Author: Prathik Desai

Compiled by: Block unicorn

Preface

Clocks are not a good way to cover up delays. For decades, financial markets have been built around the speed of information transmission. They introduced closing bells, batch settlements, and regional exchanges, which made sense in an era of slow information flow. But all that has changed. Capital does not wait. Just as water always finds a crack, so does capital. Financial gravity pulls it towards the fastest path to obtain price information. This is the law of the market. Market participants will not tolerate inefficiency forever.

This is what I have observed from a macro perspective over the past few weeks as financial markets have evolved.

In today's article, I will help you understand what has broken the old bundled structure of financial markets, transforming it into a more efficient, unbundled structure that spans different venues, wrappers, and times.

Changing of the Guard

I have been studying finance for over a decade. In the early stages of my learning, I always viewed traditional stock exchanges as synonymous with the market. For most of their development, stock exchanges were the place where everyone and everything converged: buyers, sellers, regulators, and the technology that drives the market. It had indices tracking its components, and it had clocks indicating trading hours, telling everyone when they could trade and when they could not.

But this has changed in the past few years. In fact, just in the past few weeks, we have seen several developments that confirm this shift.

On March 18, S&P Dow Jones Indices licensed the S&P 500 index to Trade[XYZ], allowing HIP-3 market deployers to launch the first and only S&P 500 perpetual derivatives contract on the Hyperliquid exchange. The S&P 500 is the world's most followed large-cap U.S. equity index, tracking 500 leading U.S. companies, covering about 80% of the total U.S. market capitalization, with a total market cap of over $61 trillion. The index covers at least half of the global equity market's capitalization.

This is an index with nearly 70 years of history, listed on a market that is only 6 months old.

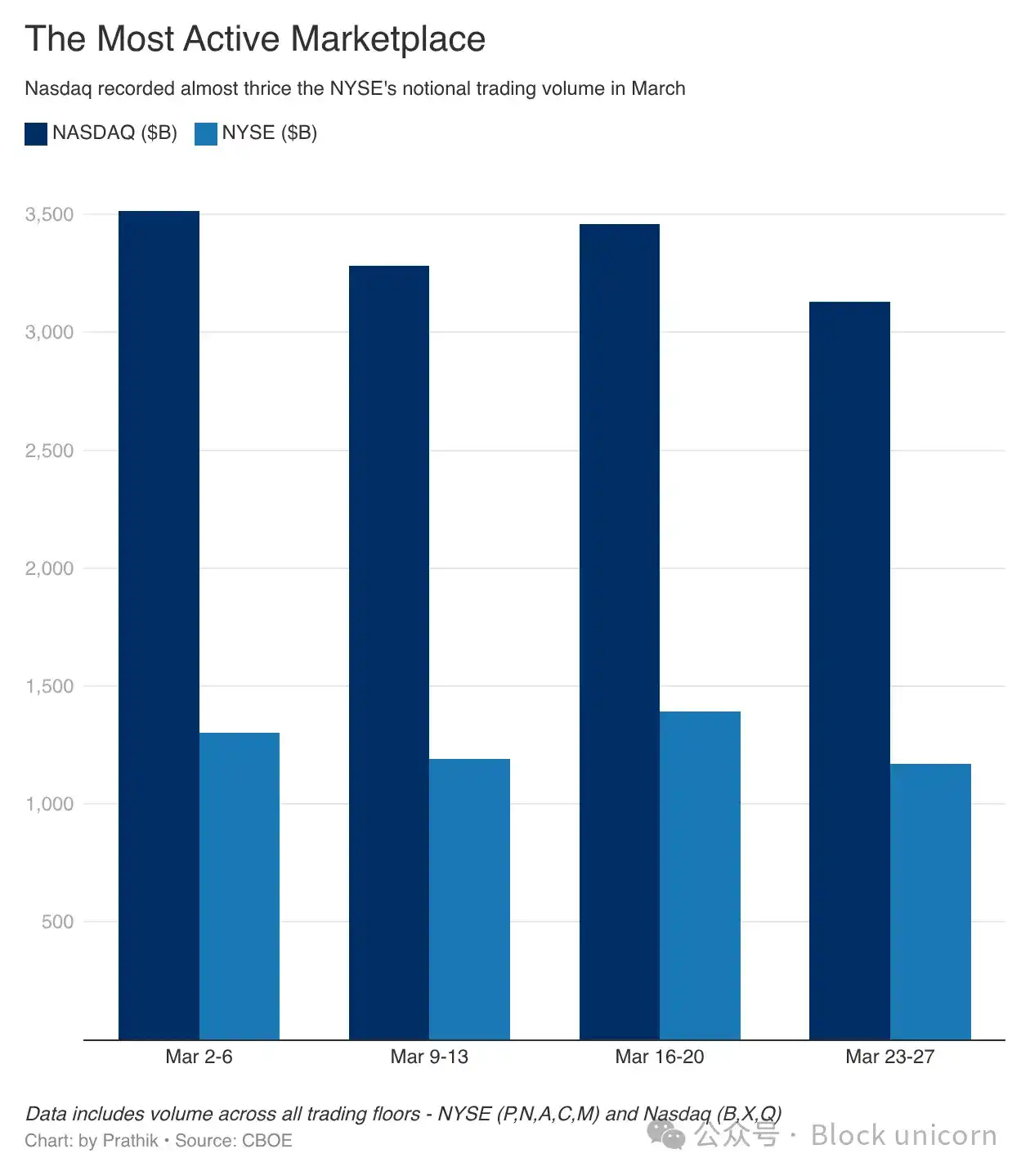

The day after S&P's announcement, the U.S. Securities and Exchange Commission (SEC) approved Nasdaq's application to trade and settle some stocks in tokenized form. Nasdaq is one of the world's most active trading venues, often exceeding the nominal trading volume of the New York Stock Exchange (NYSE), the world's largest exchange by market capitalization.

On March 16, Cboe Global Markets (Cboe Global Markets) filed a proposal with the U.S. Securities and Exchange Commission (SEC) to launch "near 24x5 U.S. equity trading." The largest operating body behind this U.S. financial exchange stated that it is ready to provide 24/5 equity trading services as early as December 2026.

But why? There is growing demand for extended U.S. equity trading hours.

These three initiatives collectively target the outdated bundled trading structure. Hyperliquid's launch of an S&P 500 futures trading market challenges the decades-old convention where investors could only trade traditional indices through traditional markets. It also enables 24/7 global trading of one of the most tracked large-cap indices.

Nasdaq's tokenized stock trading initiative targets infrastructure. It introduces a new form of wrapping, allowing the same stock to be traded in different ways. Previous attempts at tokenizing stocks have been criticized by the industry.

Investors questioned whether these tokens享有 the same rights as the original shares.

But, if I provide the same equity exposure through a token on the blockchain, without losing the voting rights and legal protections attached to the original dematerialized shares, wouldn't you accept it?

Why would you do this? What's in it for you?

Well, if you are an investor outside the U.S. who wants easier access to the stock market of the world's largest economy? What if this tokenized stock makes it easier for you to integrate it with collateral and lending systems?

When you consider 24/7 trading, these advantages multiply.

This is what Cboe is attacking. Its near 24x5 (24 hours a day, 5 days a week) trading proposal aims to acknowledge that capital does not wait for office hours. Traders always want to express their views immediately after receiving information. If Cboe does not provide them with a market to express their views, then traders will flock to other platforms that do.

Nothing I'm talking about is hypothetical, nor is it something that "might happen in the near future." They are happening, right now, as we speak.

An Unbundled Future

The adoption of financial product unbundling is most evident in Hyperliquid's HIP-3 market, which only officially launched in late October 2025.

In the past month alone, the cumulative trading volume on the HIP-3 market increased by $72 billion. The cumulative volume for the previous four months was $78 billion.

In March, Trade[XYZ] perpetual markets on traditional financial commodities and equities continued to account for 90% of HIP-3's daily trading volume. But this is not the most interesting aspect.

More than half of Trade[XYZ]'s trading volume comes from perpetual contract markets for silver, crude oil, Brent crude, and gold.

Hyperliquid provides a unified trading platform for spot cryptocurrencies as well as perpetual contracts for both cryptocurrencies and traditional assets. This not only simplifies the trading process on a unified platform but also brings higher liquidity, a unified user interface, and tighter bid-ask spreads.

Traders still want to trade some of the largest, hottest assets, spanning commodities, publicly listed companies, large private companies, and indices. You might want to trade silver, gold, crude oil, Tesla, Apple, Amazon, Google, an index tracking the top 100 U.S. non-financial companies, and the S&P 500 index—all of which can be done on the Hyperliquid platform.

HIP-3 unbundles the function of investing in these assets from the existing exchange infrastructure, while still tracking the underlying assets of their original benchmarks. So when you go long on a silver futures contract on HIP-3, the underlying asset it tracks is still pegged to the value of one ounce of silver in the Pyth data feed.

Traders have switched from previous platforms to trading silver on HIP-3 because HIP-3 does not distinguish between U.S. and non-U.S. traders, nor does it follow any specific time. Whenever an event occurs that traders want to express a view on through asset pricing, HIP-3 provides them with a market, regardless of the trader's geographic location or time zone.

The significant growth in open interest (OI) on the Hyperliquid platform over the past few weeks fully demonstrates the above results. OI measures the total value of outstanding derivative positions. Unlike volume, which reflects trading activity, OI reflects trading commitment.

Open interest was $1.13 billion on March 1 and doubled to $2.2 billion on April 1. This shows that traders are confident in Hyperliquid's perpetual contracts and are locking in funds.

These metrics indicate that when market access is easier and there is less friction, traders will not be loyal to a particular platform or asset class. They will choose any platform that offers volatility, convenience, and liquidity.

This is why traditional institutions like S&P, Nasdaq, and Cboe are taking steps to acknowledge this behavior.

At least two recent events have demonstrated the importance of 24/7 trading and market volatility to traders.

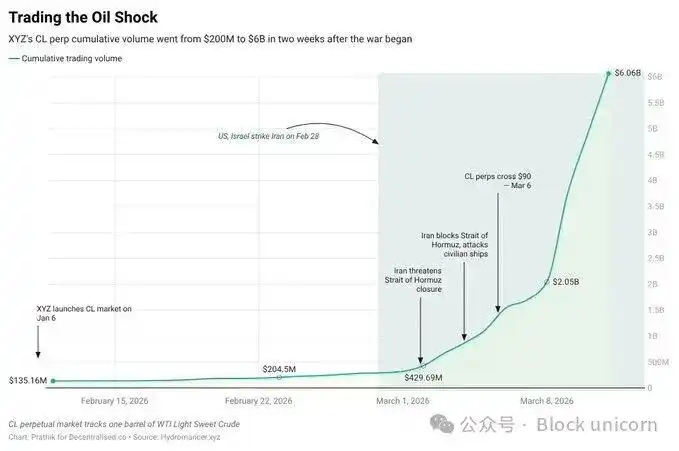

Saurabh wrote in a tweet on Decentralised.Co: "On February 28, the U.S. and Israel attacked Iran during traditional market hours. Within hours, the price of oil-linked perpetual contracts on the Hyperliquid platform surged 5% as traders digested the shock in real time."

Just two weeks after the outbreak of war, the trading volume of oil-linked perpetual contracts surged from $200 million to a cumulative $6 billion.

A major隐患 of emerging platforms is liquidity. If liquidity is insufficient, bid-ask spreads may widen, causing traders to face a pricing disadvantage worse than on other platforms.

Last week, as U.S. President Trump consulted with Iranian officials on holding "productive talks," the Hyperliquid platform demonstrated its strong liquidity. The newly launched S&P 500 index futures based on the HIP-3 platform were able to accurately track the movement of the CME E-mini S&P 500 futures, down to the minute.

Although the on-chain perpetual contract was about 50–70 points lower than the ES, the magnitude of the price movement was similar.

What This Means

For decades, traditional markets have been bundled and controlled venues (exchanges), time (trading sessions), and products (indices/contracts).

They chose to maintain the status quo because they failed to establish mechanisms to address inefficiencies such as time delays, trading hour restrictions, and regulatory constraints on non-U.S. investors. Instead, they掩盖了 these inefficiencies and packaged them into procedural systems designed to build trusted institutions to attract investors.

People still trade and invest. This is not because they are stupid, or because they believe the rhetoric peddled by traditional financial markets. They do it because they have no choice. This began to change with the advent of blockchain, which provided the world with on-chain markets, making trading and investing easier than ever before.

People saw this choice and seized it.

They didn't care in the past, and they won't care in the future about changes in market structure. They also don't care whether the new structure is bundled or unbundled. As long as traders and investors can more easily express their opinions through financial instruments, they will embrace the new market structure, whether existing institutions like it or not. It doesn't matter if this structure comes from traditional giants like Nasdaq, Cboe, or S&P 500, or from a permissionless platform running on a blockchain.

The financial industry continues to evolve as it always has, and will adopt any structure that narrows the gap between the occurrence of an event and the expression of price opinion.

Important events are happening all over the world, every hour of the day. So why should prices have to wait until a clock starts ticking on a Monday morning in a glass-walled building in New York before they are determined?