Written by: milian

Compiled by: AididiaoJP, Foresight News

In the world of cryptocurrency, the promise of "KYC-free crypto cards" occupies a peculiar position.

It is promoted as a technological achievement, packaged as a consumer product, and longed for as an "escape hatch" from financial surveillance. Spend cryptocurrency wherever Visa or Mastercard is accepted, no identity verification, no personal information, no questions asked.

You might naturally ask: Why hasn't this been done yet? The answer is: It actually has—more than once—but it has also failed again and again.

To understand why, one must not begin with cryptocurrency itself, but with the infrastructure of crypto cards. Debit and credit cards are not neutral tools; they are "permits to pass" granted by a heavily regulated payment system dominated by the two giants, Visa and Mastercard. Any card that works globally must be issued by a licensed bank, routed through an identifiable six-digit BIN code, and subject to a series of explicit compliance contractual obligations—including a strict prohibition on anonymous end-users.

There is no technical "workaround" for building a card on top of the Visa/Mastercard system. The only way is "misrepresentation".

What is typically sold as a "KYC-free cryptocurrency card" is essentially a corporate card. Except for prepaid cards with very low limits not designed for large-scale use, these cards are legally issued to businesses (often shell companies), with the intended purpose of internal reimbursement for business expenses by company employees. In some cases, these businesses are legitimate; in others, their existence is solely to obtain card issuance qualifications.

Consumers were never the intended cardholders for these cards.

This structure might work in the short term. Cards are distributed externally, labeled as consumer products, and tolerated until they attract enough attention, but attention always invites scrutiny. A Visa compliance representative can trace the BIN code to the issuing bank, identify the abuse, and then terminate the entire program. When this happens, accounts are frozen, the issuer is cut off, and the product disappears—a process usually completed within six to twelve months.

This model is not hypothetical. It is a repeatable, observable, and well-known reality within the payments industry.

The illusion persists only because the "shutdown" always comes after the "launch".

Why Users Are Attracted to "KYC-Free Cards"

The appeal of KYC-free cards is very specific.

It reflects the restrictions faced in accessing funds, intertwining privacy concerns with usability issues. Some users value privacy on principle, while others live in regions where formal banking services are restricted, unreliable, or outright denied. For users in sanctioned countries, KYC is not just a privacy invasion but a direct exclusion, severely limiting which financial channels they can use and when.

In these situations, non-KYC payment tools are not an ideological choice but a temporary "lifeline".

This distinction is crucial. Risk doesn't disappear because it's "necessary"; it just gets concentrated. Users who rely on these tools are often fully aware they are making a trade-off: sacrificing long-term security for short-term usability.

In practice, payment channels stripped of identity verification and transaction reversibility inevitably accumulate transaction flows that cannot pass standard compliance checks. This is an operational reality observed by issuers, project operators, and card networks, not theoretical speculation. When access is unimpeded and traceability is weak, funds blocked elsewhere naturally flow here.

Once transaction volume grows, this imbalance is quickly exposed. The resulting concentration of high-risk funds is the main reason these projects, regardless of marketing or target audience, eventually attract scrutiny and intervention.

The marketing around KYC-free crypto cards is always severely exaggerated, far beyond the legal constraints faced by payment network operations. The chasm between "promise" and "constraint" is rarely noticed when users sign up, but it sets the stage for the eventual outcome as these products scale.

The Harsh Reality of Payment Infrastructure

Visa and Mastercard are not neutral intermediaries. They are regulated payment networks operating through licensed issuing banks, acquiring banks, and a contractual compliance framework that requires end-users to be traceable.

Every globally usable card is tied to an issuing bank, and every issuing bank is bound by network rules. These rules require: the ultimate user of the card must be identifiable. There is no opt-out, no hidden configuration, no technical abstraction that can bypass this requirement.

If a card works globally, by definition, it is embedded within this system. The constraints are not at the application layer but in the contracts governing settlement, issuance, liability, and dispute resolution.

Therefore, achieving unrestricted, KYC-free spending on Visa or Mastercard rails is not just difficult—it's impossible. Anything that appears to defy this reality is either operating within strict prepaid limits, misclassifying the end-user, or merely "delaying" rather than "avoiding" enforcement.

Detection is easy. A test transaction is enough to expose the BIN code, issuing bank, card type, and program manager. Shutting down a program is an administrative decision, not a technical challenge.

The fundamental rule is simple:

If you didn't do KYC for your card, then someone else did.

And that person who did the KYC truly owns the account.

The "Corporate Card Loophole" Explained

Most so-called KYC-free cryptocurrency cards rely on the same mechanism: the corporate expense card.

This structure is not mysterious. It is a well-known "loophole" within the industry, or rather, an "open secret" born from how corporate cards are issued and managed. A company registers through a business identity verification (KYB) process, which is often relatively lax compared to individual consumer verification. In the eyes of the issuer, this company is the client. Once approved, the company can issue cards to employees or authorized spenders without additional identity verification at the cardholder level.

In theory, this is to support legitimate business operations. In practice, it is often abused.

The end-user is on paper treated as an "employee," not a bank customer. This is precisely why they are not individually KYC'd. This is the secret sauce that allows these products to call themselves "KYC-free".

Unlike prepaid cards, corporate expense cards can hold and transfer large sums. They are not designed for anonymous distribution to consumers or for hosting third-party funds.

Cryptocurrency usually cannot be deposited directly, hence the need for various backend "workarounds": wallet intermediaries, conversion layers, internal bookkeeping...

This structure is inherently fragile. It can only last until it attracts sufficient attention, and once noticed, enforcement is inevitable. History shows that projects built this way rarely survive more than six to twelve months.

The typical process is as follows:

- Create a company, complete KYB verification with the card issuer.

- In the issuer's eyes, this company is the client.

- The company issues cards to "employees" or "authorized users".

- End-users are treated as employees, not bank clients.

- Therefore, the end-users themselves do not need KYC.

Is this a loophole, or is it illegal?

Issuing corporate cards to real employees for legitimate business expenses is legal. But publicly issuing them as consumer products to the masses is not.

Once cards are distributed to "fake employees," marketed publicly, or used primarily for personal spending, the issuer is at risk. Visa and Mastercard don't need new regulations to act; they just need to enforce existing rules.

One compliance review is enough.

Visa's compliance personnel can register themselves, receive a card, identify the issuing bank through the six-digit BIN code, trace the entire program, and shut it down.

When it happens, accounts are frozen first. Explanations may come later, sometimes not at all.

Predictable Lifecycle

The failure of projects marketed as "KYC-free" crypto cards is not random; it follows a remarkably consistent trajectory, repeated across dozens of projects.

First is the "Honeypot Phase". The project launches quietly, early access is restricted, spending works as advertised, the first users report success. Confidence builds, marketing accelerates. Limits increase, influencers hype the offering. Success screenshots circulate, and a once-niche project becomes noticeable.

Visibility is the tipping point.

Once transaction volume grows and the project draws notice, scrutiny is inevitable. The issuing bank, program manager, or card network reviews its activity. The BIN is identified. The vast gap between the card's marketing and its contractually permitted mode of operation becomes apparent. At this point, enforcement is no longer a technical issue but an administrative one.

Within six to twelve months, the outcome is almost always the same: the issuer is warned or terminated; the project is suspended; cards stop working without warning; balances are frozen; operators vanish behind support tickets and generic email addresses. Users have nowhere to appeal, no legal standing, and no clear timeline for fund recovery—if recovery is even possible.

This is not speculation or theory. It is an observable pattern repeated across jurisdictions, issuers, and market cycles.

KYC-free cards operating on Visa or Mastercard rails will always be shut down; the only variable is timing.

Inevitable Doom Cycle (Summary)

- Honeypot Phase: A "KYC-free" card quietly. Early users succeed, influencers promote, volume increases.

- Regulatory Squeeze: Issuing bank or card network reviews the project, flags the BIN, identifies abuse of the issuance structure.

- Fork in the Road:

- Forced to introduce KYC → Privacy promise completely collapses.

- Operators abscond or vanish → Cards deactivated, balances frozen, support channels go dark.

There is no fourth outcome.

How to Identify a "KYC-Free" Crypto Card in 30 Seconds

Take the marketing image of Offgrid.cash's so-called non-KYC crypto card as an example. Zoom in on the card, and one detail immediately stands out: the "Visa Business Platinum" label.

This is not a design flourish or branding choice; it is a legal classification. Visa does not issue Business Platinum cards to anonymous consumers. This label means it participates in a corporate card program, where account and fund ownership belong to the company, not the individual user.

The deeper implications of this structure are rarely made explicit. When users deposit cryptocurrency into such a system, a subtle but crucial legal shift occurs: the funds are no longer the user's property but become assets controlled by the enterprise holding the corporate account. The user has no direct relationship with the issuing bank, no deposit insurance, and no right to complain to Visa or Mastercard.

Legally, the user is not a customer at all. If the operator disappears or the project is terminated, the funds are not "stolen"; you voluntarily transferred them to a third party that no longer exists or can no longer access the card network.

When you deposit cryptocurrency, a critical legal shift occurs:

- The funds no longer belong to you.

- They belong to the company that completed KYB with the issuing bank.

- You have no direct relationship with the bank.

- You have no deposit protection.

- You have no right to complain to Visa or Mastercard.

- You are not the customer. You are just a "cost center".

- If Offgrid disappears tomorrow, your funds are not "stolen"—you legally transferred them to a third party.

This is the core risk most users never perceive.

Three Immediate Red Flags

You don't need insider information to tell if you're funding a corporate card. Just look for three things:

- Card Type Printed on the Card: If it says Visa Business, Business Platinum, Corporate, Commercial, then it's not a consumer card. You are being registered as an "employee".

- Network Logo: If it's supported by Visa or Mastercard, it must comply with AML, sanctions screening, and end-user traceability rules.

- No exceptions.

- No technical workarounds.

- Only a matter of time.

- Unreasonable Spending Limits: If a card offers simultaneously: high monthly limits, reloadability, global usability, no KYC, then someone else did the KYB for you.

Current Card Projects Marketing This Model

Projects currently marketing "KYC-free" cards fall into two categories: prepaid cards and so-called "business" cards. Business cards rely on variations of the corporate card loophole described earlier. The names change, but the structure does not.

A non-exhaustive list of projects currently marketing "KYC-free" cards (covering both prepaid and business card models) can be found at https://www.todey.xyz/cards/.

Examples include:

- Offgrid.cash

- Bitsika

- Goblin Cards

- Bing Card

- Similar "crypto cards" distributed via Telegram or invite-only

Case Study: SolCard

SolCard is a classic example. After launching with a KYC-free model and gaining traction, it was forced to switch to full KYC. Accounts were frozen until users provided identification, shattering the initial privacy vision overnight.

The project eventually pivoted to a hybrid structure: a very low-limit KYC-free prepaid card and a fully KYC-verified card. The original KYC-free card model could not survive after attracting substantial use, an inevitable result of operating on incompatible rails.

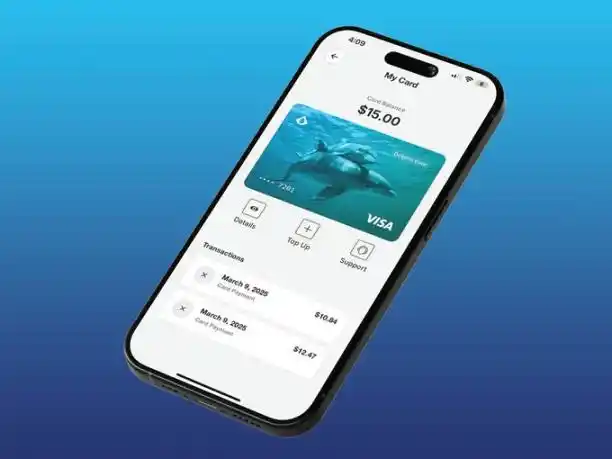

Case Study: Aqua Wallet's Dolphin Card

In mid-2025, Aqua Wallet, a Bitcoin and Lightning Network wallet developed by JAN3, launched the Dolphin Card. It was launched as a limited beta for 50 users, requiring no identity documents. Users could deposit Bitcoin or USDT, with a spending cap of $4000.

This cap itself is telling—it was explicitly designed to lower regulatory risk.

Structurally, the Dolphin Card combined a prepaid model with a corporate account setup. The card operated through company-controlled accounts, not individual bank accounts.

For a while, it worked, but not forever.

In December 2025, the project was suddenly paused due to "unexpected issues" with the card supplier. All Dolphin Visa cards immediately became invalid, and remaining balances required manual refunds via USDT, with no further explanation.

Risks Faced by Users

When these projects collapse, it's the users who pay the price.

Funds can be frozen indefinitely, refunds may require cumbersome manual processes. Sometimes, balances are lost entirely. There is no deposit insurance, no consumer protection, and no legitimate claim against the issuing bank.

Particularly dangerous is that many operators know this outcome in advance. Yet they proceed anyway. Others obscure the risk with talk of "proprietary technology," "regulatory innovation," or "new infrastructure."

There is no "proprietary technology" in issuing corporate cards to fake employees.

At best, it's ignorance; at worst, it's赤裸裸的榨取.

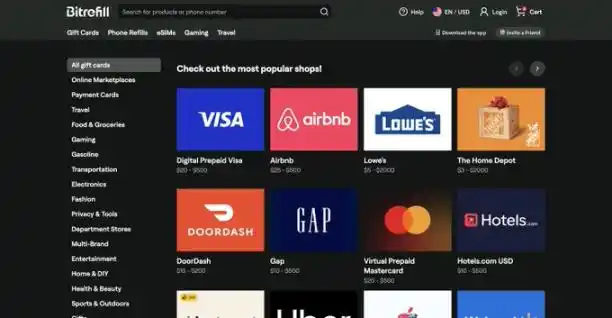

Prepaid Cards and Gift Cards: What Actually Works?

Legitimate non-KYC payment tools exist, but they have strict limits.

Prepaid cards purchased through compliant providers are legitimate because they have very low limits, are designed for small amounts, and don't pretend to offer unlimited spending. Examples include prepaid crypto cards offered through platforms like Laso Finance.

(@LasoFinance website screenshot)

Gift cards are another option. Services like Bitrefill allow users to privately purchase gift cards for mainstream merchants using cryptocurrency, which is entirely legal and compliant.

(@bitrefill website screenshot)

These tools work because they respect regulatory boundaries, not because they pretend they don't exist.

The Core Misrepresentation Problem

The most dangerous claim is not about "KYC-free" itself, but about permanence.

These projects imply they have "solved" the problem, found a "structural loophole," that their technology makes compliance "irrelevant".

This is not true.

Visa and Mastercard do not negotiate with startups; they enforce rules.

Any product promising high limits, reloadability, global usability, no KYC, while displaying the Visa or Mastercard logo, is either misrepresenting its structure or planning to disappear in the near future.

There is no "proprietary" technology that bypasses this fundamental requirement.

Some operators argue that KYC will eventually be introduced via "zero-knowledge proofs," so the company itself never directly collects or stores user identity. But this doesn't solve the core issue. Visa and Mastercard don't care "who" sees the identity; they require that identity information is recorded and can be read and retrieved by the issuing bank or compliance partner in case of audit, dispute, or law enforcement action.

Even if verification is done via privacy-preserving credentials, the issuer must still be able to access a clear, readable record at some point in the compliance chain. This is not "KYC-free".

What Happens If You Bypass the Duopoly?

(@colossuspay website screenshot)

There is a category of card-like payment systems that fundamentally changes the game: those that do not rely on Visa or Mastercard at all.

Colossus Pay is an example of this thinking.

It does not issue cards through licensed banks nor route transactions through traditional card networks. Instead, it acts as a crypto-native payment network, integrating directly with merchant acquirers. Acquirers are entities that own merchant relationships and control point-of-sale payment terminal software; there are only a few globally, such as Fiserv, Elavon, Worldpay, etc.

By integrating at the acquirer layer, Colossus completely bypasses the issuer and card network stack. Stablecoins are routed directly to the acquirer, converted as needed, and settled to the merchant. This lowers fees, shortens settlement times, and removes the "toll" Visa and Mastercard charge per transaction.

Crucially, because there is no issuing bank or card network involved in the transaction flow, there is no entity contractually required to perform end-user KYC for card issuance. Under the current regulatory framework, the only entity负有 KYC obligations in this model is the stablecoin issuer itself. The payment network doesn't need to invent loopholes or misclassify users because it doesn't operate under card network rules to begin with.

In this model, the "card" is essentially just a private key authorizing payment. KYC-free is not the goal; it is a natural byproduct of removing the duopoly and its attendant compliance structures.

This is the path to a structurally honest, non-KYC payment tool.

If this model works, the obvious question is: Why isn't it widespread yet?

The answer is distribution.

Integrating with acquirers is very difficult. They are conservative institutions, controlling terminal operating systems, and move slowly. Integration at this layer takes time, trust, and operational maturity. But this is also where real change can happen, because it is this layer that controls how the physical world accepts payments.

Most crypto card startups take the easier path: integrate with Visa or Mastercard, market aggressively, scale fast before enforcement arrives. Building outside the duopoly is slower and harder, but it's also the only path that doesn't end in "shutdown".

Conceptually, this model collapses the credit card into a crypto primitive. The card is no longer an account issued by a bank, but a private key authorizing payment.

Conclusion

As long as Visa and Mastercard remain the underlying infrastructure, unlimited spending without KYC is impossible. These limits are structural, not technical, and no amount of packaging, storytelling, or fancy terminology can change this reality.

When a card bearing the Visa or Mastercard logo promises high limits and no KYC, the explanation is simple: it is either leveraging a corporate card structure, placing users outside the legal relationship with the bank, or it is misrepresenting how the product actually works. History has proven this repeatedly.

The truly safer options are limited prepaid cards and gift cards with clear caps and expectations. The only lasting, long-term solution is to abandon the Visa-Mastercard duopoly entirely. Everything else is temporary, fragile, and exposes users to risks they often only realize too late.

Over the past few months, I've seen discussion around "KYC-free cards" heat up dramatically. I wrote this article because there is a massive knowledge gap about how these products actually work and the legal and custodial risks they pose to users. I have nothing to sell; I write about privacy because it matters, wherever it touches.

Câu hỏi Liên quan

QWhy do 'no-KYC crypto cards' that bypass traditional payment networks ultimately fail?![]()

AThey fail because Visa and Mastercard are regulated payment networks that require all globally usable cards to be issued by licensed banks, which must comply with strict contractual obligations, including identifying end-users. Any 'no-KYC' card operating on these networks relies on misrepresenting its structure (e.g., using corporate card programs for non-employee consumers), which is unsustainable and leads to eventual shutdown by compliance enforcement.

QWhat is the 'corporate card loophole' commonly exploited by no-KYC crypto card providers?![]()

AThe 'corporate card loophole' involves a company undergoing business verification (KYB) to obtain a corporate card program from an issuer. The company then distributes cards to users labeled as 'employees' or 'authorized spenders,' avoiding individual KYC checks. This structure is intended for legitimate business expenses but is abused for consumer crypto spending, violating network rules and leading to eventual termination.

QWhat are the risks for users of no-KYC crypto cards?![]()

AUsers face significant risks, including sudden account freezes, loss of funds, lack of deposit insurance, and no legal recourse against issuers. When projects are shut down, balances may be indefinitely frozen or require manual refunds. Users are not direct clients of the bank, and their funds are legally controlled by the company that obtained the card program, leaving them vulnerable if the operator disappears.

QHow can one identify a no-KYC crypto card that relies on the corporate card model?![]()

ALook for key indicators: the card prominently displays labels like 'Visa Business,' 'Business Platinum,' or 'Corporate,' indicating it is not a consumer card. Additionally, high spending limits combined with no-KYC requirements and global usability are red flags, as they imply the use of a corporate structure where someone else (the company) has undergone KYB instead of the user.

QWhat is a structurally honest alternative to no-KYC cards on Visa/Mastercard networks?![]()

AA viable alternative is to bypass Visa/Mastercard duopoly entirely by building crypto-native payment networks that integrate directly with merchant acquirers (e.g., Fiserv, Worldpay). This model, as seen with projects like Colossus Pay, uses stablecoins routed through acquirers without involving issuing banks or card networks, eliminating the need for KYC under existing card rules and offering a sustainable path for permissionless payments.