作者:Lucas

编译:佳欢,ChainCatcher

以太坊已死

加密推特上对以太坊的情绪正处于历史低点。

多年来我的许多同行已经放弃了以太坊,甚至退出了更广泛的加密行业。他们中的大多数人几乎不再持有ETH,很大程度上是因为他们认为它不再具备投资价值。这并非针对某个个人或群体,而是我在整个行业的同龄人中真实看到的情况。

虽然更大规模的资金外流似乎是因为加密货币不再是前沿科技(人工智能、机器人技术和生物科技已经取而代之),但围绕ETH的悲观情绪很大程度上源于其过去五年的价格表现。

持有ETH的体验很糟糕。无需拐弯抹角。

但我依然看好以太坊和ETH,实际上比以往任何时候都更加坚定。你也应该如此。

事实上,以太坊正处于其最激动人心的增长和普及阶段的边缘。让我来解释一下。

关于价格表现

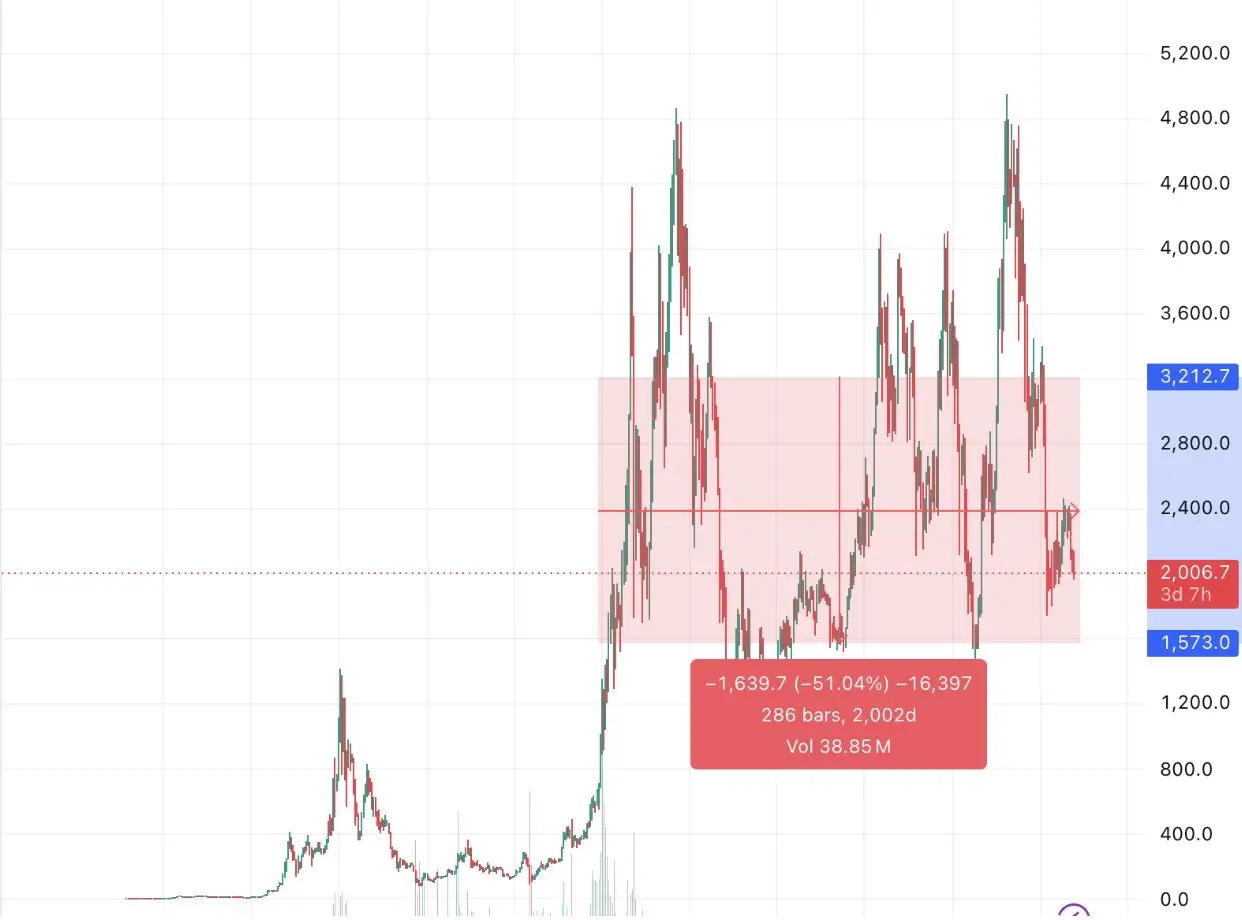

让我们从一个显而易见的问题开始:过去大约五年里,ETH的价格表现绝对是一塌糊涂。

从2021年持有至今的人,最好的情况是盈亏平衡,更糟的情况是亏损惨重。即使经历了最近的下跌,BTC依然高于2021年周期的历史高点,并在2025年峰值时达到了上轮高点的两倍。

相比之下,ETH目前比上个周期的历史高点低了约60%,并且在2025年勉强创下新高,甚至没有突破5000美元。

与此同时,标普500指数几乎每天都在创下历史新高,而华尔街追捧的任何热门概念(如人工智能、半导体、能源等)都在疯狂飙升。

好消息是,如果把时间线拉长,图表看起来实际上只是一个多年的盘整期。以太坊依然拥有超过2000亿美元的市值,并基本守住了2000美元的关口,稳居全球前100大资产之列。

更好的消息是,纵观历史,高增长资产在迎来史诗级上涨之前,经历数年的盘整和震荡并不罕见。

请忽略百分比波动的数字。这里主要衡量的是价格在这个区间内停留的时间。

事实上,当今世界上所有最大的公司都经历过这个阶段。

第一个例子是亚马逊($AMZN)。贝索斯带领公司在整个2000年代经历了近10年的盘整,熬过了互联网泡沫破裂后的低谷期,最终成为全球市值最高的公司之一。

华尔街的宠儿英伟达($NVDA)在2010年代也经历了长达7年的盘整。乘着人工智能浪潮的东风,它现在已成为全球最有价值的公司之一。

苹果($AAPL)在80年代和90年代也同样如此,一直在努力寻找立足点,直到史蒂夫·乔布斯于1997年重返公司。

最后,微软($MSFT)在突破历史高点之前经历了约15年的盘整。如果你在2000年买入MSFT,直到2015年才真正回本。它现在是全球市值第二大的公司,也是过去五年表现最好的公司之一。

相信你已经明白了。世界上几乎所有最有价值的公司都经历过这些极其漫长、乏味的盘整期(如果幸运的话,它们会短暂重测历史高点然后再次下跌),最终才遇到推动其下一轮增长的催化剂。

同样值得注意的是,在这些时期中,标普500指数屡创历史新高,而上述资产的表现却跑输大盘。

因此,就ETH的价格表现而言,如果透过金融史的镜头来看,过去五年的情况并不罕见。

最令人欣慰的是,当你抛开价格表现去审视其内在时,你会发现以太坊的基本面从未如此强劲。

关于网络活动

你可能会认为,伴随着糟糕的情绪和价格走势,以太坊的网络活动也会随之低迷。

交易量应该在下降,费用会高到没人愿意使用,而且几乎不会有任何普及。

现实情况却截然相反。

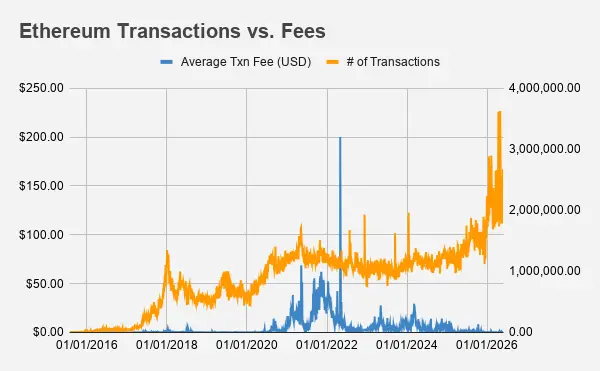

以太坊上的交易量正在激增。费用比以往任何时候都要便宜。而且代币化的速度正在加快(下文将详细说明)。

数据来源:Etherscan。

2026年5月,以太坊平均每天处理227万笔交易。这是该网络的历史新高。与此同时,这段时间的平均费用仅为0.27美元。这与2021年狂热时期人们支付的50到100美元以上形成了鲜明对比(尽管如今的交易量更大)。

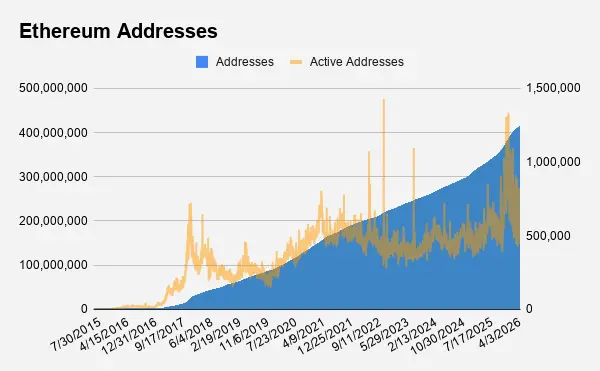

此外,地址数量继续增长。该网络已突破4亿个地址,并在2026年以平均每天约0.08%的稳定速度增长,而最近几个月的日活跃"用户"突破了100万以上。

按照这个速度,假设在此期间没有任何重大的增长催化剂,以太坊将在2029年中期的某个时候突破10亿个地址。

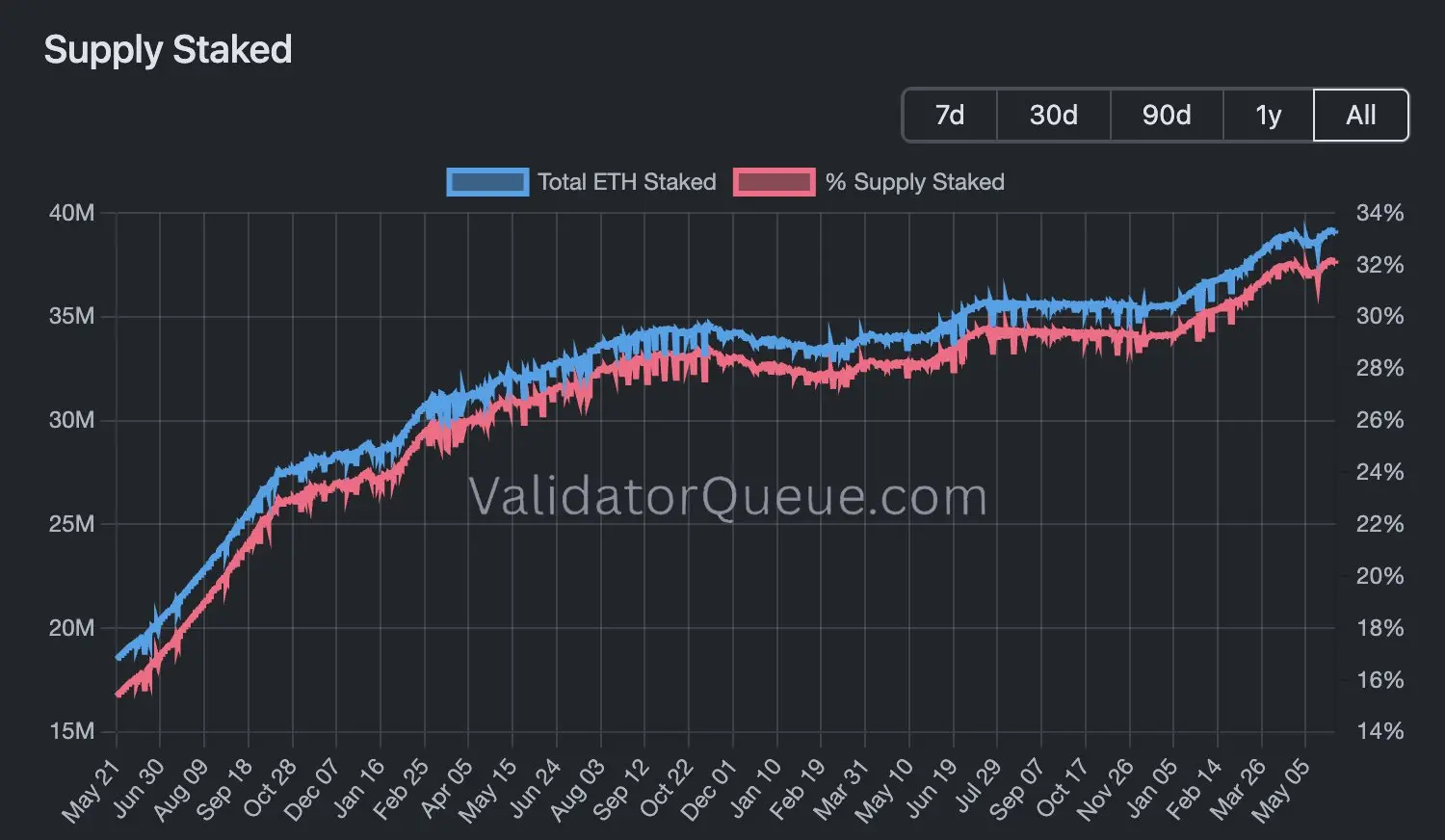

最后,网络上质押的ETH数量不断创下新高。目前超过32%的供应量被用于保障网络安全。

这一切都说明:以太坊在保持其安全性和去中心化的同时,已经实现了显著的扩容。

此外,以太坊在其存在的十多年里拥有100%的正常运行时间,这赋予了该网络一种不公平的优势:它是世界上最具可信中立性、最安全、最可编程的区块空间。

这是以太坊下一步成为全球金融系统基础设施的先决条件。

全球金融系统的基础设施

自2017年进入这个领域以来,我对以太坊的论断始终是:

- 所有价值都将被代币化

- 以太坊是代币化价值的结算层

- ETH将捕获结算层活动所产生的价值。

以太坊在其存在的第一个十年里,一直是加密原生代币化(如DeFi、NFT、模因币等)的实验阵地。这是奠定基础的关键一步,虽然这种实验将继续存在,但该网络正在开启新的篇章,将其自身推向万亿美元的级别。

对于硬核的加密原住民和密码朋克来说,这一章可能显得更加"无聊",但这无疑对世界扮演着极其有价值和重要的角色。这也是我们所有人都应该支持的。

以太坊将成为注定要上链的700万亿美元传统资产的主要大本营。

许多读到这里的人会回应道"以太坊无法扩容来支持这一点",或者"其他竞争对手会吞噬市场份额"。

但对于这些批评者来说,残酷的现实是早期数据显示了完全相反的结果,金融系统正在向以太坊靠拢。

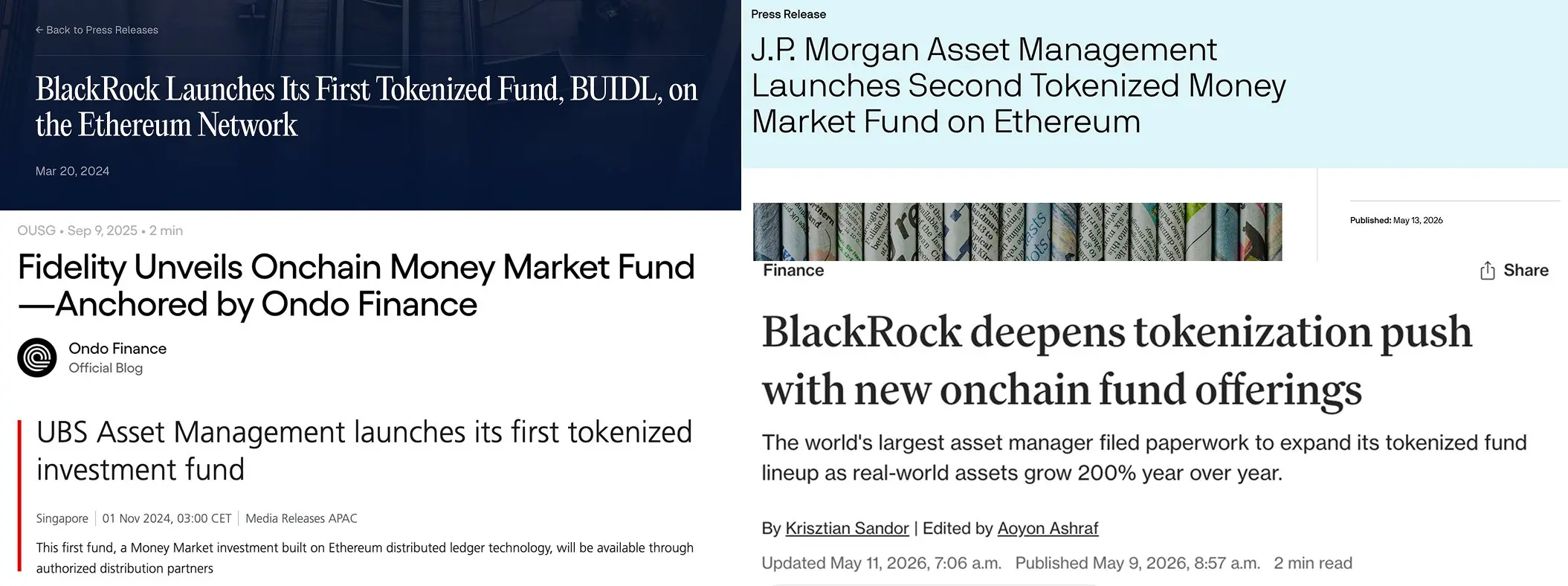

过去大约两年里的一系列新闻头条。注意它们都有一个共同点。

当今的金融机构需要确定性。银行、资产管理公司和清算所决定信任区块链来保障其宝贵资产的安全,这是一个巨大而重要的决定。

他们需要抓住眼前的巨大机遇,但同时他们也不想被解雇。

这并不意味着像Hyperliquid和Solana这样的项目不能取得成功,或者不能分得一杯羹,因为这块蛋糕足够大。事实上,我深信这一波浪潮的受益者绝不止一个。

但是,在机构迈向代币化的进程中,以太坊将是首选。

如果你不相信新闻头条,别担心。我有证据。

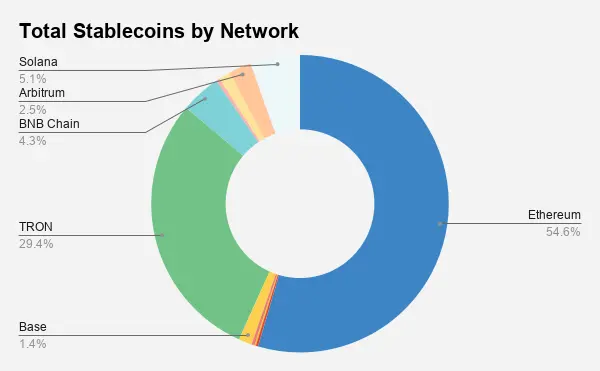

稳定币是首个找到产品市场契合度的代币化现实世界资产。其流通量已超过3000亿美元,而Tom Lee称其为加密货币领域的"ChatGPT"时刻。

稳定币的主要阵地在哪里?

以太坊,占据了约54%的总市场份额。

数据来源:rwa.xyz

它清晰地描绘了我对 RWA 代币化发展的预期:以太坊胜出,而许多其他网络也将获得自己的份额。

迄今为止的数据也支持了这一主张。

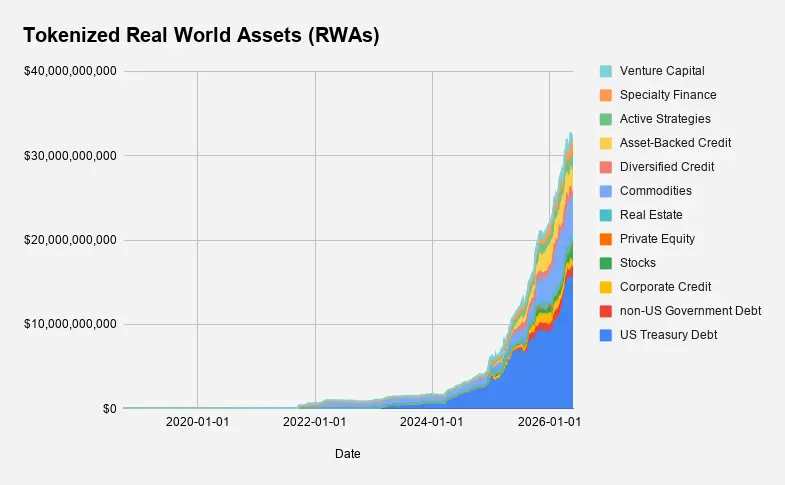

根据@RWA_xyz截至2026年6月1日的数据,现实世界资产(RWA)的总价值目前正呈抛物线增长,超过了约300亿美元。

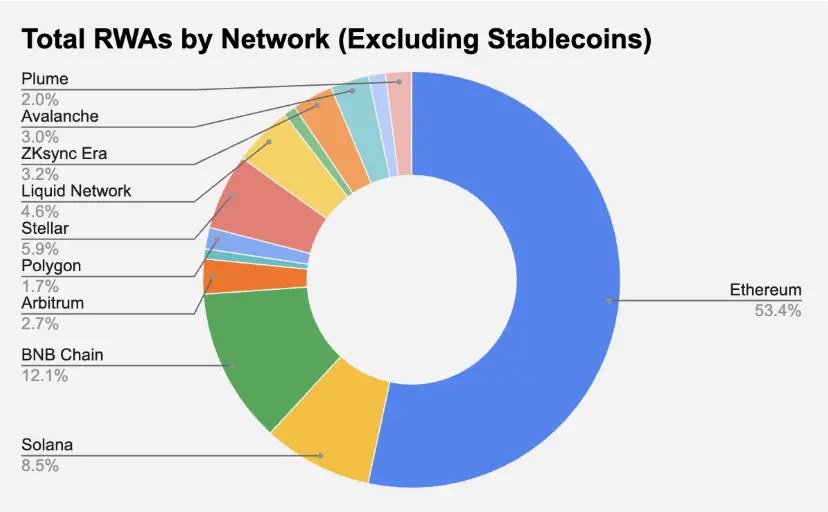

不出所料,超过53%的现有RWA位于以太坊上。尽管各个Layer 1之间竞争激烈,且任何网络都有机会争夺非稳定币RWA的蛋糕,但以太坊依然是占据主导地位的赢家。

如今的RWA让我联想到2019/2020年的DeFi。一个全新且不断兴起的领域,有着成为下一个"大趋势"的清晰路径,并有早期的增长数据作为支撑。

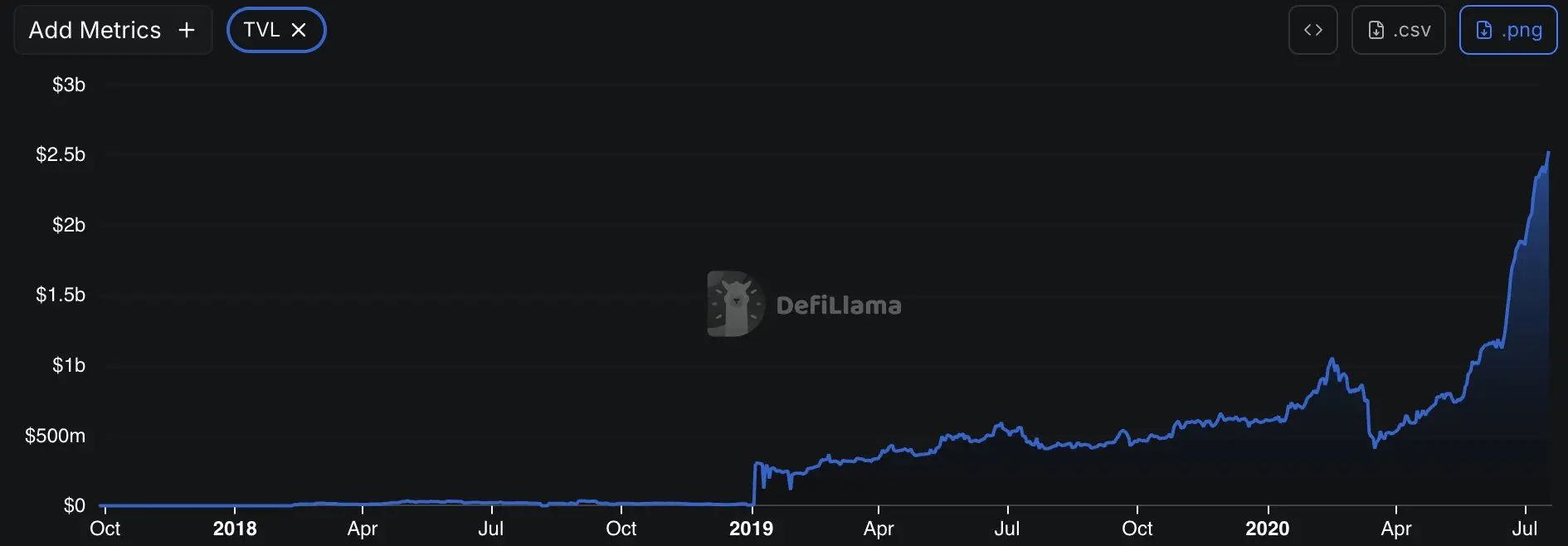

这是来自@DefiLlama的关于DeFi TVL在2020年初呈指数级增长的片段。如果你仔细观察,这张图表应该看起来很眼熟。

巧合的是,当DeFi的TVL达到数十亿美元时,正是ETH停滞不前的时期。

DeFi之夏如火如荼,流动性挖矿风靡一时,然而ETH仍在从新冠疫情引发的崩盘中恢复,估值在200亿至250亿美元之间徘徊(仅为如今估值的十分之一)。

与此同时,当时刚推出不久的BNB Chain作为一种可扩展且便宜的替代方案,正在威胁以太坊的宝座。

直到DeFi开始占据网络相当大的比重(在2021年初约占网络市值的20%),ETH才开启了其史诗级的上涨,从约300美元飙升至该年底的约4000美元。

作为背景参考,目前以太坊上所有RWA(不包括稳定币)的价值为160亿美元,占ETH 2300亿美元市值的约7%。我们现在实际上正处于同样的十字路口,只不过所有的数字都放大了10倍。不是30亿美元的DeFi,而是300亿美元的RWA;ETH也不再是停滞在200美元,而是稳坐在2000美元。

替代BNB Chain的是Hyperliquid(顺便说一句,BNB的表现依然非常出色)。

✍️ 补充说明:不可否认,当时的DeFi比今天的RWA产生了更多对ETH作为抵押品的需求,加上NFT为"ETH作为货币"的叙事锦上添花。

另一方面,当时的以太坊还没有权益证明(PoS)机制,而EIP 1559直到周期尾声才实施。现在这两种机制都已上线,因此有一条清晰的路径表明:以太坊上的任何活动都会将价值回馈给ETH。

如果这种"扩大10倍"的推算准确,这意味着在本轮周期中,RWA的总价值可能超过1万亿美元(DeFi TVL的峰值约为1500亿美元)。这还是在不包括稳定币的情况下。

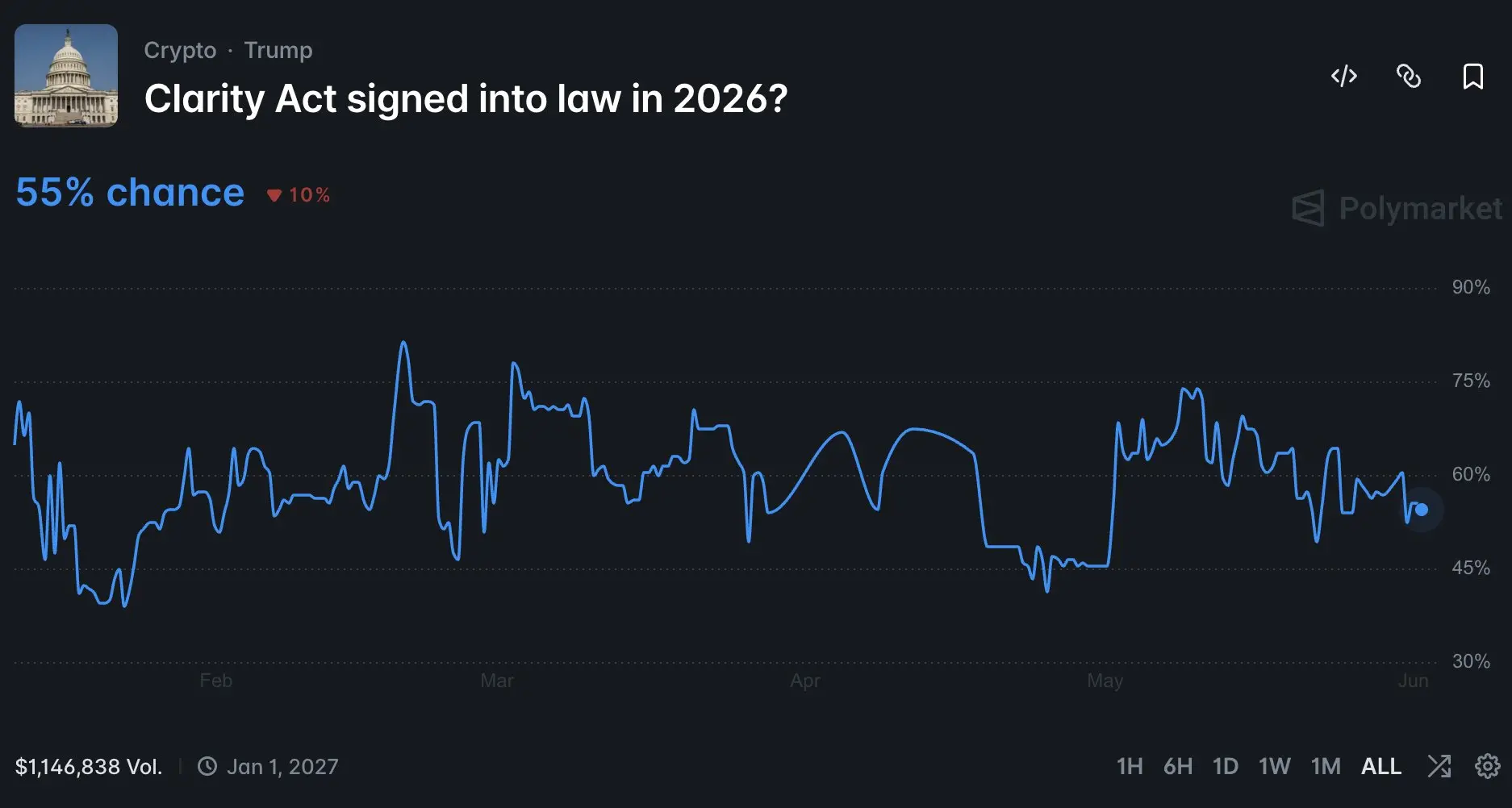

随着《清晰法案》(The Clarity Act)的推进,这种假设变得更加合理,该法案为万物代币化以及美国(乃至全球)金融系统的链上迁移铺平了道路。

根据@Polymarket的数据,截至撰稿时,该法案在年底前签署成为法律的概率约为55%。

如果它在2026年或之后签署成为法律,这将成为以太坊和整个加密领域的重大催化剂。

以太坊依然生机勃勃

所有股票、债券、大宗商品、货币、房地产、艺术品、知识产权等任何有价值的东西都将被代币化。

这是世界的下一项伟大金融创新。加密行业终于为此做好了准备。该行业在其生命的前20年中,一直致力于将独特而奇特的加密原生价值(协议、应用程序等)代币化。

下一个20年将致力于将世界上其他所有事物带到链上。

尽管加密推特上的情绪依然糟糕,但我坚信,以太坊将成为世界上大部分代币化价值的归宿。

为什么?因为它在必须依靠实力赢得的领域胜出了:安全性、可靠性和流动性。

如果以太坊承载了世界上大部分的价值,市场最终将不得不重新对ETH进行定价(就像过去那样)。

但我想我会把这个分析留到下一次探讨。

感谢阅读。挺住,ETH的持有者们。