Tesla has set its sights on the AI infrastructure business.

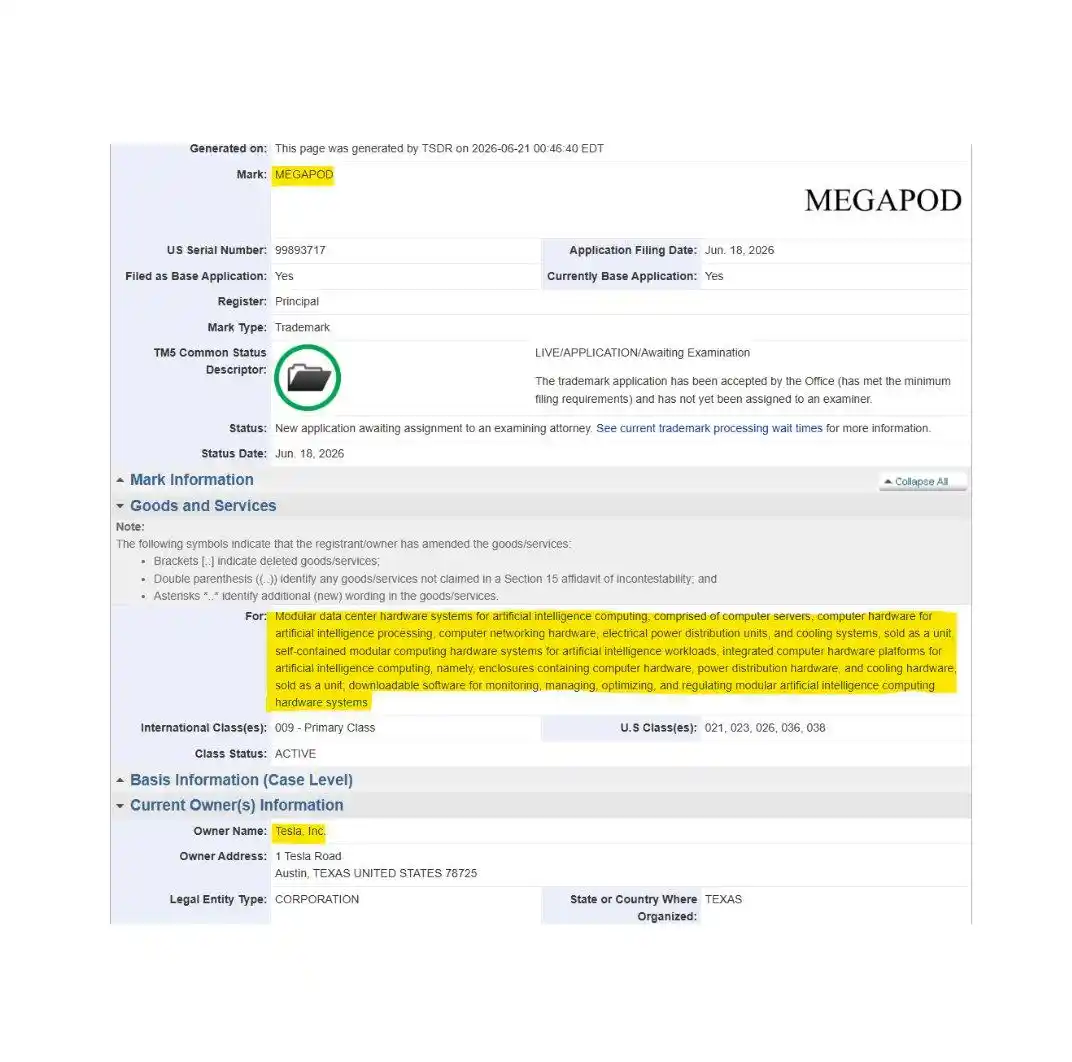

Recently, Tesla filed a trademark application named "Megapod" with the United States Patent and Trademark Office (USPTO), planning to sell modular AI data center hardware.

According to the trademark description, this is a modular data center hardware system for AI computing, including computer servers, AI data processing hardware, network equipment, power distribution units, and cooling systems.

However, just under a year ago, Tesla had disbanded its Dojo team, shutting down its only in-house AI training supercomputer.

After bidding farewell to Dojo, they are now registering a new trademark for AI data centers.

Hmm? Is Tesla just changing its approach to continue pursuing computing power?

What is Megapod?

Currently, confirmed information comes from the trademark application.

The trademark name Tesla submitted is MEGAPOD, with application serial number 99893717 and a filing date of June 18, 2026.

In terms of type, this is a standard character trademark, meaning they are securing the name "MEGAPOD" first. The filing basis is intent-to-use, indicating "an intention to use" the mark, but the product has not yet officially launched.

The description in the trademark application is quite specific. It states that Megapod covers:

Modular data center hardware systems for artificial intelligence computing, comprising computer servers, computer hardware for artificial intelligence data processing, network equipment, power distribution units, and cooling systems.

It also includes "self-contained modular AI computing hardware systems" and "downloadable software for monitoring, managing, and optimizing the aforementioned systems."

In simple terms, Megapod sounds like a plug-and-play AI data center module.

It packs servers, network equipment, power supplies, and cooling systems into a single rack. Just haul it to a site, plug it in, and it's ready to run AI training and inference.

This is also where it shares a lineage with Tesla's existing Megapack and Megablock.

Megapack sells large-scale energy storage batteries, while Megablock is an even larger, more modular energy storage system.

Megapod, on the other hand, seems to apply this "modularity" concept from power systems to AI compute systems.

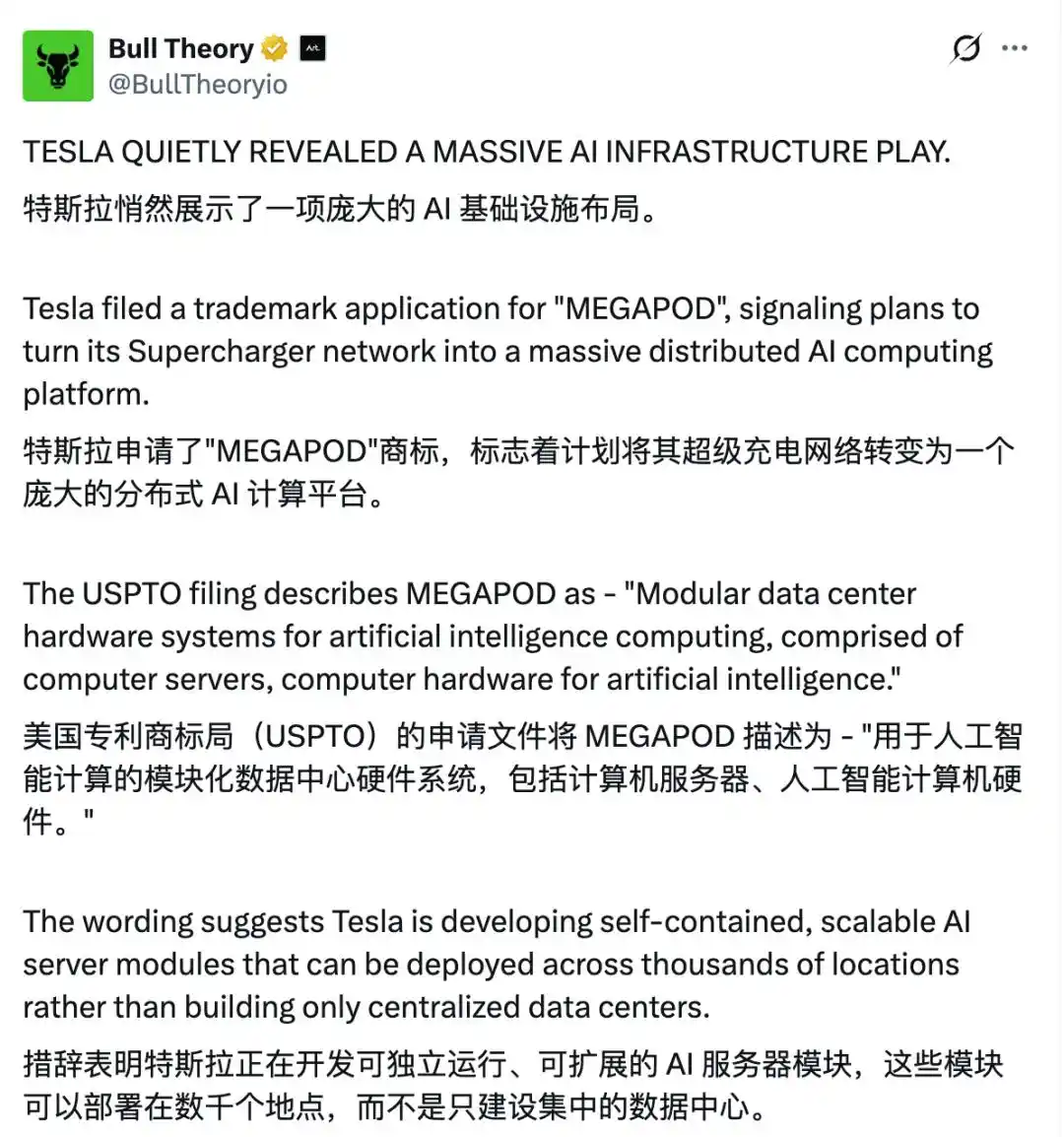

Some netizens have therefore directly called it: Tesla has quietly revealed a massive AI infrastructure play.

Others have speculated further, linking it to Musk's previous mentions of "using idle electricity to run AI." There's even conjecture that Tesla might connect its Supercharger network, battery storage, and AI compute nodes in the future to form a distributed AI infrastructure.

However, for now, Megapod is just a trademark application. There are no prototypes, specifications, prices, or delivery timelines.

Therefore, there's still a long way to go before Megapod becomes a real product.

Yet, the trademark itself indicates that Tesla is already seriously considering turning AI infrastructure into a marketable hardware category.

Is Tesla Trying to Steal Nvidia's Business?

At first glance, Megapod easily brings Nvidia to mind.

After all, the most expensive and critical components in AI data centers today are Nvidia's full-rack compute systems.

Take the GB200 NVL72, for example, which has already become a de facto standard for high-end AI data centers.

It integrates GPUs, CPUs, high-speed interconnects, liquid cooling, and networking into a single rack. Customers buy it and deploy it directly for large model training and inference. Currently, global cloud providers, AI companies, and sovereign AI projects largely revolve around this ecosystem.

In other words, in the business of "modular AI compute," Nvidia is already the absolute core player.

So, is Tesla's Megapod coming to snatch Nvidia's lunch?

In the short term, not necessarily.

Because Tesla itself is also a Nvidia customer. Tesla needs vast numbers of GPUs to train its FSD, robotics, and in-vehicle AI models; Musk's xAI is also procuring Nvidia chips on a large scale to build training clusters.

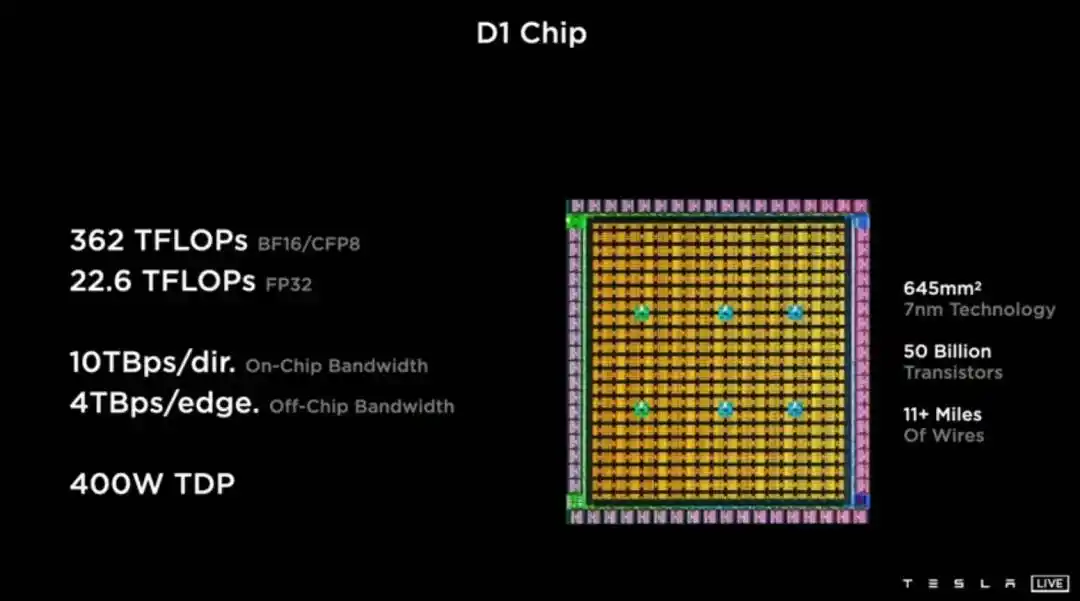

Moreover, Tesla's history with in-house AI chips has been quite bumpy.

Tesla once heavily bet on the Dojo supercomputer, hoping to use its self-developed D1 training chips to support FSD model training.

At the 2021 AI Day, Tesla officially showcased Dojo and the D1 chip, with the rationale being to accelerate autonomous driving model iteration through a self-developed training system.

But by 2025, the Dojo team was disbanded, its lead departed, some members moved to AI chip startups, and the remaining personnel were transferred to other Tesla data center and computing projects.

Musk later stated that the company should not spread its resources thin by expanding two different AI chip designs, and that the focus would shift to AI5/AI6, relying more on external compute ecosystems like Nvidia and AMD.

From this perspective, Tesla's new move likely isn't about stealing Nvidia's GPU business, but rather targeting another layer of the AI data center business: power, energy storage, cooling, power distribution, and modular deployment.

This is also a current pain point for AI data centers. Large model training and inference are consuming electricity voraciously. New AI data centers aren't just short on GPUs; they also lack grid access, transformer capacity, cooling systems, and rapidly deployable infrastructure.

Many projects can't start running even after the chips arrive, often stalled by power supply, heat dissipation, construction timelines, and grid connection approvals.

And these problems happen to fall closer to the capabilities of Tesla's energy business.

Tesla's Truly Profitable AI Business Might Be Batteries

Over the past few years, when Tesla talks about AI, the outside world has focused most on FSD, Optimus, and Dojo.

But from a business perspective, the most direct connection between Tesla and AI data centers might actually be the Megapack.

Megapack is Tesla's large-scale energy storage battery product, targeting grids, power stations, commercial and industrial sectors, and large infrastructure projects.

After an AI data center connects to the grid, it creates very sharp fluctuations in power consumption. Especially during large-scale GPU cluster training, loads can spike or drop rapidly, placing high demands on grid stability.

This is where energy storage systems can act as a buffer.

They charge when grid power is abundant and discharge when AI cluster loads increase; they can also help smooth out shocks caused by power fluctuations during training tasks.

This is the real entry point for Tesla's energy business into AI data centers.

Documents have previously shown that xAI purchased approximately $1 billion worth of Tesla Megapacks cumulatively from 2024 to April 2026, with a single-month purchase of $269 million in April 2026 alone.

This indicates that a major spending area for AI infrastructure is no longer just chips and servers. The power system itself is becoming part of the AI race.

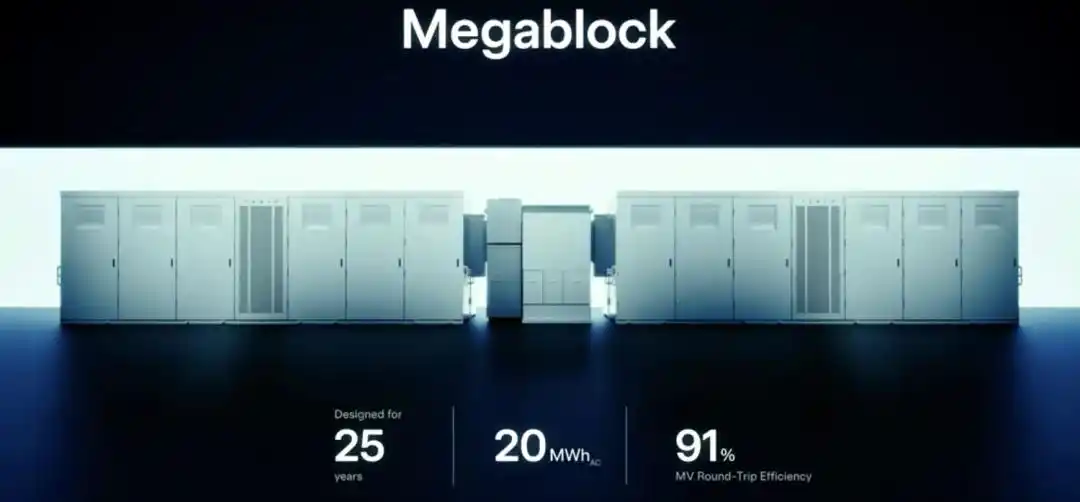

Judging by the names, from Megapack to Megablock to Megapod, there's clear continuity.

A proper "mega trilogy".

Megapack solves energy storage; Megablock solves larger-scale, faster-deploying power modules.

If Megapod materializes, it could further bundle servers, networking, power, cooling, and software management into an integrated infrastructure product for AI customers.

However, AI data center hardware is an extremely complex market, already populated by established players like Nvidia, Dell, Supermicro, Vertiv, Schneider, Eaton, and others.

From GPU racks to server integration, liquid cooling systems, power distribution, and UPS, each layer has high engineering barriers and long customer qualification cycles.

Tesla's strengths lie in modular manufacturing, battery storage, power control, and AI demand within Musk's ecosystem.

But its weaknesses are also evident: limited experience in enterprise data center delivery, an unstable in-house AI chip roadmap, and it remains unknown whether customers are willing to entrust critical AI infrastructure to Tesla.

However, Musk has already tasted the sweet success from SpaceX's massive compute contracts.

According to reports, Google will pay SpaceX $920 million per month to lease approximately 110,000 Nvidia GPUs along with related CPUs, memory, and other components, for a period of three years.

Prior to this, Anthropic also signed a contract to lease all the compute capacity at SpaceX's Colossus data center for $1.25 billion per month.

Combined, these two contracts mean SpaceX can rake in around $2.17 billion per month just from "renting out compute power."

What? A rocket-building company earning over $2 billion a month just from renting out idle GPUs???

When it comes to being a landlord on this scale, no one does it quite like Musk.

This also makes Megapod even more intriguing:

On one side, SpaceX is turning AI compute into a rentable asset, while on the other, Tesla is using the "mega trilogy" to penetrate power, energy storage, cooling, and modular deployment.

One can imagine that Megapod might not become "Tesla's version of Nvidia."

But when every AI company is short on power, cooling, and deployment speed, this business might just be more tangible than telling autonomous driving stories~

References:

[1]https://electrek.co/2026/06/21/tesla-megapod-ai-data-center-hardware/

[2]https://x.com/BullTheoryio/status/2068569421971436011

[3]https://techcrunch.com/2026/06/05/google-will-pay-spacex-920m-per-month-for-compute/

This article is from the WeChat public account "QbitAI," author: Ting Yu