Author: Frank, PANews

Original Title: Pump.fun Joins the Billion-Dollar Club, How Much Business Does the "MEME Cash Machine" Have Left?

On March 8, Pump.fun's cumulative revenue exceeded $1 billion, making it the first platform on Solana to reach this milestone and solidifying its position as the most prominent money printer in the MEME sector. However, after the hype subsided, the question is no longer just "who made the most money," but rather how much business these MEME-driven platforms still have left.

Looking at top ecosystem projects like Pump.fun, GMGN, Four.meme, Axiom, as well as Photon, BullX, and BONK, the answer is becoming increasingly clear: MEME hasn't disappeared, but the business is increasingly concentrated among the top players, and the divergence between chains and platforms is becoming more pronounced.

Pump.fun: The "Absolute Oligarch" Across Bull and Bear Markets, Billions in Profits but Hard to Retain

If the last wave of MEME frenzy was a non-stop gold rush, then Pump.fun was undoubtedly the most profitable toll booth in this gold rush town. Public data shows that as of March 2026, Pump.fun's cumulative total revenue has exceeded $1 billion. Of this, 2024 contributed approximately $321 million, and 2025 further increased to about $664 million. Starting in 2026, the MEME industry experienced a significant downturn, but Pump.fun seemed relatively unaffected, still generating about $98.3 million in revenue to date.

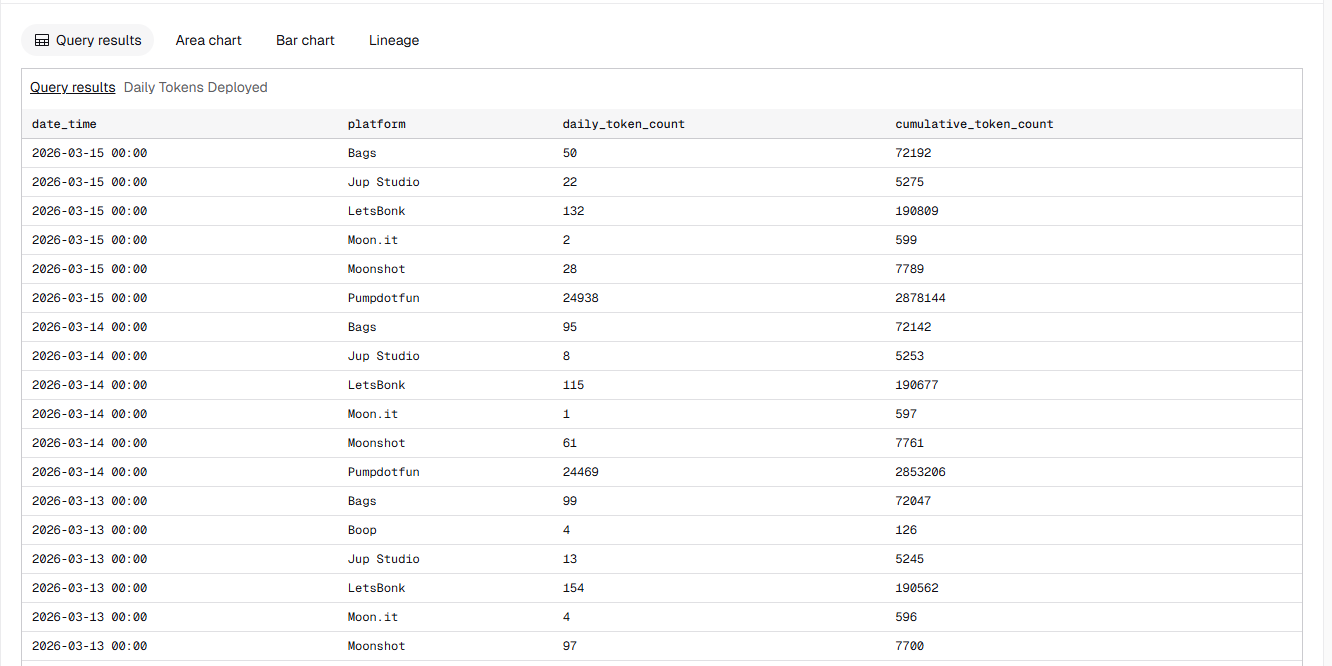

In terms of market structure, Pump.fun's dominant position in the Solana ecosystem has further strengthened. Taking data from March 15 as an example, Pump.fun's token creation share reached 99.1%, the graduation rate of tokens was 94.8%, and its daily trading volume share was about 93%. That day, Pump.fun launched 24,938 tokens, while LetsBonk had only 132, Bags had 50, and Moonshot had 28. The daily volume of other token launch platforms is no longer competitive with Pump.fun.

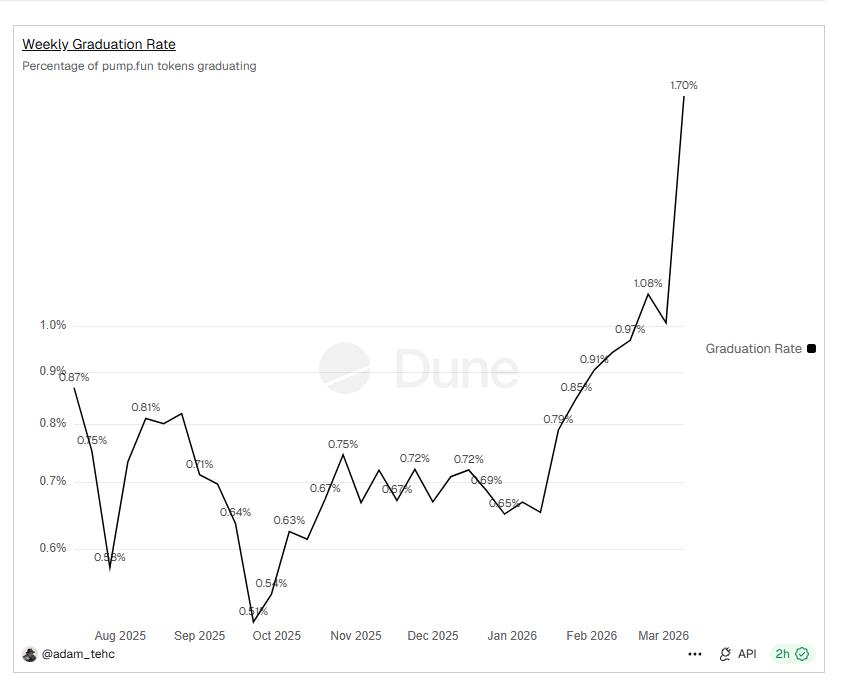

Looking back at Pump.fun's own data, it has also maintained a surprisingly high standard. Rough calculations based on visible data from the past two weeks show that Pump.fun currently averages about 29,700 token launches per day, with approximately 157,700 daily active wallets, a daily trading volume of about $93.65 million, and daily revenue of about $870,000. At the same time, the graduation rate, long seen as a weakness of the platform, has shown signs of recovery, recently even surging to around 1.70%. Although the specific reason behind this short-term peak is not yet clear, Pump.fun's graduation efficiency is indeed improving.

However, although fee generation remains robust, for Pump.fun, it does not mean that all this revenue can be fully converted into protocol profits. First, more than half of the fees are given to creators and LPs. Second, the remaining revenue is also used for token buybacks. In the first quarter of 2026, Pump.fun generated a total of $227 million in fees, of which $123 million was distributed to creators and LPs, and the remaining $100 million was almost entirely used for token buybacks.

The problem is that the buybacks did not automatically translate into a rise in token price. As of March 16, the price of PUMP was about $0.002, still about 76.21% lower than its all-time high of $0.0088. A more reasonable explanation is that buybacks can only provide support and maintain the narrative but are insufficient to reverse the overall compression of valuations in the MEME sector. In other words, Pump.fun's cash flow machine is still running at high speed, but the market is no longer willing to give it higher valuation multiples simply because it "makes money," as it did during the last hype cycle.

In summary, for Pump.fun, the market structure remains relatively stable. Although the entire meme coin sector is experiencing a decline, it's mostly the competitors that have died off,反而 making Pump.fun's dominance even stronger. If this market can explode again, Pump.fun is likely to capture even greater红利.

GMGN: Quarterly Revenue Grows Fivefold, BSC Becomes the "New Traffic Hotspot"

GMGN's revenue saw another explosive growth in the first quarter of 2026. Total revenue for Q1 2026 reached $25.31 million, a nearly fivefold increase compared to $5.64 million in Q4 2025. This quarter's revenue also became the second-highest quarterly revenue in GMGN's history (only lower than Q1 2025's $40.81 million).

A closer look at this revenue structure shows that it is mainly driven by the BSC chain. Starting in October 2025, GMGN's trading volume on the BSC chain began to significantly exceed that on Solana, and by 2026 this trend had stabilized. To date, the trading share on the BSC chain on GMGN is nearly three times that of the Solana chain.

From an overall trading volume perspective, user activity and trading volume on GMGN improved somewhat in Q1 2026, but the increase is not as high as the revenue change suggests. Therefore, from this angle, the revenue improvement in Q1 2026 is real, but the explosive growth is likely a statistical issue with DefiLlama (BSC chain revenue data was empty before October 2025).

However, this growth was primarily driven by a surge in MEME trading volume on the BSC chain in January, which generated $16.34 million in cross-chain revenue that month. This number dropped to $5.18 million in February and is about $3.77 million so far in March. The overall level for Q1 this year is similar to that of the same period in 2025.

Four.meme: The "Face" of BSC, Daily Revenue Only a Fraction of Its Peak

If Pump.fun has almost absorbed most of the traffic on Solana launch platforms, then on BSC, the closest to a similar role is Four.meme.

DeFiLlama data shows that as of March 16, Four.meme's protocol revenue for Q1 2026 has reached $16 million, significantly lower than the $54.24 million in Q4 2025. However, looking at the monthly revenue changes this year, there has been a slight recovery.

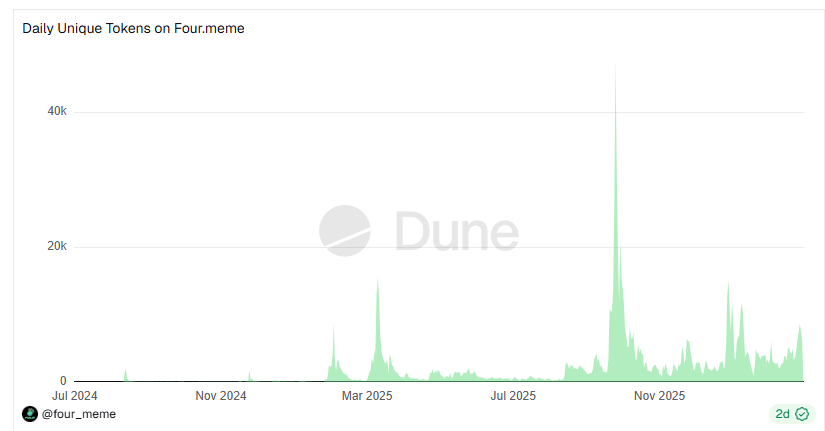

According to visible data tracked by Dune for the last 10 days, Four.meme averages about 4,858 token launches per day, with approximately 5,749 daily users. Only about 25.7 tokens are listed on the DEX Pancake daily, and the short-term graduation rate has further dropped to around 0.53%. Judging from these data changes, the current Four.meme is also operating at a low level. Compared to the peak daily revenue of $4.22 million in October 2025, current revenue has fallen to the $200,000-$300,000 level.

For comparison, estimates based on Pump.fun's data from the past two weeks show it still averages about 29,700 token launches per day and a daily trading volume of about $93.65 million. Clearly, as the main platforms for MEME coins on Solana and BSC respectively, there is a significant gap in scale and token quality between Four.meme and Pump.fun, reflecting the development of MEME on these two chains.

Axiom: Farewell to High Growth, Stuck in a Continuous Volume Contraction Quagmire

If GMGN's growth in Q1 2026 was more like catching the红利 of the BSC rotation, then Axiom's situation is almost the opposite.

According to DeFiLlama data, as of now, the protocol's revenue in Q1 2026 is approximately $29.03 million, higher than GMGN's $25.31 million for the same period.

However, Axiom's current problem is that its business is in a state of continuous decline. According to DeFiLlama's quarterly revenue data, Axiom's protocol revenue reached highs of $133 million and $150 million in Q2 and Q3 2025 respectively, but fell to $60.66 million in Q4 2025, and is currently $29.03 million for Q1 2026. Compared to the most疯狂 phase last year, the business volume has significantly contracted. Comparing this with GMGN reveals that although both are in a post-peak decline phase, GMGN's revenue still has occasional阶段性 rebounds, while Axiom seems unable to regain its momentum.

For Axiom, it is no longer just a tool reliant on MEME hype bursts but更像是一台经历过多轮行情检验的成熟交易机器 (more like a mature trading machine that has been tested through multiple market cycles). Compared to GMGN, which is still talking about growth elasticity, Axiom's imagination space seems to be shrinking.

Photon, BullX, and BONK: The "Stragglers" After the Tide Recedes

Compared to GMGN, which still has rebounds, and Axiom, which maintains a leading scale, the revenue curves of Photon, BullX, and BONKbot have more clearly entered a downward trend in 2026.

According to DeFiLlama data as of March 16, Photon's cumulative revenue is approximately $438 million, but its quarterly revenue has declined from $122.8 million in Q1 2025, to $32.31 million in Q2, $18.99 million in Q3, $5.29 million in Q4, and is only $4.52 million so far in Q1 2026, showing a nearly阶梯式坠落 (stepped decline) trend.

BullX's cumulative revenue is about $203 million, but it also experienced rapid contraction. Quarterly revenue dropped from $87.37 million in Q1 2025 to $14.25 million in Q2, $3.86 million in Q3, $878,000 in Q4, and is only $491,000 so far in Q1 2026.

BONKbot's decline is relatively less steep but has also clearly receded. According to DeFiLlama data, its cumulative revenue is about $93.57 million. Quarterly revenue was $12.61 million in Q1 2025, then fell to $3.40 million in Q2, $2.85 million in Q3, $1.85 million in Q4, and is $1.84 million so far in Q1 2026.

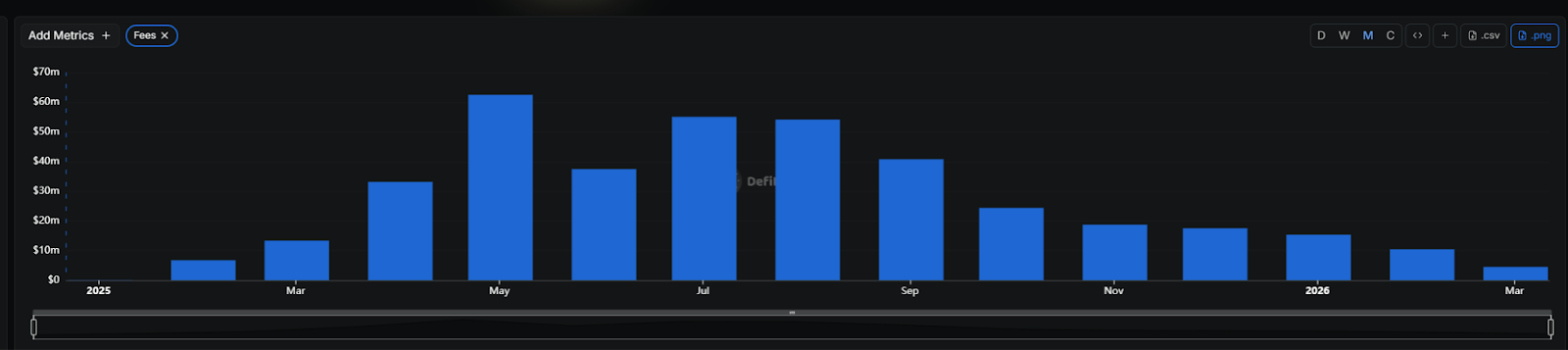

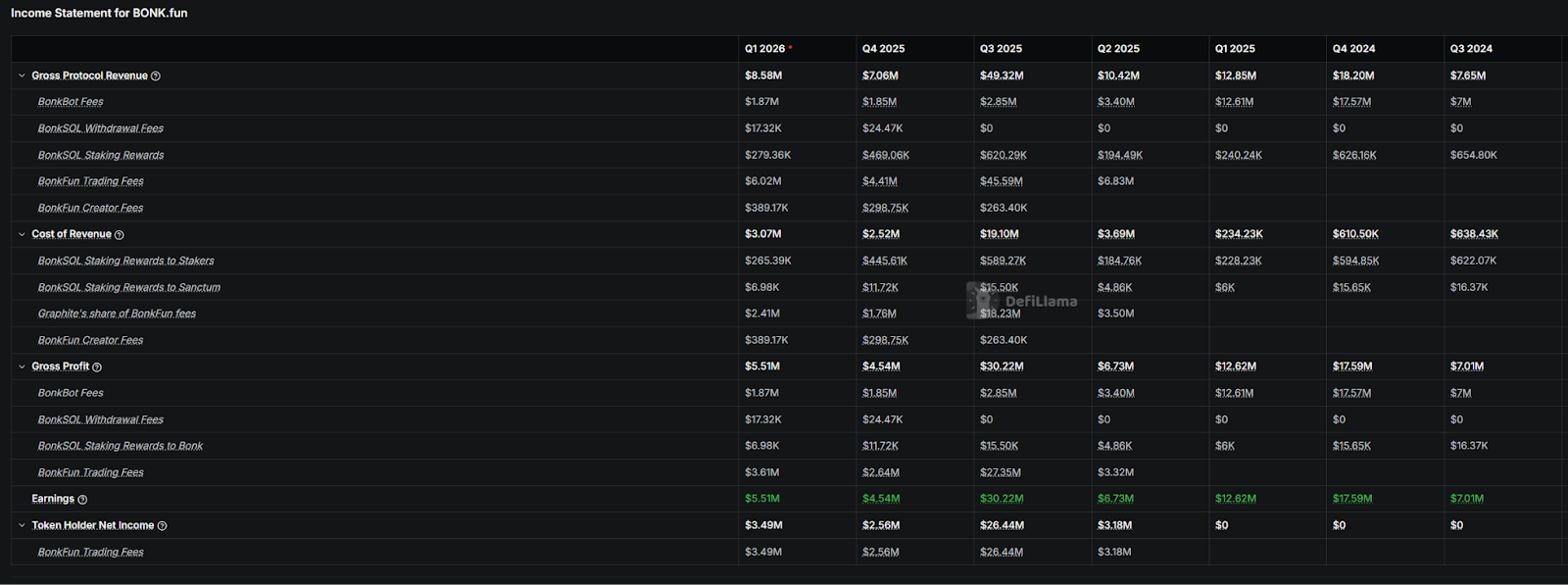

However, the BONK ecosystem itself has not simultaneously熄火 (fizzled out). As of now, BONK.fun's protocol revenue for Q1 2026 is approximately $8.51 million, already higher than the $7.06 million in Q4 2025. Of this current quarter's revenue, about $6 million comes from Bonk.Fun, and about $1.84 million comes from BonkBot.

Looking at this MEME coin battle royale, it's not hard to draw a conclusion: the MEME track is not dying out; it's just that the era of wild competition has彻底终结 (completely ended), and the reshuffling speed has far exceeded everyone's expectations.

After the tide receded, the platforms that truly remained are no longer just the fastest runners but those that have built a complete closed loop encompassing launch, trading, liquidity, and fee collection. If the next wave of MEME行情 (market trend) starts again, they are most likely the ones to benefit first.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush