Dogecoin’s [DOGE] on-chain activity has expanded sharply lately. And yet, the price action stayed muted, establishing a clear imbalance between flow and valuation. Transfer volume climbed to 1.037 billion DOGE, roughly $97.8 million, while the price held near $0.094 with gains of only 0.3%.

As this divergence developed, the transaction count increased to 26,627 alongside 32,915 active addresses, reflecting rising network engagement. However, the price failed to respond in tandem, shifting attention towards the composition of these flows.

The high volume is more likely a sign of redistribution, exchange routing, or internal wallet movements than accumulation. As activity intensifies without directional follow-through, the gap between volume and price will only widen.

This pattern also suggested that raw on-chain expansion, when unadjusted for internal transfers, does not quite confirm genuine demand or sustained buying pressure.

Whale flows signal distribution behind Dogecoin’s volume spike

As transaction volume cools down, whale flows can help clarify why the price has been unresponsive. Transfers above $90 million moved into Bitget-linked wallets within 24 hours, signaling distribution into available liquidity.

As these flows hit exchanges, they increased immediate sell pressure, which absorbed incoming demand rather than pushing the price higher.

Meanwhile, top-100 holders still control over 66% of supply, translating to approximately 101.99 billion DOGE, without expanding balances, reinforcing the absence of accumulation. This behavior implied a late-cycle rotation, where large players offload into retail-driven activity. As supply met demand at these levels, the price stabilized near $0.094 instead of breaking out.

However, since holdings have been concentrated, the downside stayed controlled, leaving DOGE range-bound until either accumulation resumes or sell pressure intensifies.

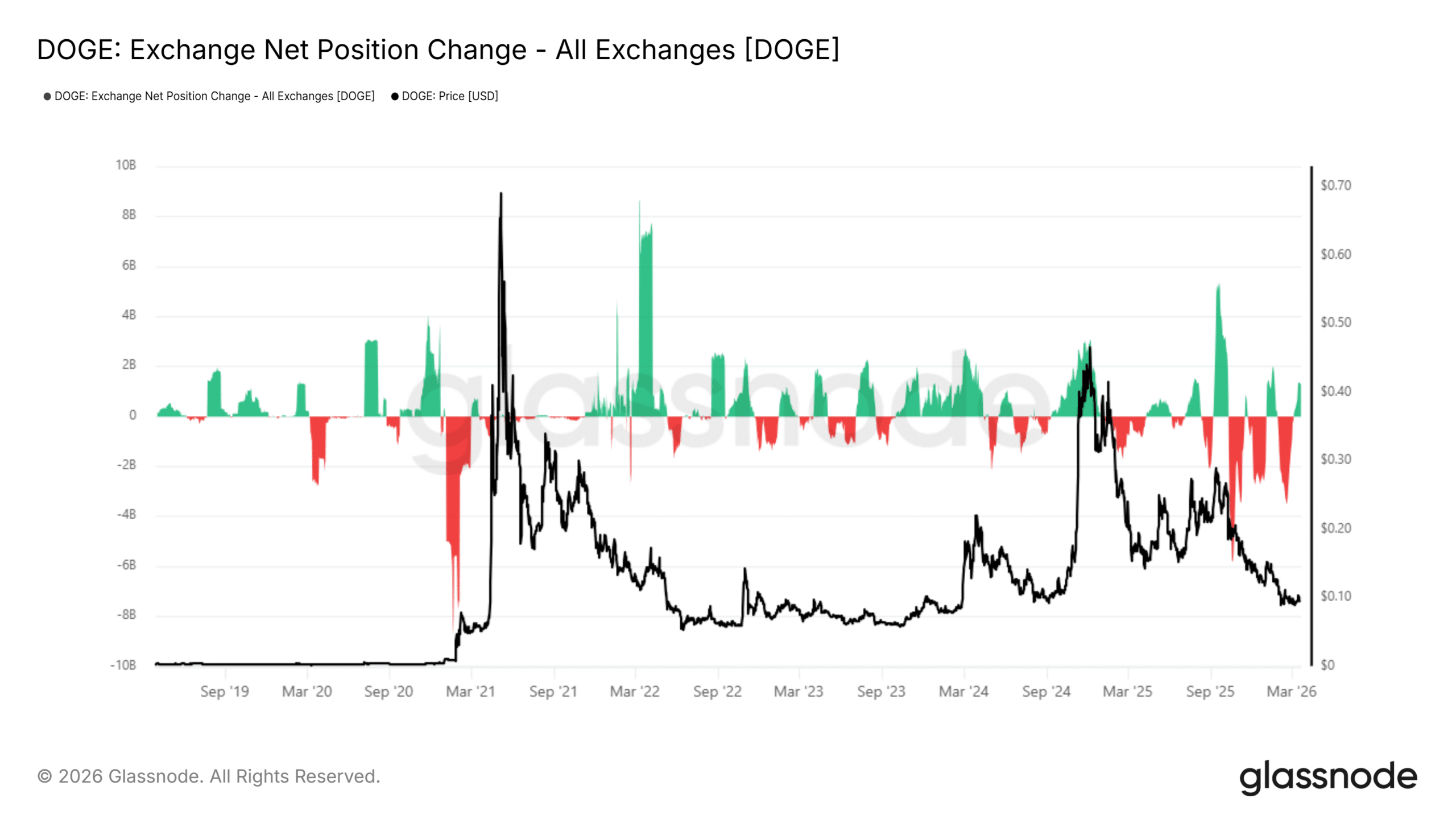

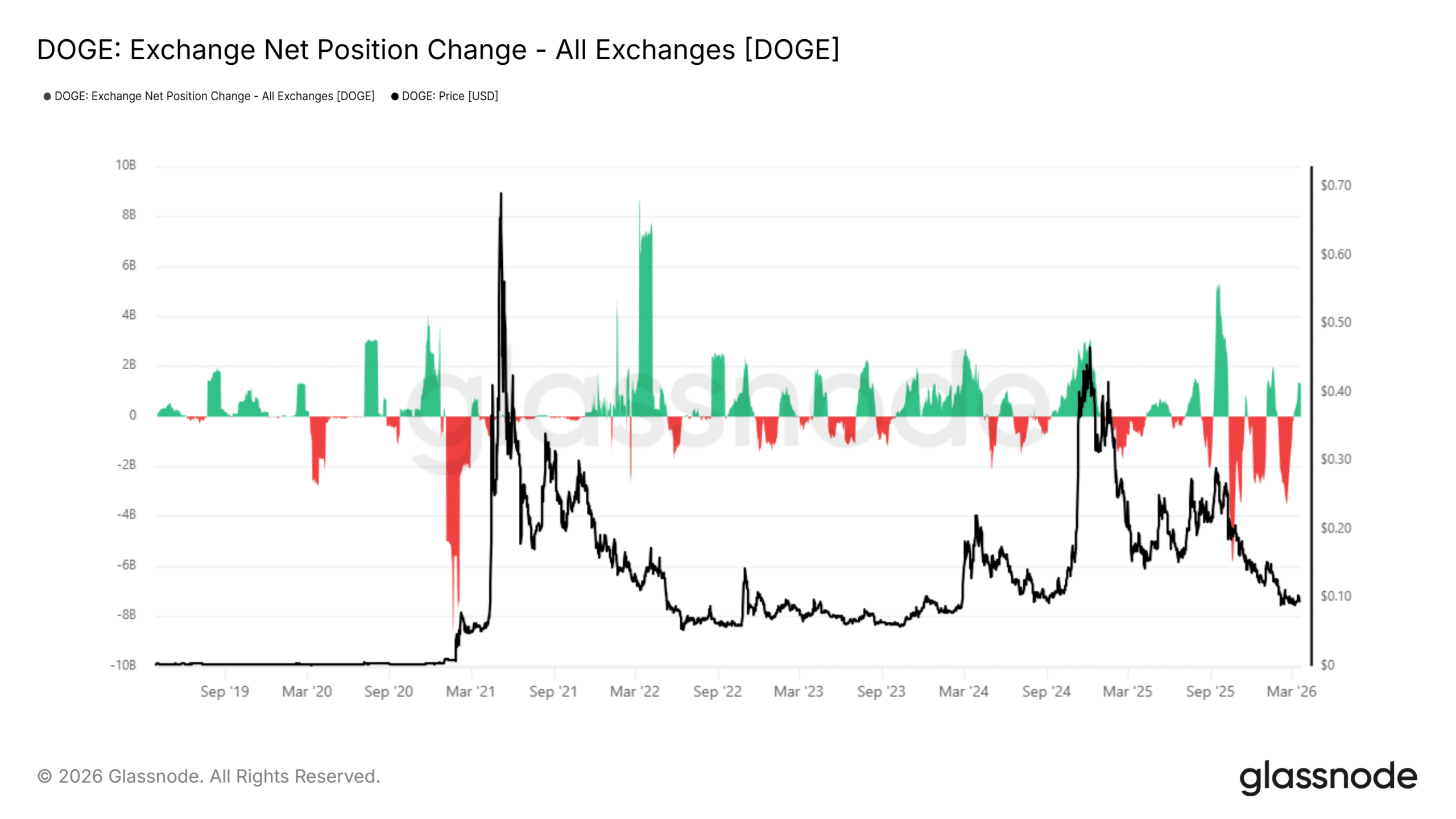

Exchange flows keep Dogecoin range-bound

Exchange flows add context to the redistribution narrative. For example – The Net Position change showed repeated spikes above 4 billion DOGE, reflecting strong inflows into exchanges during key periods.

As these inflows rise, the price often stalls or declines, reinforcing sell-side pressure. More recently, persistent negative flows hinted at intermittent outflows – Indicative of periods of absorption or accumulation.

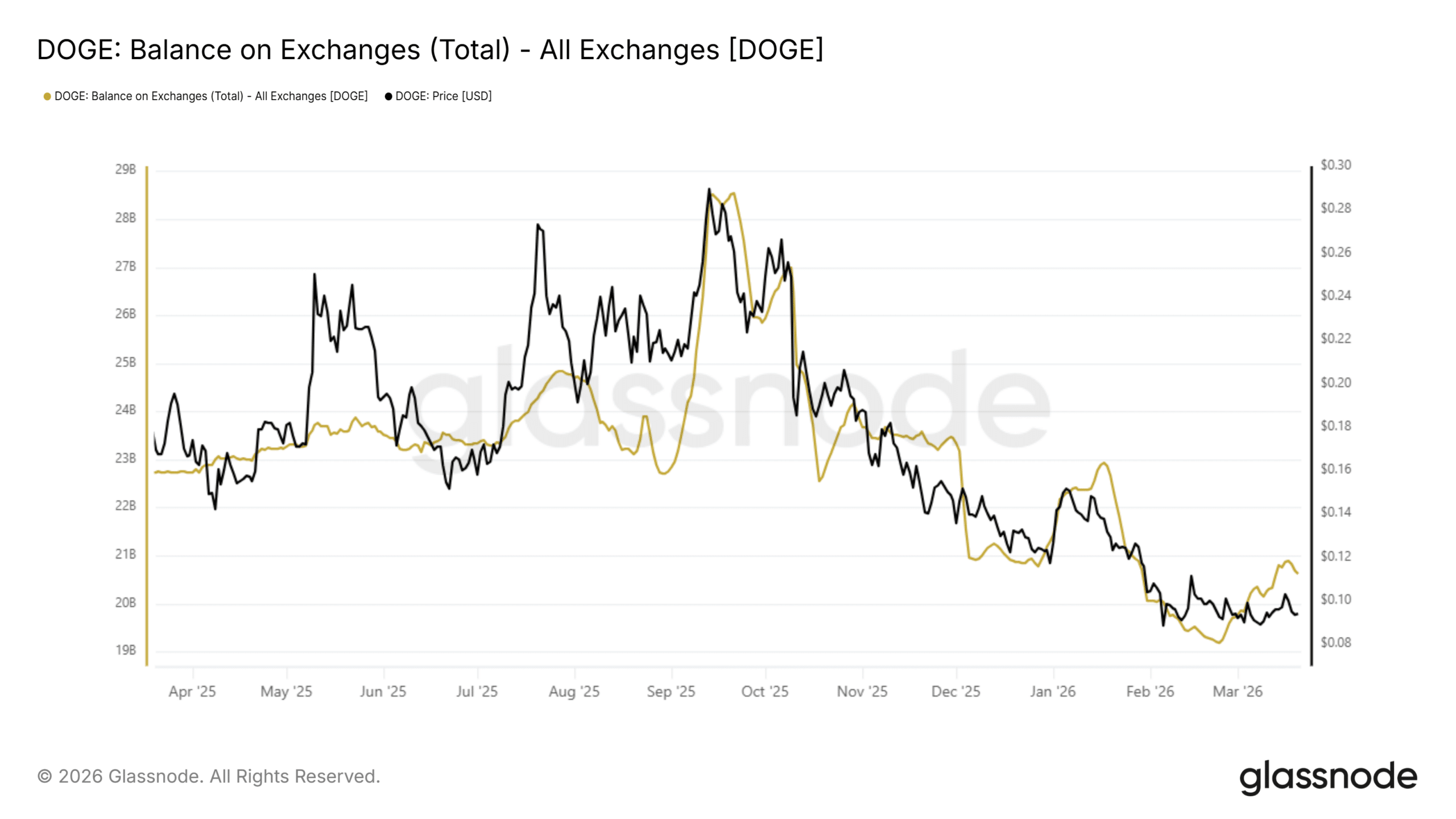

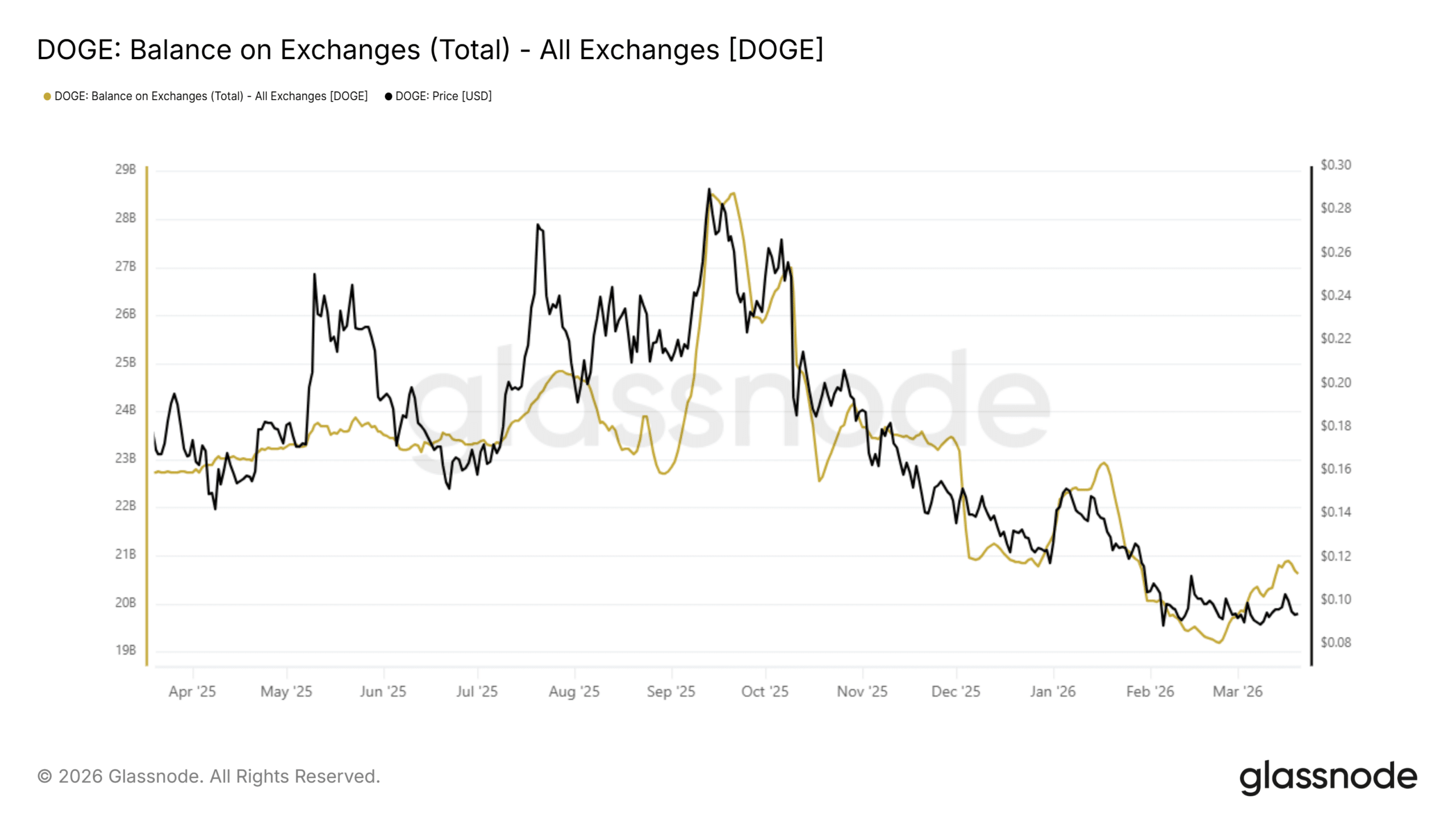

At the same time, total Exchange Balances declined from nearly 29 billion DOGE in late 2025 to around 20 billion DOGE at press time – Marking a roughly 30% drop. This reduction could allude to supply moving off exchanges, which can support price over time.

However, intermittent inflow spikes have still introduced some overhead pressure. This is likely to keep DOGE range-bound as opposing forces balance market direction.

Final Summary

- Dogecoin’s [DOGE] on-chain volume of 1.037 billion DOGE with the price near $0.094 reflected whale-led redistribution into exchanges.

- Exchange inflows above 4 billion DOGE, alongside a 30% drop in balances, revealed ongoing absorption, despite intermittent sell pressure keeping price compressed.