Original | Odaily Planet Daily (@OdailyChina)

Author | DingDong (@XiaMiPP)

Altcoins are dead—this is a consensus that crypto users have been reluctant to admit but have had to face over the past year. Even former blue-chip tokens have fallen into prolonged sideways movement or gradual decline amid the continuous market weakness, showing little sign of recovery.

However, amidst this overall slump, the MORPHO token has rebounded from a low of $0.96 in early February to the range of $1.8-$1.9, doubling against the trend. From the daily chart perspective, this rebound has largely formed a rounded bottom pattern, potentially signaling a bottom reversal. Is this surge merely driven by short-term market sentiment, or is it the start of a trend fueled by the resonance of fundamental and structural variables?

When the Old Dynasty Begins to Consume Itself

Morpho is a lending protocol launched in 2021. Initially, its mechanism was similar to lending protocols like Aave and Compound. However, in 2023, Morpho began rolling out Morpho Blue (the current main version), completely transforming into an independent, permissionless lending base layer, steadily ranking among the top lending ecosystems on Ethereum.

Nevertheless, in the lending sector, Aave remains the largest in scale and the strongest in brand—an undeniable fact. But recently, Aave has once again plunged into serious governance controversy due to a $51 million "Aave Will Win" funding framework proposed by its founder, Stani.

This fund was originally planned to support new product development, and the proposal explicitly stated that future related brand revenue would be 100% returned to the DAO treasury—a move that seemed like an ideal operation of "surrendering control and benefiting the community" but unexpectedly ignited long-simmering internal conflicts within the DAO.

The reason is that DAO governance representative and ACI founder Marc Zeller publicly released an "audit" report on February 25, accusing Labs of low fund utilization, having taken approximately $86 million from the DAO over the past few years without transparent disclosure. Meanwhile, core DAO developer BGD Labs announced it would exit in April 2026 due to governance friction. The founder's high voting power once again dominated the controversial proposal, further pushing the entire DAO into an open tug-of-war over power and fund distribution. As early as December last year, cracks had already appeared within the Aave community. For details, refer to Will AAVE Still Be Worth Buying After the Second-Biggest Holder Dumped Their Bag Amid Deep Divisions?

Now, while Aave is slowing down due to governance friction, the "simplicity" of Morpho's governance model is beginning to attract attention. Aave can be considered the first-generation lending governance paradigm of "DAO-led, global parameter adjustment," where all risk parameters (such as collateral factors, liquidation thresholds) are determined by global DAO voting. While this design ensures overall robustness, it easily falls into a governance bottleneck—any minor parameter adjustment requires broad community consensus, and any disagreement can lead to delays, especially during contentious periods, potentially paralyzing decision-making.

In contrast, Morpho follows a second-generation path of modularity and market-driven mechanisms: the protocol itself is highly permissionless, allowing anyone to create isolated markets at any time. The risk parameters for each market (such as LTV, interest rate curves, liquidation incentives) are set by independent professional risk managers (curators), rather than relying on全网 DAO voting. This means risks are strictly localized within individual markets, with responsibility分散到 specific curators, significantly speeding up decision-making. Curators can quickly iterate parameters based on actual market conditions without waiting for global consensus. The advantage of this design is that it greatly reduces governance friction and decision-making delays.

When the old dynasty begins to consume itself internally, it might be the opportunity for new forces to overtake on the curve.

Data Verification: Does It Deserve This Window of Opportunity?

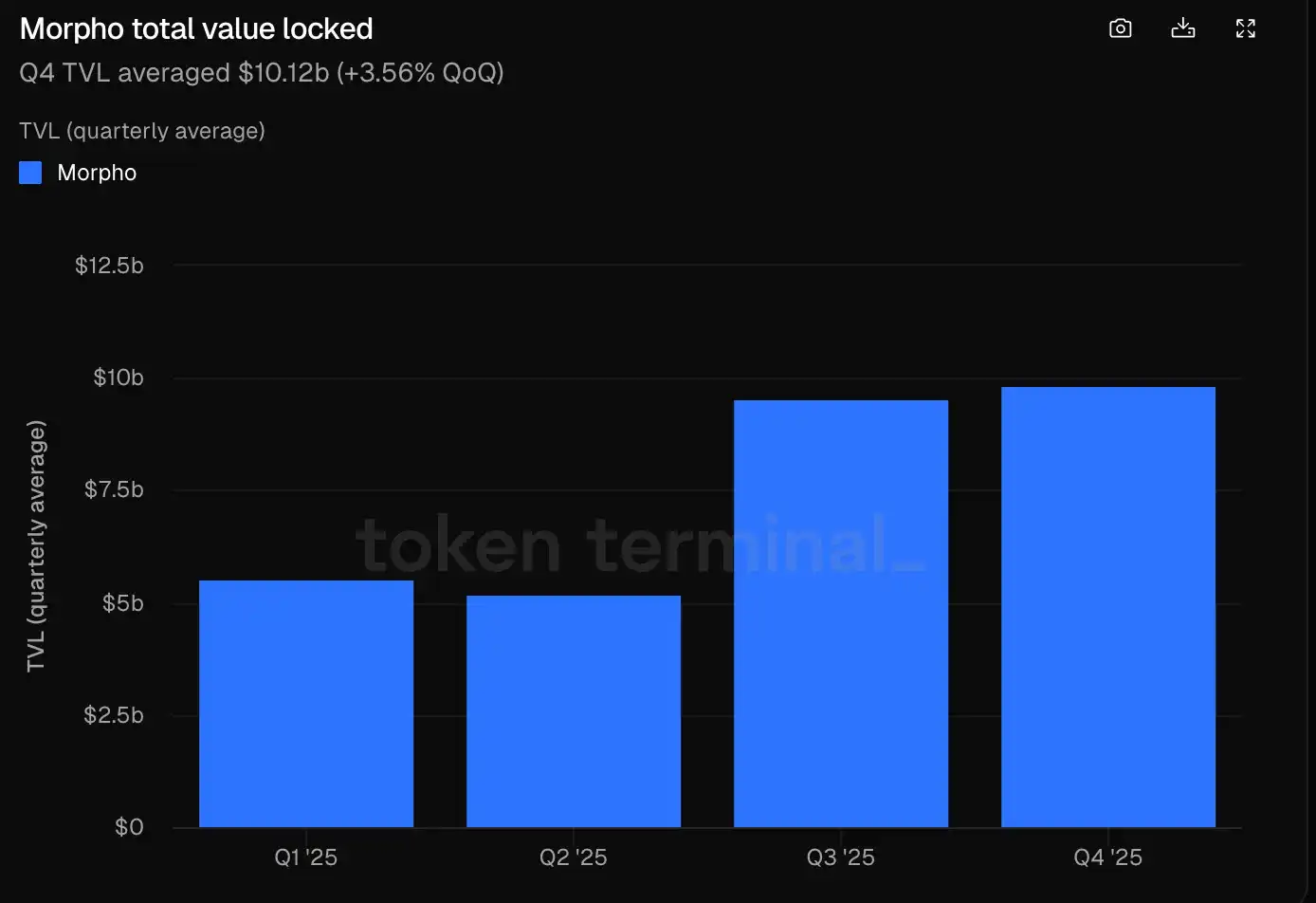

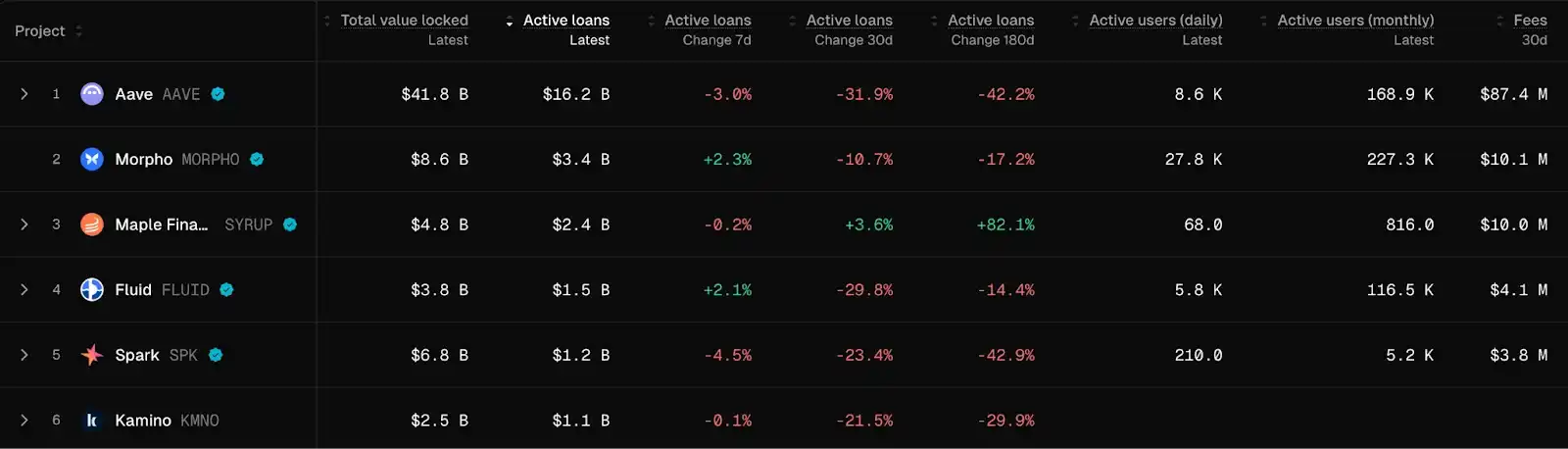

Let's look at Morpho's fundamentals to see if it has the potential to challenge Aave's lending throne. According to Tokenterminal data, in Q3 and Q4 of 2025, Morpho protocol's TVL remained above $9.5 billion, an increase of about 80% compared to the first half of the year;

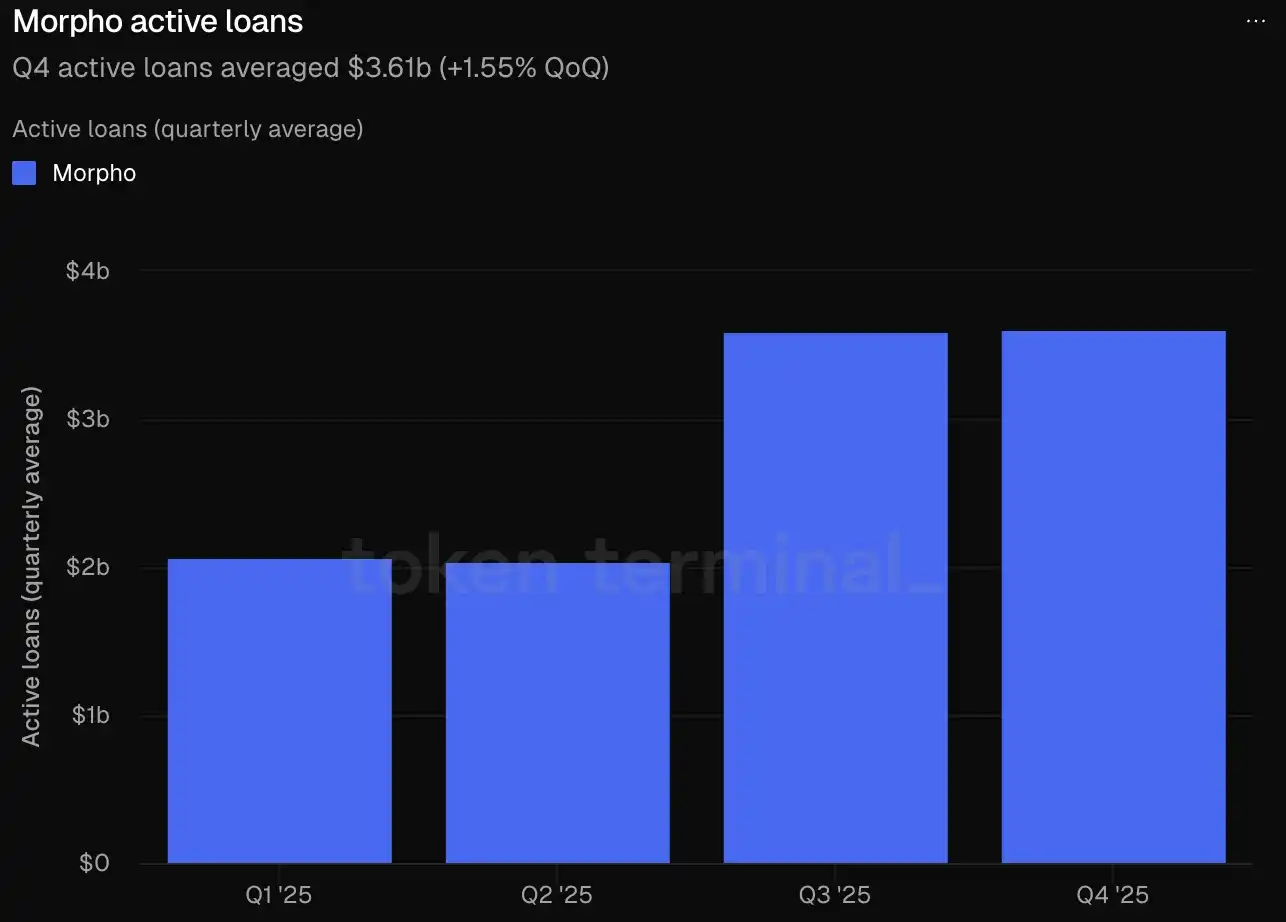

The active loan size within the protocol also stayed above $3.5 billion in both Q3 and Q4, a year-on-year increase of about 80%.

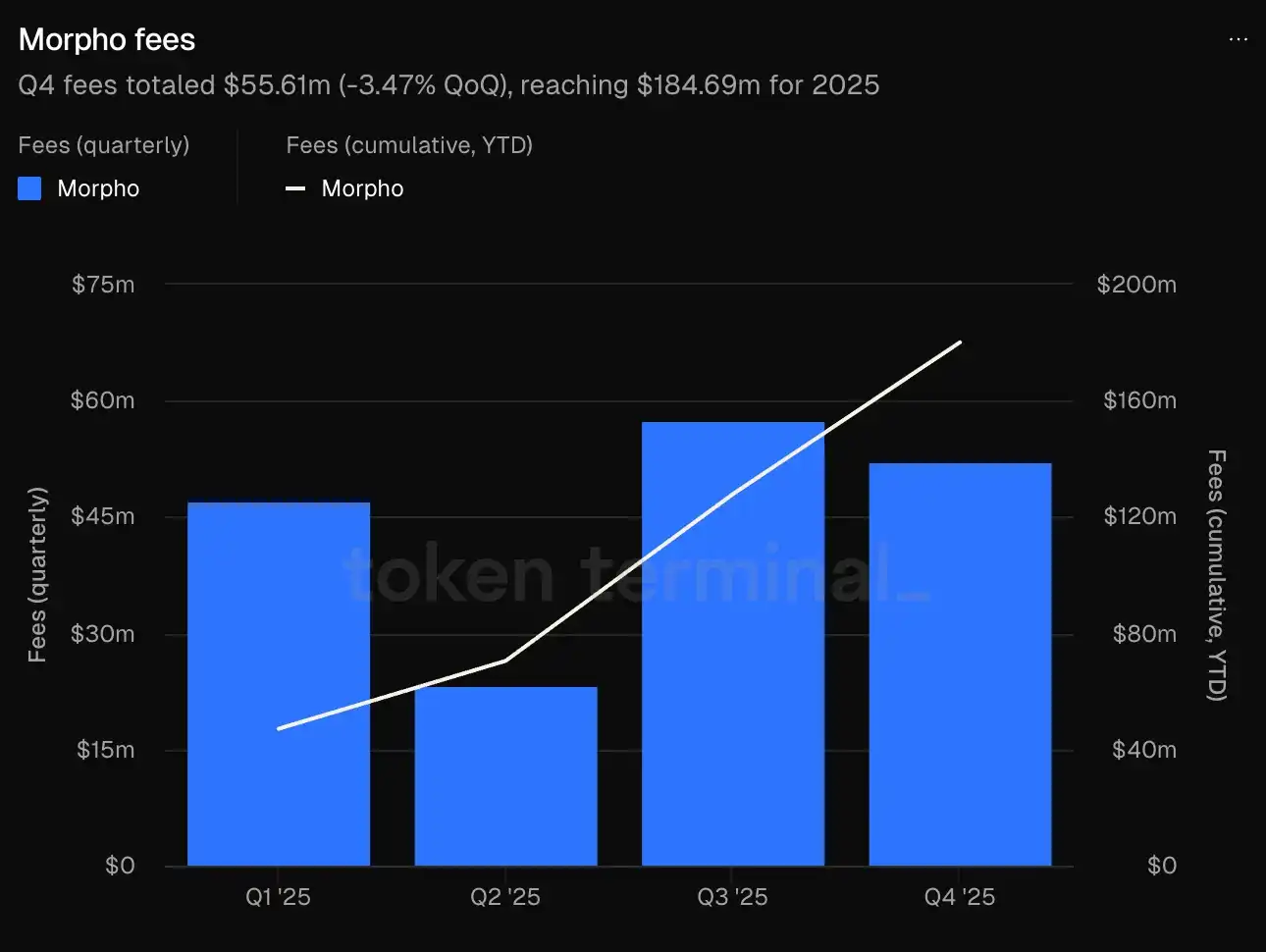

Regarding one of the core metrics for DeFi protocols—protocol revenue—aside from a relatively weak performance in Q2, it remained stable at around $50 million in other quarters.

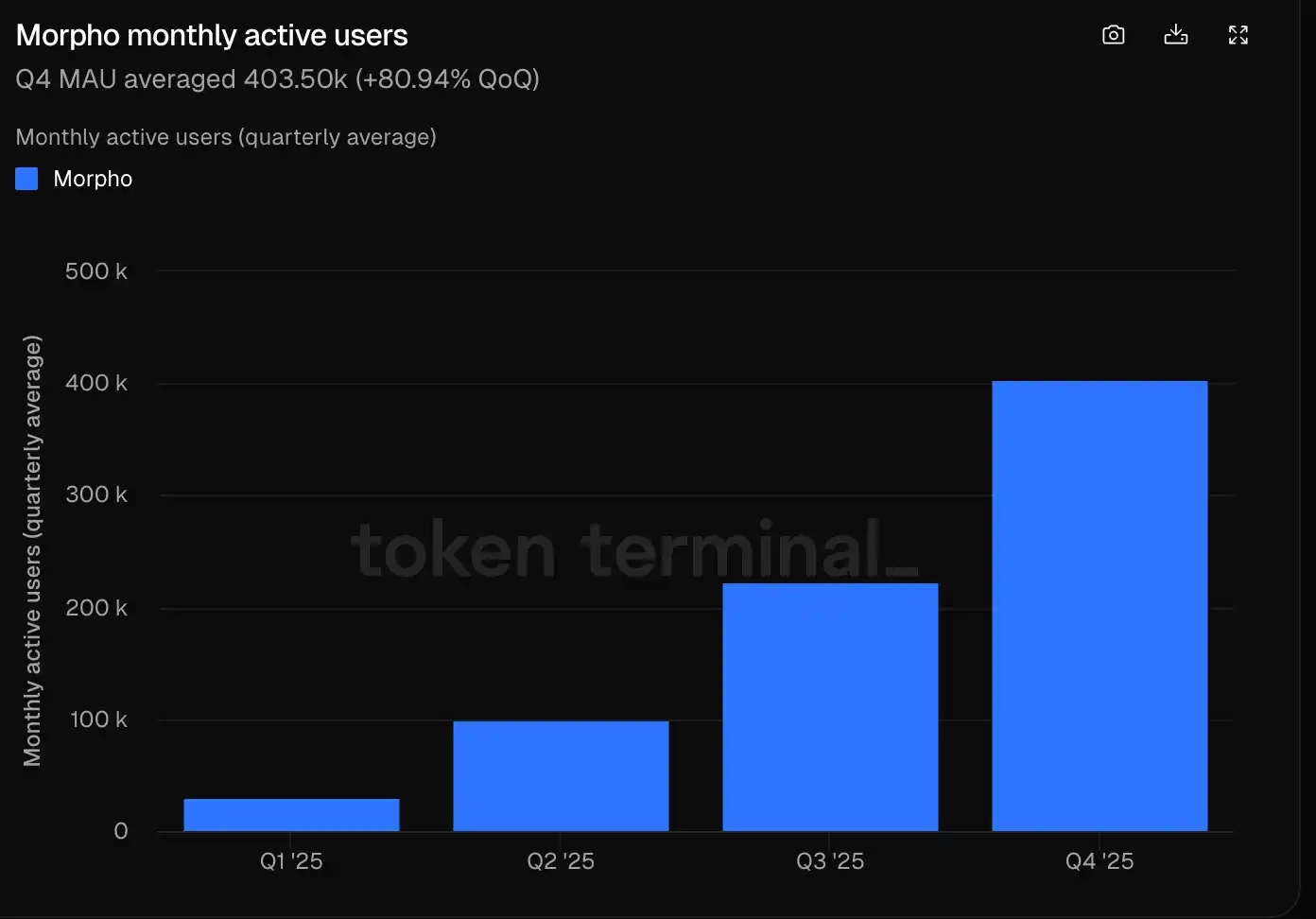

User growth is even more直观, with its quarterly active addresses rapidly expanding from about 30,000 in Q1 to the 400,000 level, showing strong organic growth momentum.

Although Morpho's current TVL and active loan size still lag behind Aave's, its user growth rate has made it one of the most aggressive "dark horses" in the lending赛道. Especially against the backdrop of the entire DeFi sector generally facing pressure and experiencing阵痛 in 2025, Morpho's performance can be considered achieving counter-trend high growth,足以证明 its product model has withstood the market test. Protocols that can continuously attract capital and users during a bear market often possess stronger爆发力 in the next cycle.

Institutional Variable: When Traditional Capital Starts Betting

Good fundamental data performance only proves that the protocol has a solid foundation, but the bigger catalyst that truly changes the market cap curve is the entry of traditional financial giants.

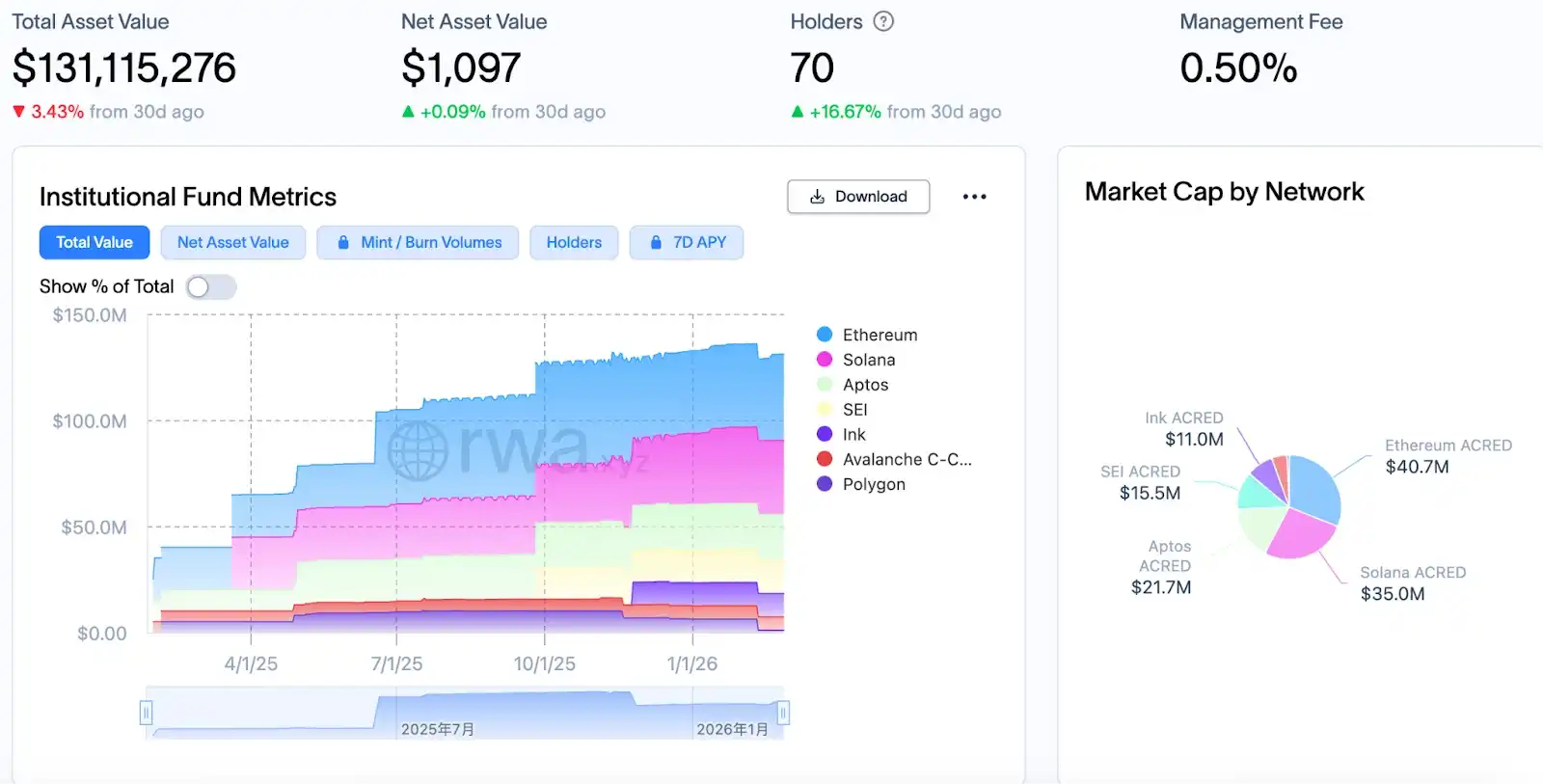

On February 13, Wall Street asset management giant Apollo Global Management signed a重磅 cooperation agreement with the Morpho Association, the non-profit organization behind Morpho. Specifically, Apollo plans to gradually acquire up to 90 million MORPHO tokens over the next 48 months, equivalent to approximately 9% of Morpho's total supply. At the current price of $1.8, this is worth about $162 million.

From a purely trading perspective, this will bring sustained buying demand for MORPHO. But if you know Apollo, you'll understand that this is more like its strategic penetration into DeFi.

Apollo manages assets接近 $940 billion, and its private credit business is known for pursuing high yields. The on-chain world can provide opportunities for leverage amplification and global instant liquidity. It began dipping its toes into the crypto industry in 2024, with RWA as its main battlefield, partnering with Securitize to tokenize its diversified credit strategy into ACRED, which has now reached a scale of $130 million.

However, the core challenge after bringing RWA on-chain has never been issuance, but liquidity release. Assets can be tokenized, but without efficient lending markets and leverage environments, their yield potential is difficult to unleash. Looking at Apollo's布局, it's not unreasonable to speculate that it likely intends to use Morpho's lending markets to amplify the yield of its credit products. Because Morpho's modular lending structure provides a天然适配场景 for RWA—isolated markets, independent risk parameters, customizable leverage environments. These mechanisms are far more attractive to institutions than parameter games under unified governance.

This conjecture is not without basis, because although Morpho is highly permissionless, key parameter options still need to be expanded through Morpho DAO governance. If Apollo holds a significant amount of MORPHO tokens, it will gain corresponding voting power and could promote the addition of RWA-friendly parameters. If Apollo's intentions materialize as推测, Morpho's modular design could attract accelerated inflows of more institutional capital, making it key infrastructure for the on-chain amplification of institutional credit products. This institutional-level endorsement would not only strengthen Morpho's competitive advantage but also narrow the gap with Aave—especially while Aave is deeply mired in internal governance issues.

Conclusion

Aave's governance crisis may continue to drag down its market cap and liquidity in the short term, while Morpho, leveraging its product structural advantages and institutional catalysts, is quietly rewriting the competitive landscape of the lending赛道. However, whether Morpho can truly shake Aave's throne still depends on observing its continued TVL追赶 and the follow-up of more TradFi players. But至少 for now, the power transition for the "second-generation lending leader" has already begun.

Risk提示: MORPHO tokens will undergo a large unlock in March, belonging to the Morpho DAO, Morpho Association treasury, and core contributors. Short-term liquidity impact requires attention.