今日,比特币突破 68, 686 美元,据创下历史新高仅需 314 美元;与此同时,比特币生态的 NFT、铭文等资产也迎来可观涨幅。

比特币涨了,但社区里似乎并不太开心,因为很多人手上都没有比特币,而是一手不涨反跌的山寨币。

大多数人,都踏空了

华尔街的资金持续不断的进入比特币,但大部分散户手中却已经没有足够的资金上车比特币。

年前,大家拿着钱参与比特币、以太坊各个生态的铭文,现在还在翘首以盼铭文第三春。随着质押概念的火热,散户手里大部分筹码又被动锁仓,存入 EigenLayer、Blast、Merlin 等项目之中。但不得不说,如果不是这些锁仓项目,手里或许也拿不住以太坊或者比特币。

而还有一部分人在比特币现货 ETF 通过之后认为已经 price in ,消息落地便不算利好,因此纷纷卖掉手中筹码埋伏下一个利好新闻,或许我们都低估了比特币现货 ETF 的力量。

面对 2 月春节以来比特币的疯狂涨幅,很多人甚至来不及反应比特币一下子拉出 10% 的涨幅。也有一部分人被以往的牛市经验所限制,犯了「恐高症」,都在等待一波大回调。

说这是牛市,毫无疑问比特币的价格是最好的证明,但这个牛市却又和以往不太一样。面对比特币单边行情,市场对于是否会出现山寨币牛市产生了分歧。

为什么只有比特币在涨?

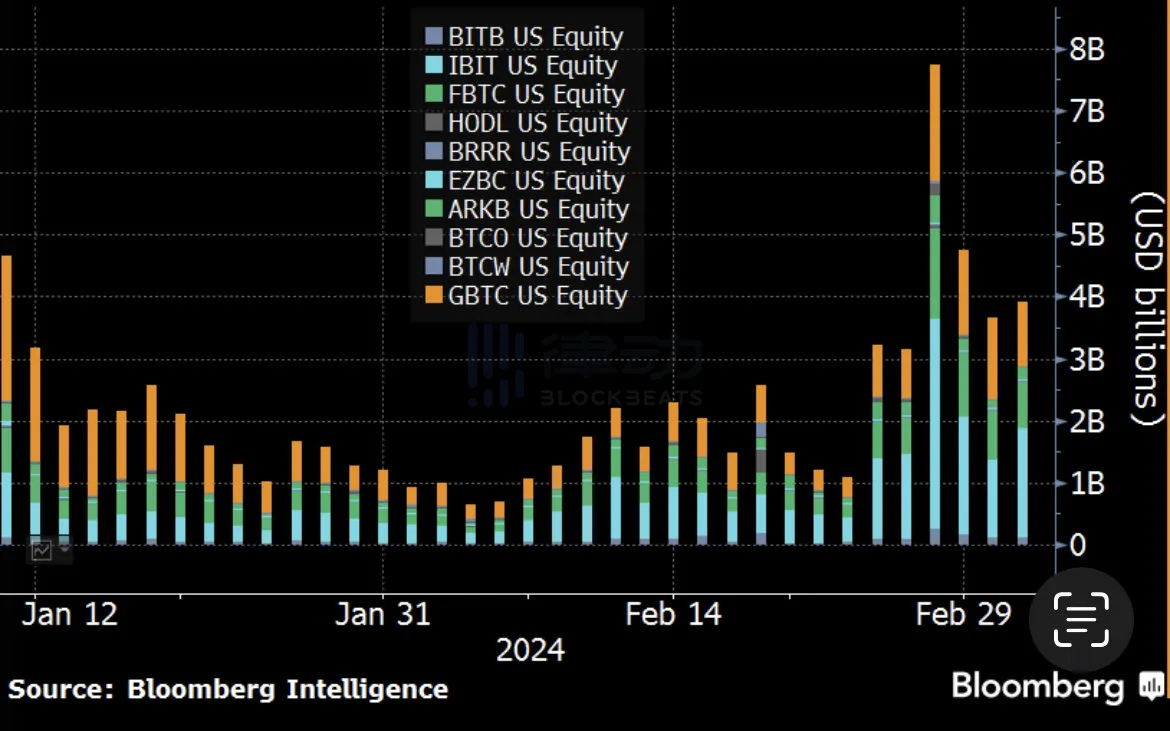

2 月 29 日比特币现货 ETF 单日交易量达 76.9 亿美元,创下发布以来的新历史记录,随后几天总体也都保持在 40 亿-50 亿的水平。比特币现货 ETF 的成交量不到两周内强势流入,使得比特币价格逼近历史新高。

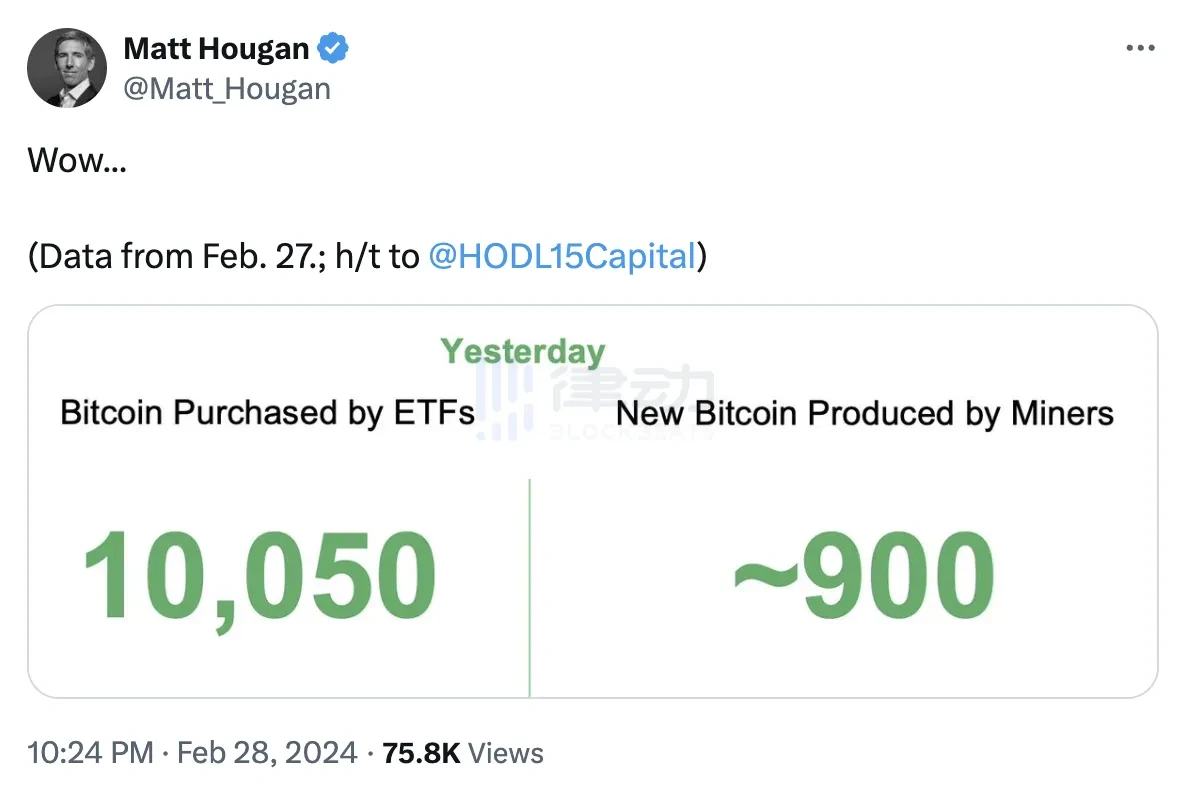

随着价格持续攀升,许多人都在寻找原因,最明确的答案是供需失衡。比特币现货 ETF 带来的强劲需求超越了矿工挖矿产出的比特币。

Alternative 数据显示,今日加密货币恐慌与贪婪指数为 90 (昨日为 82),为 2021 年 2 月以来首次达到 90 ,市场陷入极度贪婪情绪。市场情绪很热,但与之形成鲜明对比的是山寨币的价格低迷。

令人焦虑的地方在于,比特币价格一直涨,但山寨币价格纹丝不动甚至还在下跌。很多观点认为,流入比特币现货 ETF 的资金并不会流向场内的山寨币,而是会兑现为美元,因此导致这一轮不会有山寨币牛市。

在与 BlockBeats 的采访中,Matrixport 分析师 Markus 认为当前的市场可能只是比特币牛市,并不涉及山寨币。但 Markus 表示购买 ETF 的投资者并不这么认为,「这个牛市非常不同,上一个牛市是 DeFi summer,山寨币是主角,但这一次或多或少集中在比特币上。」

上一个周期,加密货币牛市发生在比特币市占率低于 48% 时,山寨币疯狂上涨;但目前比特币市占率为 50.19% 。Markus 还提到比特币的市场主导地位大约为 52% ,并认为如果山寨币要出现反弹,比特币的主导地位必须降到 50% 以下。

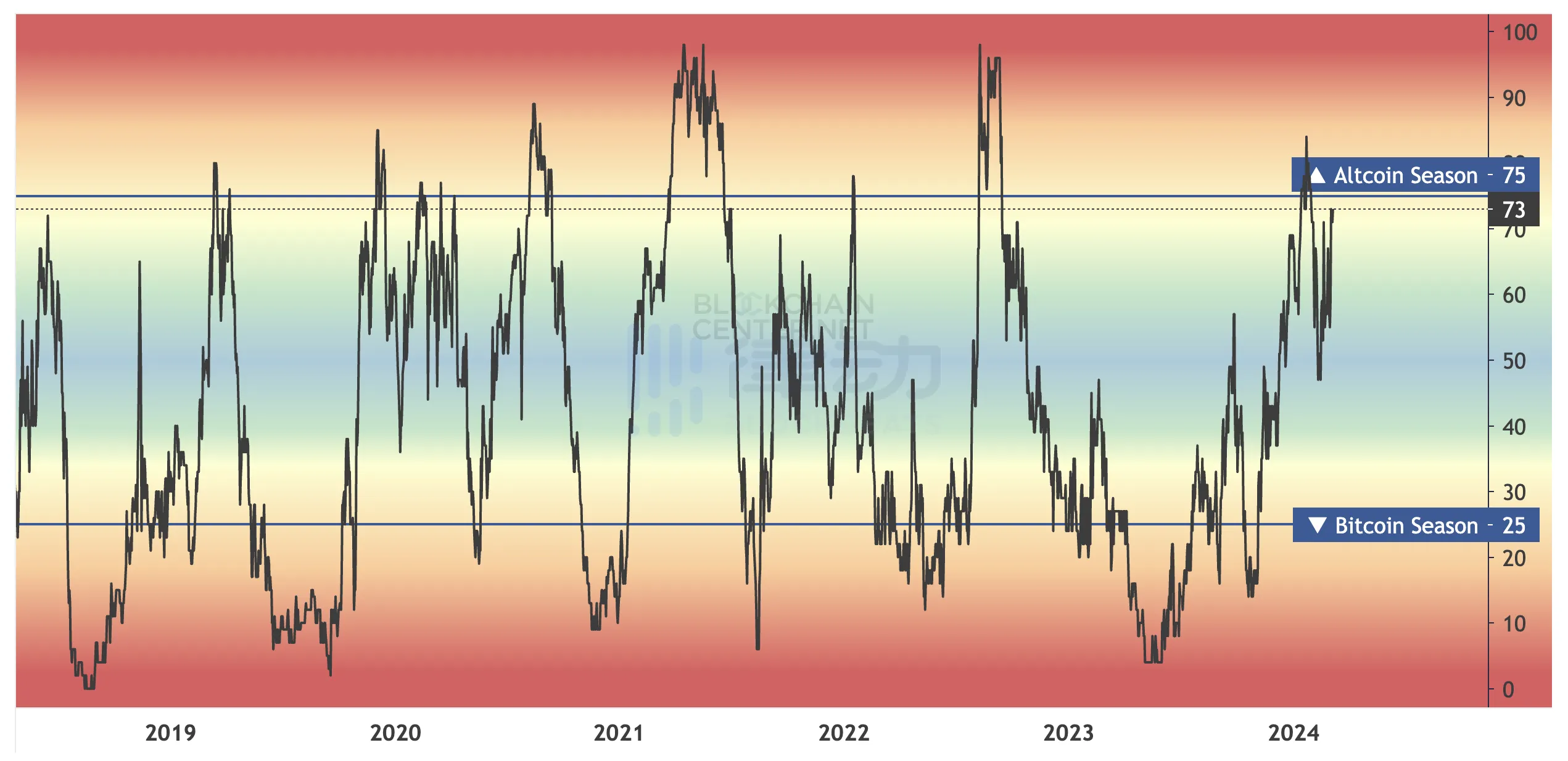

如果前 50 名代币中 75% 在 90 天的表现优于比特币,则为山寨币季节。据 BlockchainCenter 数据,目前的山寨币指数为 73 ,山寨季还未来临,但距离 75 的标准已经较为接近。

山寨币季节指数;图源:BlockchainCenter

尽管目前有许多声音认为本轮或是比特币牛市,难遇「狂暴」山寨季,但以太坊、Solana 等生态还是有一些事情值得期待。

还能有山寨季吗?

尽管昨晚 SEC 推迟了对 BlackRock(贝莱德)以太坊现货 ETF 申请做出决议,以太坊仍突破 3700 美元。据 8 marketcap 数据,以太坊市值达 4490 亿美元,超越万事达和埃克森美孚等公司,资产市值排名第 23 位。

今年以太坊最大的叙事再质押目前也只进行到了前半场, 2 月 22 日,a16z 向流动性再质押协议 EigenLayer 投资 1 亿美元,而 ether.fi、Renzo 等再质押赛道头部项目也接连获得融资。基础设施方面,除了再质押,模块化也依然被头部 VC 看好,Founders Fund 和 Dragonfly 领投了 Polygon 模块化区块链 Avail 2700 万美元种子轮融资,Jump Capital 领投了模块化区块链 Lava Network 1500 万美元种子轮融资。

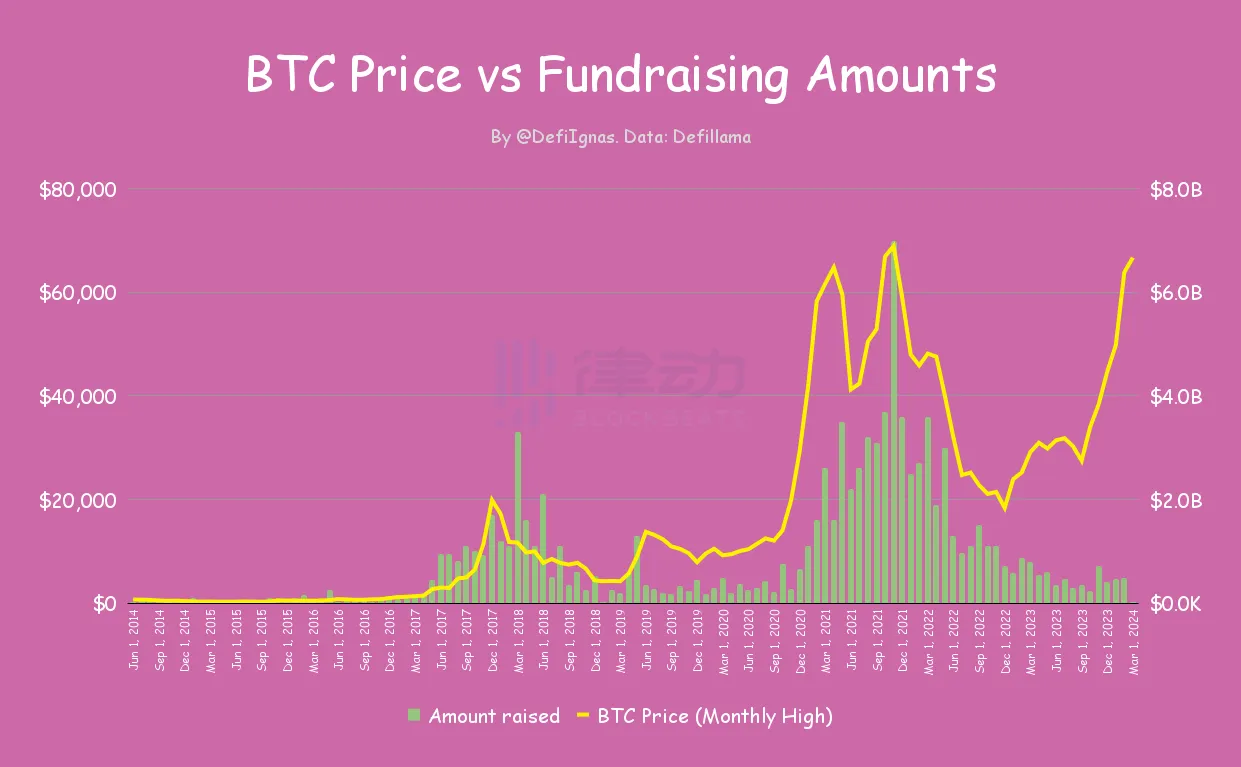

在之前的周期中,加密领域的融资数量都是紧随比特币价格的,但这一次并没有呈现相关趋势。据加密研究员Ignas分析,项目通常会在熊市期间筹集资金,然后选择在对他们来说更有意义时公布投资。但目前市场如此火热,「公布金额」仍然相对较低。这说明未来将会有更好的时机宣布融资新闻,因而更看好后市。

SOL 的价格在这波比特币强势行情中表现也不算差,除了以太坊,市场对于 Solana 的后续表现也持乐观态度。

2024 年将会上线由 Jump Crypto 开发的 Solana 第二个节点验证器 Firedancer,它有助于 Solana 一次处理更多的交易,目标是达到每秒一百万笔交易,这可能使 Solana 比许多传统支付系统(比如 Visa)更快。而 Solana 上的 AI、Depin 等项目也是其有竞争力的版块,在积分激励系统的催化下,接下来会有一批 Solana 生态项目上线并发布代币。

在撰稿期间,ENS、OP、STRK 等以太坊系代币价格突破上涨,乐观情绪进一步增强。比特币还未突破前高,未来仍然值得期待。