By Financial Story Collection, Author: Linda, Editor: Chen Jiying

OpenAI CEO Altman's house was set on fire.

Early Friday morning, a 20-year-old threw a Molotov cocktail at Altman's former residence in San Francisco. Fortunately, no one was injured.

An hour later, this reckless young man appeared outside the OpenAI office building, threatening to burn down the entire building. The suspect's social media account referenced the plot from the novel Dune, where humanity launches a holy war to destroy AI.

A visibly shaken Altman later unusually shared a family photo and wrote a lengthy post. He said AGI has become the 'One Ring,' and the real danger is not the technology itself, but the thought of 'becoming the one who controls AGI,' which can drive people to do extremely crazy things. He also publicly apologized for the first time for the 2023 board turmoil, admitting that his 'fear of conflict' personality had created a huge mess for the company.

This company just completed the largest single round of private fundraising in human history: $122 billion, with a post-money valuation of $852 billion. On one side, some want to burn it down; on the other, some are pouring in hundreds of billions of dollars. Fear and greed have never been so starkly juxtaposed around a single company.

The institutions providing the funds have their own calculations. Amazon committed $50 billion, but not all at once—$15 billion is immediate, with the remaining $35 billion conditional on OpenAI completing an IPO or achieving Artificial General Intelligence (AGI) by the end of 2028. Nvidia and SoftBank each invested $30 billion, to be disbursed in batches by July and October 2026, respectively. Microsoft followed on with an investment, but the specific amount was not disclosed. Top-tier institutions including a16z, Sequoia, BlackRock, Blackstone, Thrive Capital, and over 20 others all entered the fray.

Amazon and Nvidia are not putting all their eggs in one basket; they are also investors in Anthropic, OpenAI's biggest competitor.

Amazon poured tens of billions into Anthropic, deeply integrating the Claude model with AWS; then it turned around and wrote a $50 billion check to OpenAI. The logic of betting on both sides is clear: it's not about betting on who wins, but ensuring you have a seat at the table no matter who wins.

Cash-rich Nvidia's $30 billion investment in OpenAI will ultimately flow back into its own pockets in the form of GPU purchase orders. This resembles a prepaid chip sales contract more than a traditional investment.

OpenAI also did something unprecedented: for the first time, it opened subscription to individual investors through banking channels, raising over $3 billion from retail investors. ARK Invest also announced it had purchased $240 million worth of OpenAI shares through several of its ETFs. A company not yet public is already making comprehensive preparations for an IPO.

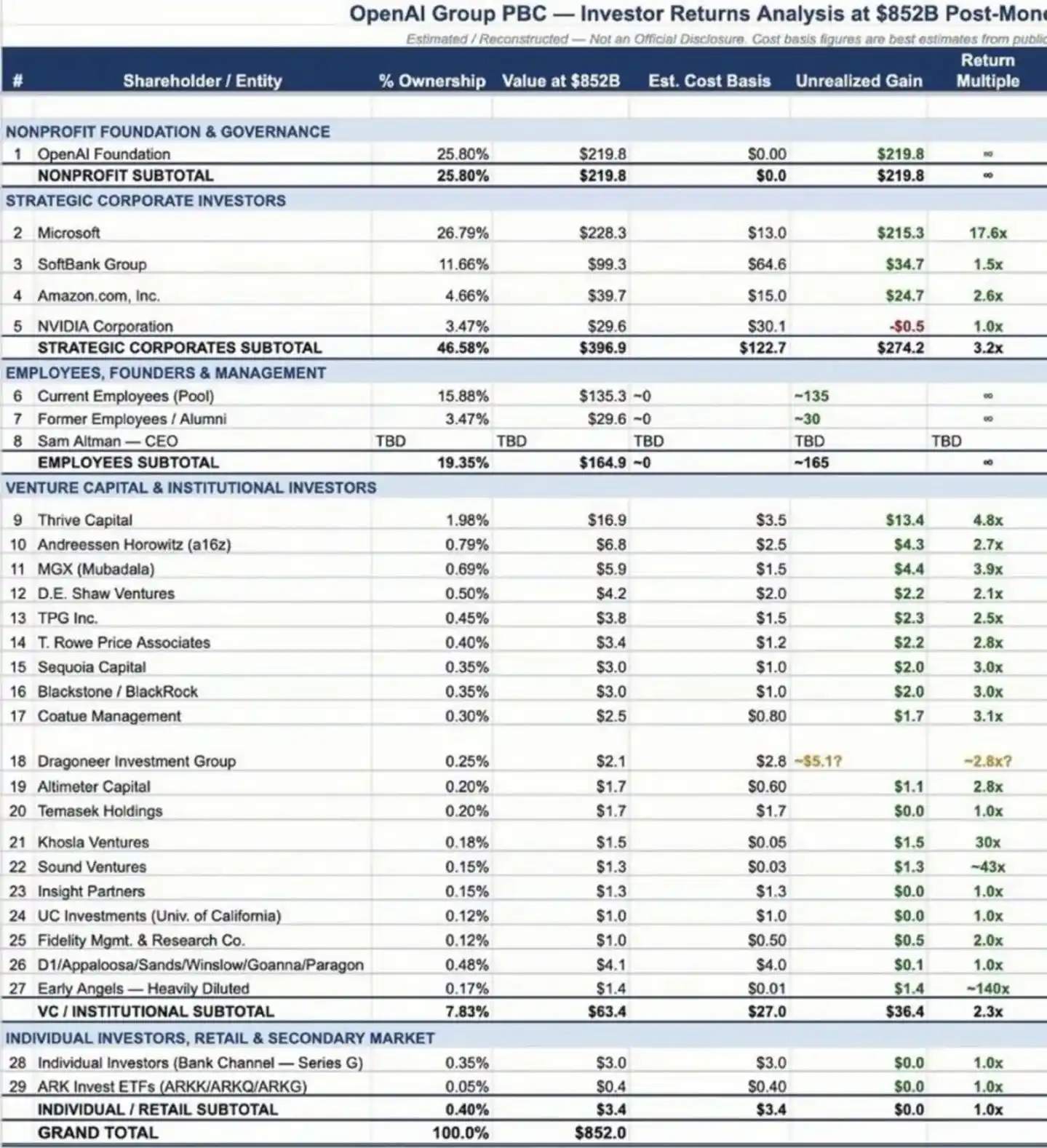

But after $122 billion is poured in, whose pockets does this money ultimately end up in? Just as the financing news was announced, a cap table was leaked.

A Leaked Cap Table

This equity structure table, allegedly from inside OpenAI, laid out the first clear picture of the company's ownership distribution.

The top five shareholders are: Microsoft 26.79%, OpenAI Foundation 25.8%, SoftBank 11.66%, Amazon 4.66%, and Nvidia 3.47%. Current and former employees collectively hold approximately 20%.

Microsoft is the biggest winner on this list. Starting with its first $1 billion investment in 2019, followed by $10 billion in January 2023, and another $2 billion top-up in 2024, Microsoft has invested approximately $13 billion cumulatively into OpenAI. Based on the current $852 billion valuation and its 26.79% stake, this $13 billion is now valued at $228.3 billion on paper, a return multiple of over 17 times. This might be one of the single most profitable bets in the history of tech investing. Microsoft's advantage was getting in early; when it made its first investment in 2019, ChatGPT didn't exist, and the term 'large language model' was almost unheard of outside academic circles.

Looking at other players. SoftBank's $64 billion investment (likely a typo in original, context suggests a large sum) is currently valued at approximately $99.3 billion on paper, a paper return of about 1.5x. This number might not seem exciting for a simple reason: SoftBank got in when the valuation was already high. By the same logic, Amazon and Nvidia are entering at an even higher price in this round. They are betting not on short-term returns but on strategic positioning in the AI infrastructure layer.

But the most striking number on this table is not Microsoft's $228.3 billion, but another number—zero. OpenAI's CEO, Sam Altman, holds zero shares. This leads to the most dramatic thread in the entire OpenAI story.

CEO Holds Zero Shares

A company valued at $852 billion, and the CEO holds not a single share. His annual salary is $76,001, which, according to Altman, is the 'minimum wage to qualify for health insurance.'

Altman's explanation for this has always been candid. At the New York Times DealBook summit last December, he said this was his 'dream job since childhood,' and 'being in a room with the smartest researchers in the world, participating in this crazy adventure, is worth more to me than any extra money.' But then he said something even more intriguing: 'If I could go back, I would take some equity, even just a little bit, so I wouldn't have to answer this question forever.'

Not taking equity was initially an active choice. When OpenAI was founded in 2015 as a non-profit, managers holding equity would affect its tax-exempt status. Altman himself has stated that he needed to prove to the outside world that he could separate personal利益 (interests) from the company's mission. But as the company's valuation grew from zero to $852 billion, the cost of this 'active choice' became increasingly high.

Zero shareholding implies governance risks. In 2023, the OpenAI board suddenly ousted Altman. In a normal company, the CEO is usually one of the largest shareholders, making it difficult for the board to fire him without his consent. But Altman had no equity voting rights on the board; his CEO position relied entirely on the trust of the directors. Later, under pressure from Microsoft and employees, Altman was reinstated, but this incident served as a reminder that a CEO without equity is extremely vulnerable in the governance structure.

Reflecting on this event later, Altman said he 'learned a lot about communication during a crisis,' but also felt for the first time a sense of pride that 'the team could operate without me.'

There has been external speculation that Altman would eventually receive equity. In September 2024, Bloomberg reported that the OpenAI board was discussing granting Altman a 7% stake. Subsequently, Altman denied this at an all-hands meeting, saying there were 'no plans to receive a huge equity grant' and that the media-reported number was 'way off.'

But both he and CFO Fryer admitted one fact: investors were concerned about him not holding equity because they want the CEO's interests aligned with theirs. Board Chairman Bret Taylor confirmed to the media around the same time: the board had indeed discussed the matter but hadn't discussed specific numbers.

By October 2025, after the company completed its transformation, Altman took to social media again to discuss the topic, his tone more candid than before: 'I wish I had taken equity long ago; it would have saved a lot of conspiracy theories.' He also said the initial decision not to take equity was 'dumb, trying to express 'I already have enough money.'' The change in wording from 'active放弃 (abandonment)' to 'dumb move' speaks volumes. And the 'transformation' Altman referred to is the biggest change OpenAI underwent in the past year.

From Non-Profit to Nearly Trillion-Dollar Valuation

On October 28, 2025, OpenAI completed its transformation from a non-profit to a for-profit company. This nearly year-long restructuring aimed to solve a fundamental contradiction: a company that needs to burn through hundreds of billions of dollars could no longer continue raising funds under a non-profit structure.

The new structure is as follows: the original non-profit entity became the 'OpenAI Foundation,' holding a 26% stake in the for-profit subsidiary 'OpenAI Group PBC,' valued at approximately $130 billion. Microsoft received a 27% stake, worth $135 billion. The Foundation's board holds 'special voting rights' and can appoint and remove all directors of the PBC. California Attorney General Rob Bonta commented on this plan, saying it 'ensures that charitable assets are used for their intended purpose, safety will be prioritized, and OpenAI will remain in California.' The subtext of this statement is: without these promises, the Attorney General might have taken this plan to court.

But there is no lack of external skepticism. Johnston, head of the non-profit oversight organization Midas Project, pointedly noted: the board members of the Foundation and the PBC are almost entirely overlapping, and the non-profit's oversight power is essentially reduced to 'the power to fire themselves.' This criticism touches the core contradiction of the entire transformation: when mission and profit conflict, will a dual structure managed by the same group of people truly forsake self-interest for public good?

The transformation is complete; the next step is an IPO. And the IPO timeline is becoming an increasingly public point of divergence within OpenAI.

According to The Information, Altman hopes to go public as early as the fourth quarter of this year, but CFO Fryer has privately expressed concerns. She believes conditions are not ripe for an IPO in 2026, as process and organizational preparations are not yet complete, and there are risks associated with massive spending commitments.

Amid this disagreement, it is reported that Altman has begun excluding Fryer from some financial planning discussions. Such a rift between the CEO and CFO is not a good sign for a company preparing to go public.

External competitive pressure is also intensifying. Anthropic is also considering an IPO by the end of 2026, expected to raise over $60 billion. If Anthropic lists first, it would siphon off a wave of market enthusiasm for AI stocks. Therefore, for OpenAI, an IPO is not just a financing need but also a race against time. And the finish line of this race points to a question everyone is asking.

Is $852 Billion Worth It?

Is OpenAI really worth $852 billion?

First, look at revenue. According to Reuters, citing Fryer's statements earlier this year, OpenAI's current monthly revenue is $2 billion, annualized to approximately $250 billion (Note: This seems like a potential mistranslation/error in the original Chinese. $2B monthly is $24B annual, not $250B. The original likely said 年化约240亿 or similar, mistyped as 250亿. The PS ratio calculation below also suggests $24B annual revenue is intended. Will proceed with $24B for calculation consistency). ChatGPT has over 900 million weekly active users, over 50 million paid subscribers, and enterprise revenue already accounts for over 40% of total revenue. The advertising pilot generated over $100 million in annualized recurring revenue within six weeks. In terms of growth rate alone, OpenAI is indeed growing faster than Google or Meta did at a comparable stage.

A $852 billion valuation against $24 billion (adjusted, see note above) in annualized revenue gives a price-to-sales (P/S) ratio of approximately 35.5x. If calculated against the trillion-dollar valuation expected by the market for a year-end IPO, the P/S ratio would be even higher. For comparison, Nvidia's P/S ratio never exceeded 40x even at its most frenzied, and Nvidia was actually profitable, whereas OpenAI is expected to lose $14 billion this year (Note: Original says 140亿, assumed $14B).

The pressure on the cost side is equally astounding. According to The Information, OpenAI's computing power investment plan for the next five years amounts to a staggering $600 billion, and it is not expected to achieve positive cash flow until 2030, during which time it will lose over $200 billion more. Meanwhile, its API pricing remains several times higher than its rivals. Once a price war breaks out, revenue growth will come under pressure, while computing支出 (expenditure) is rigid.

Revenue is elastic; costs are rigid. This is a dangerous signal.

Pulling the focus back to China, the contrast is even stronger. Since the beginning of 2026, AI financing in China also looks hot: Moonshot AI raised $700 million, StepFun completed a Series B+ round of 5 billion RMB, setting a new record for single-round financing in domestic large models. But if you total the historical financing of all major Chinese AI model companies, it probably only amounts to the loose change from OpenAI's single round. This is not just a question of a technology gap; the capital structure is completely different.

AI financing in the US is essentially an arms race among tech giants. Amazon invests $50 billion to sell cloud services; Nvidia invests $30 billion to sell chips; SoftBank invests $30 billion to push its own Stargate project—the money goes full circle back to the investors.

AI financing in China is still dominated by VCs and local industry funds; it hasn't formed this kind of 'investment equals procurement' closed loop. When one side is fighting a war using the balance sheets of giants, and the other is still seeking financial investors round by round, the capital foundation of this competition is different from the starting point.

So what exactly is the $852 billion buying? Altman himself provided the answer. He wrote in a blog post: 'We are now very confident; we know how to build AGI.' He also said that by 2035, every person on Earth should be able to mobilize cognitive能力 (capability) equivalent to the total intellectual sum of all humanity in 2025.

This is the vision investors are betting on. If AGI truly arrives, all of today's numbers will be rewritten, and $852 billion will seem cheap. If it doesn't come, or comes slower than expected, today's valuation is a massive bubble. This $122 billion is betting not on a company's financial statements, but on the endgame of AI.

Conclusion

From its founding as a non-profit lab in 2015 to its $852 billion valuation and IPO sprint in 2026, OpenAI has traveled a path in 11 years that most companies never complete in a lifetime. In these 11 years, it transformed from an idealistic research institution into the most funded commercial company in history, experienced the drama of the CEO being fired and reinstated, completed the legal transformation from non-profit to for-profit, and its leader still hasn't received a single share.

The problems facing this company have no ready-made answers. The divergence between the CEO and CFO over the IPO timeline has surfaced. It needs to burn $600 billion over the next five years; once revenue growth slows, it will become被动 (passive). A 'non-profit controls for-profit'架构 (structure) managed by the same group of people has not yet been tested by a real conflict of interest.

Altman once predicted, 'Approaching the singularity; not sure on which side.' The $122 billion bet has been placed. The answer will take years to reveal itself.