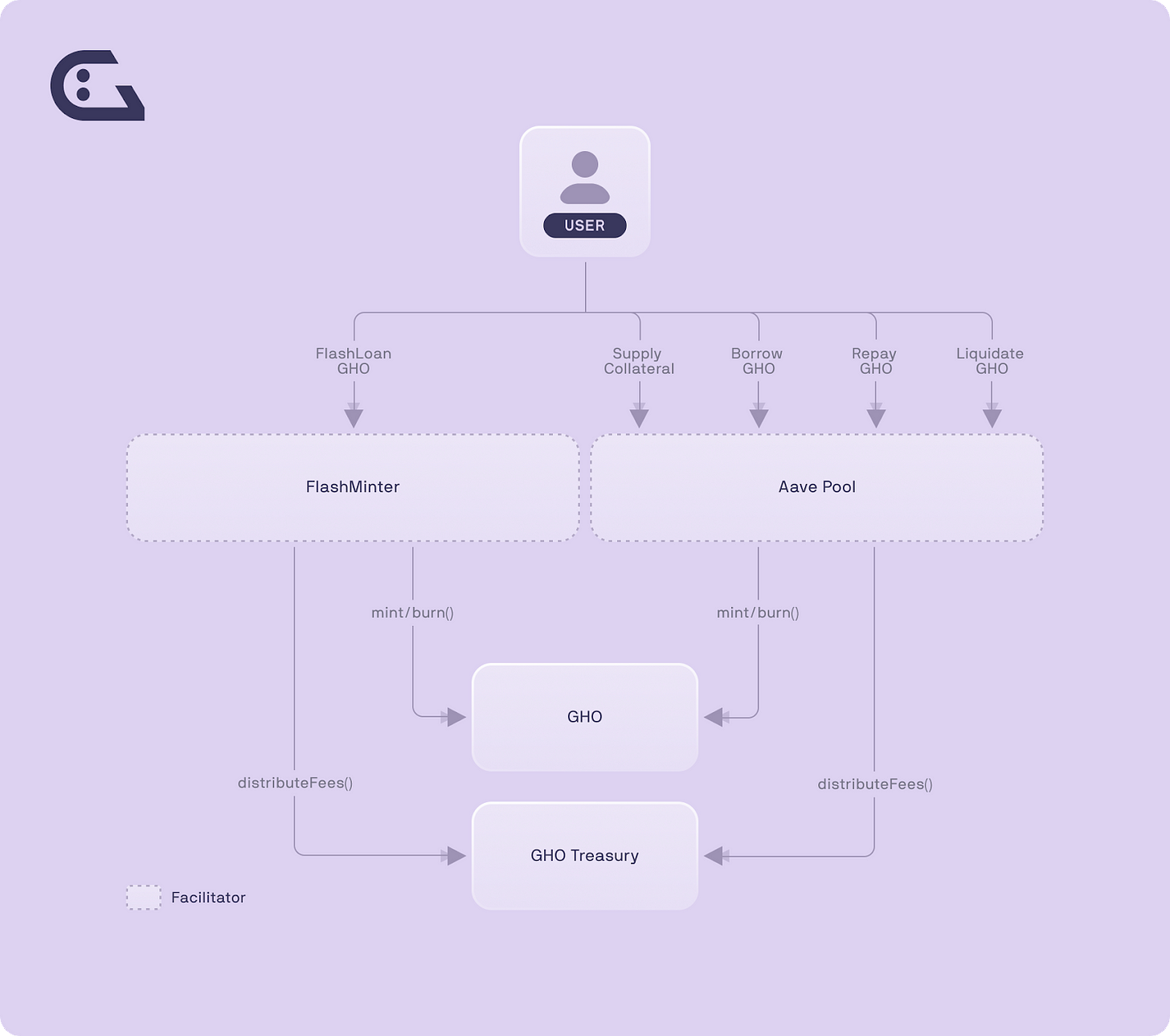

GHO is a decentralized stablecoin issued by Aave. GHO is overcollateralized as it’s backed by deposits in Aave V3, with users able to mint the stablecoin directly into the money market.

GHO is unique in that, rather than having interest rates determined algorithmically like other assets in Aave, its borrow rate will be manually set by governance. This gives Aave total control over the cost to mint/borrow GHO, allowing the DAO to potentially undercut its competitors (more on this later).

GHO Design - Source: GHO Docs

In the future, GHO will be able to be minted from other venues besides Aave V3 via whitelisted entities known as facilitators. These facilitators can mint GHO based on various types of collateral, including delta-neutral positions and real world assets.

We’ve seen similar stablecoin designs before, such as with Frax’s lending AMO and Maker’s D3M. But GHO’s growth prospects are strong thanks to Aave’s built-in user base, brand, team’s business development skills, and the sizable DAO treasury worth $130.9M (though a majority of this is in AAVE tokens).

GHO is currently live on Goerli testnet, and is slated to launch later in 2023.

crvUSD:

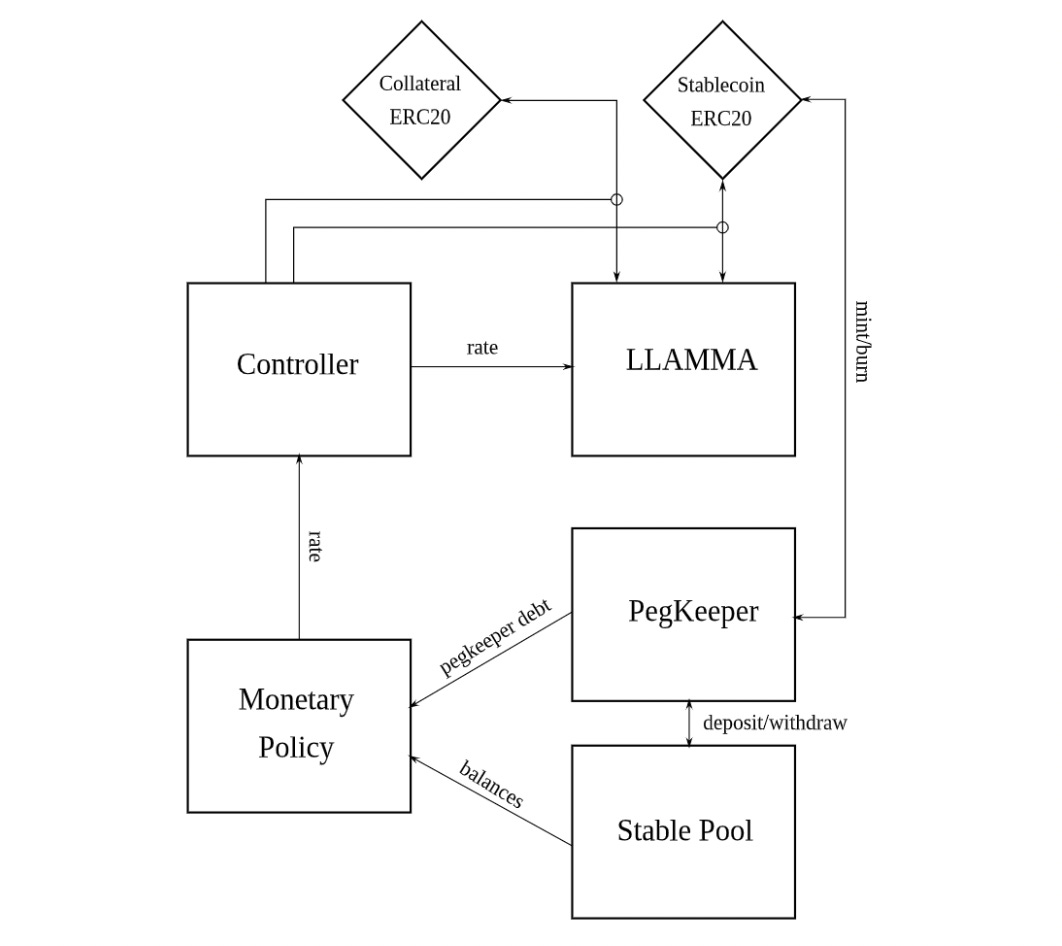

crvUSD is a decentralized stablecoin issued by Curve. Many details surrounding the stablecoin have been kept under wraps, but we know that crvUSD will utilize a novel mechanism known as a lending-liquidating AMM algorithm (LLAMA).

LLAMA employs a “kinder” liquidation design that gradually swaps a user’s collateral into crvUSD as its value decreases, rather than fully liquidating a user’s position in one fell swoop.

crvUSD Design - Source: Curve Stablecoin Whitepaper

In all, LLAMA should help lead to far less punishing liquidations, and this improved UX for borrowers is likely to increase the attractiveness of opening crvUSD-denominated CDPs.

There have been few details given about supported collateral types and the role of crvUSD within the ecosystem, but it's likely that the stablecoin will be minted from LP tokens of Curve Pools. This would help increase the capital efficiency of providing liquidity on the platform, as LPs would also be able to earn from deploying their crvUSD into DeFi.

crvUSD should also benefit from Curve’s gauge system, which is used to allocate CRV emissions, and — by doing so — liquidity on the DEX. It's highly likely that a portion of these emissions will be allocated to crvUSD pools, or that crvUSD will become part of a base pair for other stablecoins, helping it easily build out deep liquidity.

Market Impact:

Now that we have a sense of the state of the app-specific stablecoin landscape, let’s dive into the impact this will have on the market.

A (Theoretical) Increase in Revenue For The Issuing DAO

One of the parties most directly impacted by app-specific stablecoins is the issuing protocol themselves. In theory, creating a stablecoin strengthens the business model of the issuing protocol, as it provides them with an additional stream of revenue.

Currently, protocols like Curve and Aave are dependent on trading fees and the utilization based lending interest respectively. The low-quality nature of these revenue sources has become apparent during this bear market, as reduced trading & lending activity and fee compression due to increased competition have led to steep declines in revenues.

The issuance of an in-protocol stablecoin changes this dynamic, as now protocols will be able to earn an additional source of revenue to bolster their top-line. Although interest revenue is still cyclical in that it is dependent on demand to borrow, it’s generated much more efficiently (i.e. has a Higher Return on TVL) relative to trading fees or capturing the spread on money markets.

While this interest revenue may also be subject to similar fee compression (more on this later), it — in theory — still has the potential to diversify the revenue mix and strengthen the moat of the underlying protocol through other means such as minting/redemption fees, peg arbitrage and liquidations.

*Potential* Value Accrual For Tokenholders

Another party set to benefit from the application-specific stablecoin boom are the tokenholders of the issuing protocols.

While this is dependent on each individual protocol, any revenue share will increase the yields that can be earned to the holders that either stake or lock a token.

In a bear market where we’ve seen revenue-sharing assets like GMX and GNS outperform, protocols that issue stablecoins and then share that revenue with their holders will make their tokens more attractive and in doing so increase the odds they outperform.

For instance, it’s likely that Curve will share crvUSD revenue with veCRV lockers, meaning that lockers will earn a share of trading fees, governance bribes, and now stablecoin based cash flows.

Given the regulatory risks present with this approach, it’s also possible that issuing protocols add utility to their tokens in other ways. For instance, AAVE stakers will be able to borrow GHO at discounted rates relative to other users on the platform.

Bribes and Liquidity Fragmentation

One of the most critical factors to the success of a stablecoin is having deep liquidity. Liquidity is the lifeblood of any stablecoin — not only does it enable low-slippage trades but it also helps facilitate integrations, as liquidity is needed for liquidations on lending platforms and to secure valuable infrastructure such as a ChainLink oracle.

This need for liquidity among application-specific stablecoins is likely to help buoy the governance bribe markets.

Popularized by the Curve Wars, stablecoin issuers can build out liquidity for their token on decentralized exchanges like Curve and Balancer through bribes, or payments made to tokenholders in order to secure their vote on directing emissions to select pools.

Through bribing, issuers are able to rent liquidity on a desired venue on an as needed basis. An abundance of application-specific stablecoins is likely to lead to a greater number of DAOs playing this game and bribing these tokenholders.

In turn, this should increase the yields for lockers of CRV and BAL as well as CVX and AURA, who through metagovernance control a majority of emissions on Curve and Balancer respectively and receive a majority of bribes.

Another beneficiary of this bribe boom are marketplaces such as [Redacted] Cartel’s Hidden Hand and Votium who facilitate these transactions.

However, this bribing will come at a cost to end-users in the form of fragmented liquidity. In a crypto market that is showing few signs of seeing inflows, liquidity is likely to be stretched more thinly across a variety of different stablecoins, leading to worse execution for whale traders.

A Credit Boom

The growth of application-specific stablecoins is also likely to catalyze a DeFi credit boom by leading to a proliferation of low borrow rates.

To compete with incumbent stablecoins like USDC, USDT, DAI, and FRAX, stablecoins such as Aave and Curve will likely have to offer GHO and crvUSD at low borrow rates in order to attract users to mint new units to grow their circulating supplies.

In theory, this low-interest rate driven credit boom can be a stimulus for DeFi and crypto markets broadly, with yield farmers and degens alike able to lever up and borrow at incredibly low rates. It may also open up interesting Crypto <> TradFi arbitrage opportunities, as users will likely be able to borrow stablecoins at a rate far cheaper than that being paid by US Treasuries.

We’re already seeing early signs of adjustment to this new paradigm from stablecoin issuers like Maker, who will offer DAI borrowing at the 1% Dai Savings Rate (DSR) via Spark, a Maker-controlled fork of Aave V3.

While this undercutting of borrow rates may damage the bottom lines of issuing protocols like Aave and Curve, it may help satiate a market that is starved for credit following the implosion of CeFi lenders in 2022. With interest rates dramatically higher than the DSR and the likely borrow rate of stablecoins such as GHO, crypto will become one of the cheapest credit markets in the world.

DeFi’s Wildcat Era

Wildcat banking was a period in American history where banks each issued their own currency. As we say, DeFi is speed-running the history of finance and — with stablecoins like GHO and crvUSD — appears on the verge of starting down a similar trajectory.

While they are unlikely to surpass incumbents with far more lindy such as DAI and FRAX, GHO and crvUSD benefit from integrations with their issuing protocols and can carve out a niche.

While, in theory, these stablecoins would help strengthen the business models of their issuers and value accrual to tokenholders, they are unlikely to do so due to a “race to the bottom,” where issuers will undercut one another on rates in order to offer borrowers the cheapest possible credit.

As a result, these low interest rates are likely to catalyze a credit boom, stimulating the on-chain economy with cheap capital.

In a world where the cost of money has increased dramatically over the past year, this has the potential to position DeFi as one of the cheapest capital markets on Earth, perhaps re-igniting interest and leading to inflows into the ecosystem.